collapse of Terra and the subsequent collapse of FTX marked the start of the so-called crypto winter, with the collapse of the once-booming decentralized finance (DeFi) segment. TVL has stagnated for more than a year, with the current level about 77% below the end-2021 ATH.

Nevertheless, in contrast to the broader trend, the DeFi category Real World Assets (RWA) is growing rapidly. The value deployed in the segment has risen by more than 70% since the start of the year.

In this article we discuss tokenised real-world assets, their characteristics, links to traditional finance, and prospects.

- Demand for tokenised assets (real estate, equities, and treasury bonds) is rising steadily.

- RWAs open broad opportunities for market participants to earn returns and diversify investment portfolios.

- For the sector there are specific constraints and risks, for example: mandatory KYC-procedures, minimum balances for full interaction with platforms, and the risk of borrower default due to unsecured loans, etc.

What are Real World Assets?

As the name implies, Real World Assets are existing tangible and other assets (real estate, commodities, works of art) that are tokenised for use in the DeFi space.

RWAs are widely represented in TradFi, being its foundational element. The global real estate market in 2020 was valued at $326,5 trillion, with the corresponding figure for gold exceeding $12 trillion. The Real Assets sector is enormous, but still poorly integrated with DeFi, signalling substantial growth potential.

Real World Assets open up new opportunities for DeFi participants, including yields attractive relative to TradFi. The new asset class can also be used to reduce volatility and diversification of investment portfolios.

The main idea of RWA is to create on-chain investment instruments tied to real assets. Instead of recording ownership on paper, it is entered into a distributed ledger. This allows parties to trade assets or their fractions directly, without intermediaries.

Advantages of this approach:

- reduced costs by removing intermediaries such as lawyers, brokers, banks, etc.;

- fast and efficient 24/7 trading of assets that are traditionally traded only during business hours;

- lower entry barriers;

- increased liquidity of assets;

- transparency of processes.

Real World Assets also include stablecoins — assets like USDT and USDC that are essentially tokenised dollars.

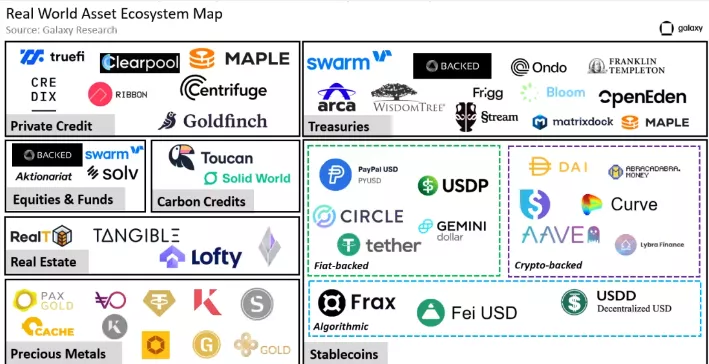

The RWA ecosystem is confidently developing, continually replenished with new projects.

Major funds are examining RWAs’ advantages. For example, hedge funds T. Rowe Price Associates, WisdomTree, Wellington Management, and Cumberland evaluate advantages of on-chain deals and settlements for currency and interest-rate swaps using subnetworks Avalanche.

JPMorgan launched Tokenized Collateral Network (TCN). The blockchain solution has already been used by BlackRock and Barclays for converting shares into digital tokens and the subsequent OTC trading of derivatives between the two institutions.

In July, the Securitize platform released security tokens on the securities of the Spanish real estate fund Mancipi Partners.

RWA’s Place in the DeFi Ecosystem

Some DeFi projects offer users the possibility to invest crypto assets (primarily stablecoins) in traditional financial market instruments, including government and corporate bonds.

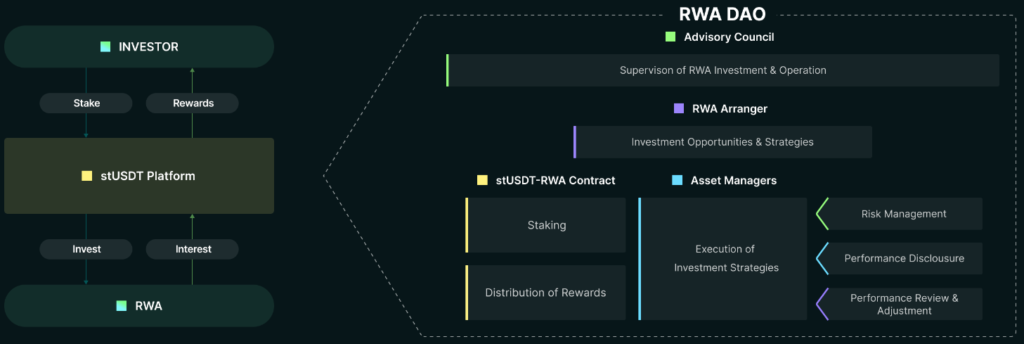

One such RWA platform is stUSDT on the TRON and Ethereum blockchains. The service enables staking of USDT at just over 4% annual yield. In return, users receive a “token-receipt” for stUSDT, confirming investments in real-world assets such as short-term government bonds.

TVL of the stUSDT platform has surged since July and has already reached $1.78 billion (as of October 11, 2023).

Another noteworthy platform is Ondo Finance, where the USD Yield (USDY) asset is used.

“USDY is a tokenised note backed by short-term U.S. Treasuries and demand deposits, delivering institutional-grade yields with low risk,” the project site states.

The protocol converts users’ stablecoins into fiat dollars, which are then used to buy real assets. Accordingly, as funds are invested, new tokens are minted. The latter are burned upon redemption, and users receive USDC in return.

The platform offers around 5% yield on invested funds. USDY-locked value exceeds $30 million.

On Ondo Finance accounts for around 50% of the tokenised securities market. In September, L2 project Mantle Network announced support for USDY.

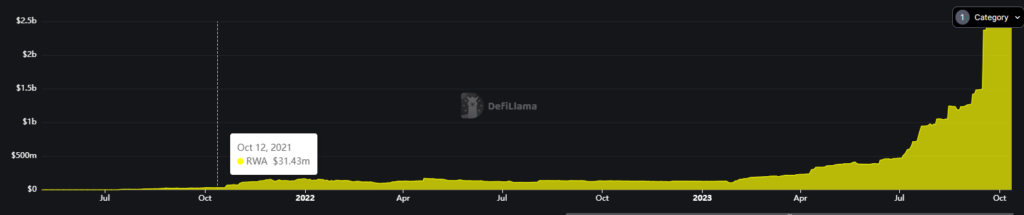

The chart below shows the heady growth of RWAs. In October 2021, the segment’s aggregate TVL (excluding stablecoins) stood at about $30 million. In just two years, the figure rose by more than 700%.

The combined TVL of the RWA segment stands at $2,4 billion (as of 11 October 2023). This figure is higher than those of the “Derivatives”, “Yield aggregators”, and “Cross‑chain solutions” categories in DeFi Llama’s ranking.

Outlook for the RWA Segment

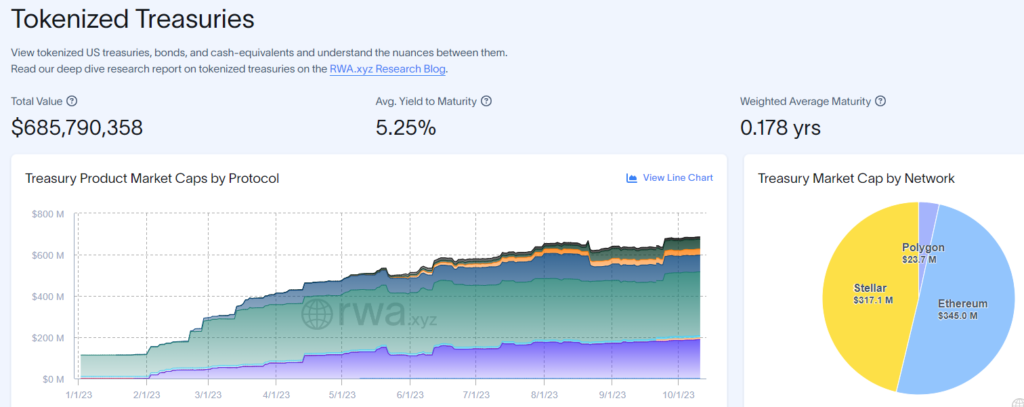

Demand for tokenised U.S. Treasuries is growing. The total capitalisation of these financial products is approaching $700 million. The most popular blockchain ecosystems are Ethereum, Stellar, and Polygon.

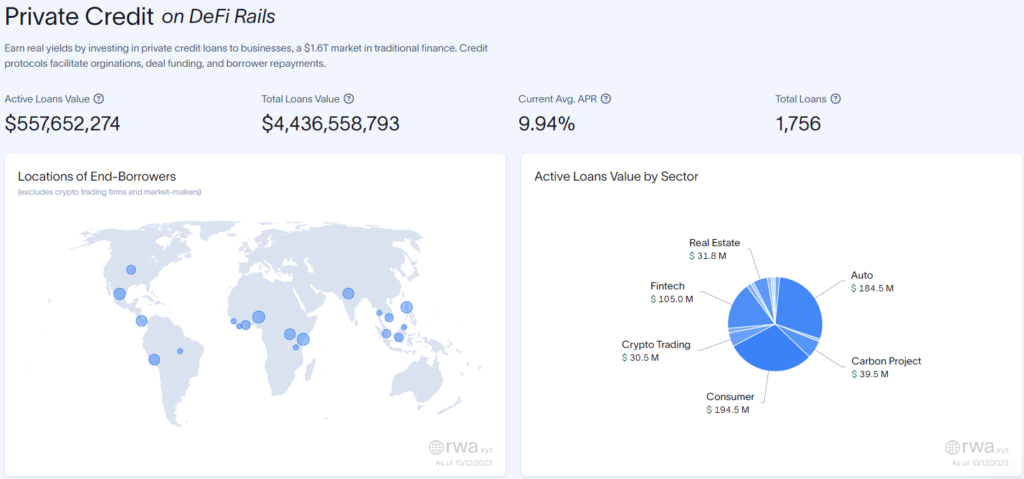

A sizable share of the TVL in the RWA segment is accounted for by tokenised private credits, issued by non-bank institutions. As of 12 October, the total value of outstanding such loans stood at $557.6 million. The average rate in the segment is about 10%.

The most popular private-credit protocols:

- Maple Finance (syndicated loans);

- TrueFi (“modular on-chain lending infrastructure” with native token TRU);

- Goldfinch (unsecured crypto loans);

- Centrifuge (lending platform, focusing on a broad range of RWA assets).

Significant demand for private credits is visible among residents of Kenya, Uganda, the Philippines, India, and other developing countries.

Total new-type loans rose 84% from January 1 to September 30. Galaxy analysts, however, note the metric remains about 70% below the summer 2022 peak. The overall market capitalisation of tokenised real assets is also about 9.6% below spring last year’s peak.

According to a Bank of America April report, the size of the tokenised gold market has already surpassed $1 billion. The financial giant called RWAs “a key driver of digital-asset adoption.”

Galaxy research shows that 82% of the value created in the segment this year comes from income-generating assets like private credits, real estate, and Treasury bonds. The share of such instruments in the RWA segment has nearly doubled over the last three quarters.

Experts say that the growth in interest in new products is largely facilitated by monetary-policy measures by the U.S. Federal Reserve.

“This has created new demand for certain types of RWAs among native DeFi users seeking higher yields on their crypto assets,” Galaxy analysts noted.

Limitations and Risks

Although many RWAs are issued on public blockchains, they typically do not offer permissionless access to financial products and services.

In most cases, users interacting with real on-chain assets must undergo KYC/AML procedures. Access is often limited to accredited investors with balances meeting minimum requirements. Thus, in Real World Assets, restrictions are no less stringent than in traditional markets.

“In addition to the technological risks inherent in all on-chain apps and services, there are also unique risks associated with RWAs,” Galaxy analysts noted.

As an example, experts cited the risk of funds loss due to borrower insolvency, largely due to the unsecured nature of some private loans.

As the segment grows, more projects experiment with RWAs. For example, stablecoins backed by real-world assets are being created.

One such project — Real USD — suffered a setback in October. The asset-backed stablecoin, primarily backed by tokenised real estate, suddenly lost its peg to the U.S. dollar, dropping by 50%. The likely reason for the depeg was a wave of redemptions of low-liquidity collateral.

Conclusions

The drivers of growth for most RWA platforms are predominantly native crypto-market participants, not institutions. Yet some major organisations such as Franklin Templeton and BlackRock have shown genuine interest in tokenising real assets.

Tokenised stocks, bonds, funds and other financial products have long been available in the market. The TVL of corresponding platforms has steadily grown, despite the prolonged stagnation of the broader DeFi segment.

Despite rapid growth even amid the crypto winter, RWAs remain at an early stage of development. But one can confidently speak of gradual maturation and significant potential for the segment in the future, given its still-minuscule size relative to the traditional financial market.