Fixed-rate instruments are among the bedrocks of traditional finance. The rigidity of their initial terms reduces uncertainty for lenders and borrowers.

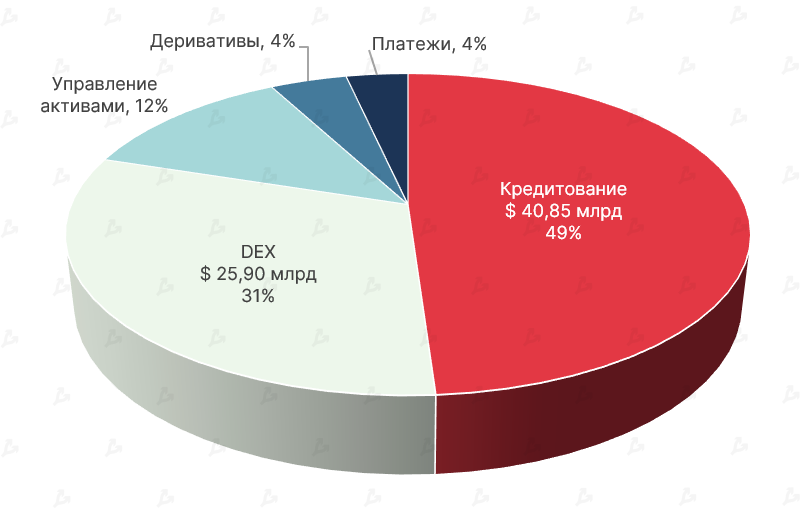

Lending protocols are expanding rapidly, accounting for the largest share of the DeFi sector.

However, most such protocols entail a constantly shifting cost of borrowing and return on invested capital. While for some assets on Aave there are fixed rates, they are relatively high for borrowers, and their magnitude can vary with sharp changes in market conditions.

Nevertheless, protocols that originally offer fixed-rate interest (Fixed Interest Rate Protocols, FIRPs) are emerging and gradually gaining traction. Their mechanisms for stabilising borrowing costs can differ markedly, and some instruments bear clear similarities to traditional market products such as bonds.

ForkLog has examined the features of these relatively new, intricate yet increasingly popular DeFi instruments.

Key points

- FIRPs are slowly but steadily growing their TVL. Such protocols appear to be a natural stage in the evolution of the DeFi sector.

- Fixed-rate instruments may seem complex, especially for newcomers. The simplest of them resemble bonds, but there are more sophisticated solutions — tranche-based with different risk levels and based on game theory.

- The interfaces of many FIRPs are not particularly intuitive, and some platforms clearly lack liquidity. It will be interesting to monitor the segment’s development against a bear market when a large share of investors search for a “safe harbour” for assets.

What are fixed-rate protocols for?

Credit is the cornerstone of any financial system. It gives firms a powerful incentive to grow, boosting working capital and expanding fixed assets. Individuals meet temporary cash needs, while lenders earn income from the funds lent.

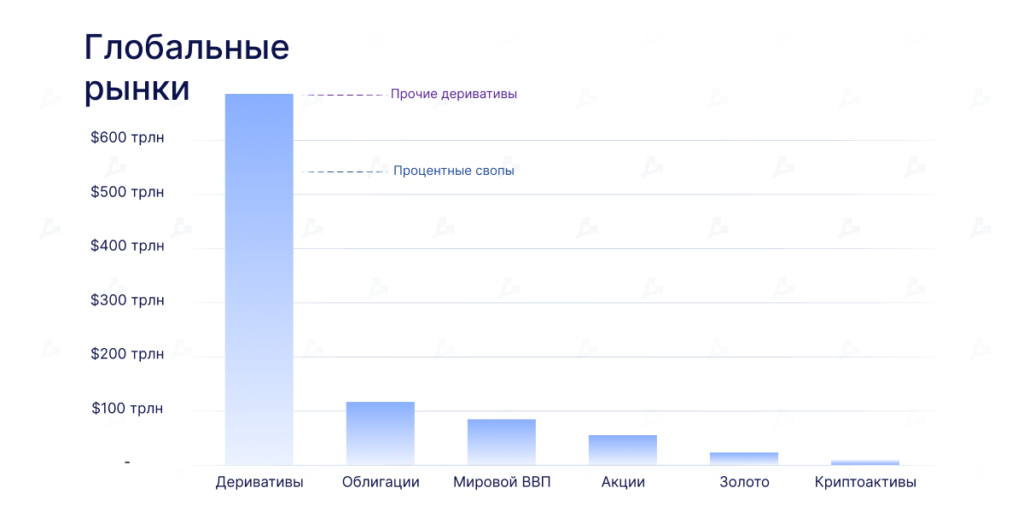

The global credit market is roughly three times the size of equities. The fixed-income securities market was worth $128 trillion in August 2020.

One of the largest segments of traditional finance is the market for interest-rate derivatives, including futures, options and interest rate swaps. In the first half of 2019, the total notional value of outstanding interest-rate derivatives obligations stood at $524 trillion, according to data from the Bank for International Settlements.

These astronomical sums fascinate the imagination, and given DeFi’s trajectory, it is unsurprising that decentralized, open-access and no less efficient analogues are developing in the space. The aggregate TVL of lending protocols is likely to continue rising.

DeFi developers have produced innovative projects handling user assets worth billions of dollars:

- Aave, Maker and Compound (lending).

- Curve, Uniswap and SushiSwap (decentralized exchanges).

- Synthetics, dYdX and Nexus Mutual (synthetics and derivatives).

- yEarn, Autofarm (yield aggregators).

However, the vast majority of DeFi projects rest on over-collateralised loans and floating rates.

In DeFi, activity surges often drive up on-chain fees and interest rates, which does little to encourage mid- to long-term investment and financial planning.

Market conditions in the crypto space and in DeFi can shift quickly, causing sharp changes in capital costs. As a result, lenders and borrowers need to monitor the market closely and periodically rebalance their positions to maximise income or minimise interest payments.

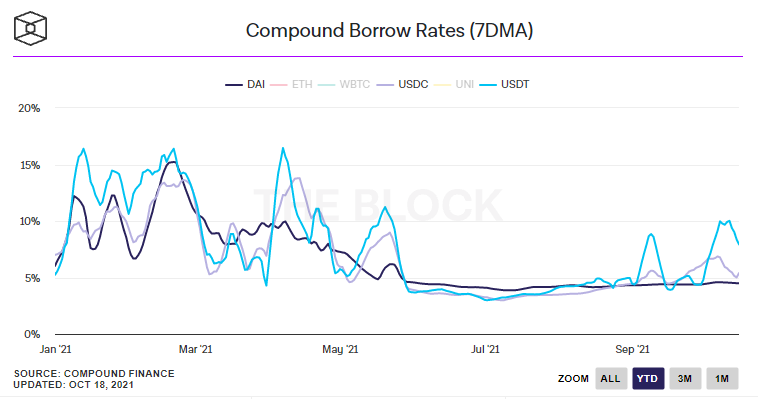

On the chart below, borrowing rates for stablecoins USDT, USDC and DAI were high in early 2021 when exuberance prevailed. In the May correction, these figures fell significantly.

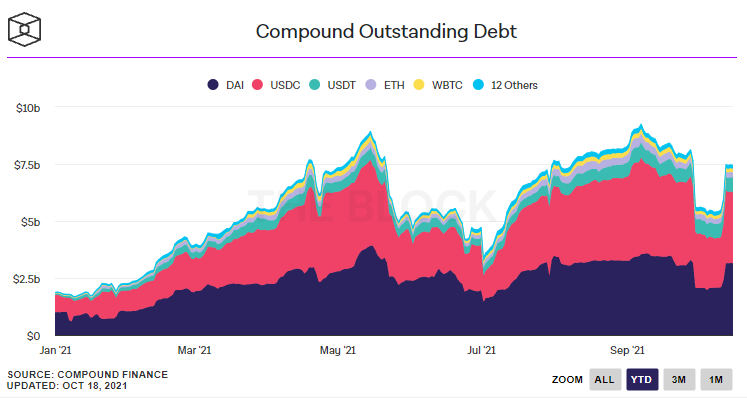

The chart of total outstanding debt on Compound mirrors the same dynamic — growth during upswings and declines amid corrections and softer investor sentiment. In Q3 2021, as Bitcoin moved toward a new all-time high , the amount of issued loans increased by 57%.

According to Messari researcher Jack Purdy, fixed rates provide lenders and borrowers with certainty, as well as the ability to forecast costs and returns on invested capital with precision. This is, among other things, a tool for gauging market sentiment.

Purdy believes that protocols such as Yield, UMA and Mainframe (now HiFi Finance), whose instruments resemble bonds in many respects, will bring DeFi closer to the traditional market.

TVL figures for the handful of fixed-rate protocols remain modest. Yet FIRPs present an untapped field for developers and other market participants. That suggests further growth for this sub-segment.

Main types of FIRPs

FIRPs are intended to offer market participants a set-and-forget solution, with loan maturities and interest rates fixed. A following example helps illustrate how it works.

Suppose a user wants to borrow a little USDC against ETH collateral at a fixed rate. To do so, they must create and then sell tokens that effectively represent ultra-collateralised zero-coupon bonds. These tokens then need to be repaid.

In this example, ETH trades at $4,000 and, to implement this scheme, the borrower could:

- deposit 1 ETH into the FIRP smart contract as collateral;

- issue 2000 bUSDC-JUN — USDC-denominated notes with a maturity of June 30, 2022 (the coins represent the borrower’s obligation to return 2000 USDC);

- on January 1, 2022 sell 2000 bUSDC-JUN at a discount on the open market — for $1950;

- repay the debt on June 30 or earlier to release the collateral (the tokens are burned at maturity).

In simple terms, the user borrowed 1,950 USDC at the start of the year. Over six months the amount to pay to settle the debt will be 2,000 USDC. Essentially, they raised funds at 5% per annum.

It is important to note that if the collateral-to-debt ratio falls below the level set by the protocol, the position is liquidated to partially cover the loan. Similar mechanisms are implemented in MakerDAO and Reflexer, issuing DAI (an algorithmic stablecoin) and RAI (a low-volatility token) respectively. Borrowers still need to monitor their positions to avoid liquidations.

Now consider a lender’s perspective. The lender can buy on the open market the debt-backed tokens at a discount and, after some time, settle them at par. For example, a lender could:

- buy 1 January 2000 bUSDC-JUN for 1950 USDC;

- settle 2000 bUSDC-JUN and, thus, release 2000 USDC on or after June 30.

Accordingly, the lender would earn a few percentage points on the funds lent.

Because debt positions are tokenised and interchangeable, lenders (or borrowers) can close them before maturity by selling or repurchasing.

Returning to MakerDAO, note that the protocol issues a super-collateralised stablecoin DAI. Borrowing rates are set by the community through lengthy procedures with discussions and votes. In the end, they may not fully align with current market conditions. In addition, many users may be unaware of community decisions until they take effect. Yield Protocol — a FIRP closely integrated with MakerDAO. Through this platform, users can lend and borrow DAI at a fixed rate.

Users of MakerDAO can move their debt positions or “vaults” into Yield Protocol and lock in rates until the maturity date. In doing so, fyDai tokens are used, which should be redeemed on a pre-set date. The vaults can then be converted back to Maker.

Ethereum-denominated fyDai tokens are akin to zero-coupon bonds. Borrowers issue tokens and sell them through Yield’s native AMM pool to obtain a fixed-rate loan.

Market rates depend on the value of fyDai. For lenders, a high price for fyDai means a lower yield to maturity. Conversely, a high token value implies advantageous rates for borrowers.

Consider a scenario where a user deposits 1.5 ETH to attract 900 DAI at a 10% annual rate. They receive 1000 fyDai, which the protocol automatically sells for 900 DAI. At the end of the year, the borrower will need to pay 990 DAI to free up their collateral.

Another example: Bob has 1 ETH and wants to borrow 1000 DAI for a year at 5%. Alice has 1000 DAI and is happy to lend it for a stable rate.

1 ETH is posted as collateral in Yield Protocol. Then 1000 DAI is sent to Bob from Alice, and 1050 fyDai is issued.

After a year, Bob repays 1050 DAI (1000 DAI plus interest) and returns 1 ETH. On the same day, Alice redeems her 1050 fyDAI to obtain 1050 DAI.

Thus, each fyDAI corresponds to 1 DAI at maturity. As an ERC-20 token, fyDAI freely trades on the market. Consequently, six months later Alice may find another buyer (for example, Fred) willing to purchase her 1050 fyDAI for 1025 DAI.

Bob does not realise that Alice has exited the trade and that fyDAI is now with Fred. Fred, in turn, also knows nothing of Bob. Fred will simply receive 1050 DAI for his 1050 fyDAI six months later.

Yield offers a range of pre-set bond-like tokens, differing by interest rates and maturity dates.

A second version of the protocol is in the works, supporting a variety of collateral types and longer maturities. Developers also promise gas-optimisation when interacting with smart contracts and a more user-friendly interface.

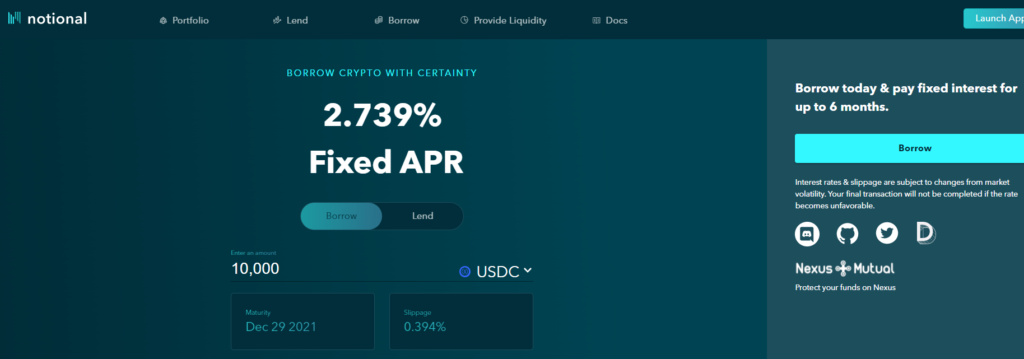

Notional — another lending platform on Ethereum with fixed rates and terms. The service is similar to Yield Protocol — offering similar zero-coupon-like instruments, but built on the fCash standard of EIP-1155.

Notional is positioned as an independent platform, not dependent on parent services like MakerDAO. In addition to DAI, the platform supports the stablecoin USDC.

If Yield requires 150% collateral, Notional requires 140%. In addition to Ethereum, the platform accepts USDC and WBTC as collateral.

«Notional’s interface includes stablecoin loans collateralised by other stablecoins, which doesn’t make much sense, but hints that the token list will expand», said Andrey Belyakov, founder of Opium Protocol.

He added that his project, like UMA, “from day one built contracts with fixed terms and conditions, but the market was not yet ready.”

«We’re seeing rising interest only now, as DeFi matures»,

said Belyakov.

The service began in mid-January 2021. Within three months, the platform’s TVL reached $17 million.

In April, Notional closed a Series A round, raising $10 million from Pantera Capital, Parafi Capital, 1Confirmation, Spartan Group, Nascent, Nima Capital and other investors.

In July, Notional version 2 went live. Key changes in v2 include:

- longer-maturity options for lenders and borrowers;

- integration with the lending service Compound, enabling liquidity providers to earn passive income by using nTokens.

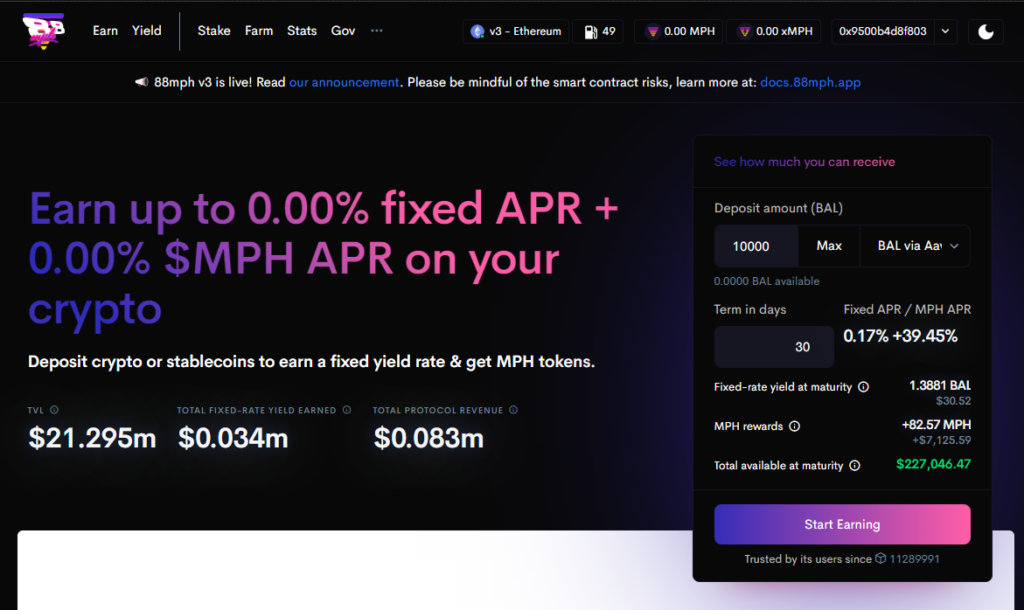

88mph. The protocol allows users to deposit stablecoins and other crypto assets, earning fixed-rate income as well as MPH tokens.

The system works as follows:

- The user contributes assets, selecting a maturity from 1 to 365 days (this changes the fixed yield and APR on the MPH token).

- Deposited funds generate yield at a variable rate via external protocols such as Aave and Compound until the maturity date.

- In return, users receive ERC-721 NFTs representing deposits with a custom maturity, or ERC-20 tokens (if the maturity period is preset).

- In addition to fixed-rate income, native project tokens — MPH — accrue until the maturity date.

- MPH can be staked on the 88mph platform to earn additional yield and participate in governance.

The fixed rate is formed by smoothing the 30-day exponential moving average (EMA) of the variable yield. Depending on the maturity, 88mph offers yields at 25-75% of the EMA value.

Besides Ethereum, the platform supports Polygon, Avalanche and Fantom. TVL of 88mph as of 23.10.2021 stands at $41.6 million, according to DeFi Llama.

There is also another approach enabling fixed yields. For example, pools tied to various protocols are categorized into — so-called tranches with unique characteristics.

Such services aggregate user funds and allocate them across lending protocols. Yields generated by the latter are distributed among market participants non-proportionally — according to their risk tolerance.

Users must choose the tranche that suits them — senior (safe, with a conservative rate) or junior (high-yield, but with higher risk). If senior inflows exceed expectations, the junior tranche earns extra income. Conversely, juniors incur losses if seniors fall short of expected returns.

Assume the senior tranche carries a fixed rate of 5% APR. The senior-to-junior TVL ratio is 7:3. If the pool’s overall annual yield is 10%, the senior tranche would receive 5% APR. In this case, the junior tranche would gain from the 21.6% APR advantage.

However, suppose overall yields are a mere 3% APR. Then the senior pool still earns 5% while the effective rate on the junior pool becomes -1.6% (reflecting the risk of holding positions that offer higher returns for conservative investors).

It’s clear that the junior pools must possess sufficient liquidity to guarantee senior-pool yields across market scenarios.

Saffron Finance allows users to assemble portfolios with different risk-return profiles by selecting annuities in categories AAs or As.

To access high-yield tranches (A), one must stake the native token SFI.

The ecosystem includes a built-in risk-reduction mechanism — high-risk tranche holders insure the losses of more conservative investors (AA).

In version 2, the protocol implements perpetual staking, automatic compounding, and multi-currency tranches. Akin to BarnBridge, one of its early products is SMART Yield Bonds, which aggregates yields from protocols such as Compound and distributes them among senior and junior pools. The latter differ in risk and return parameters.

Unlike SFI, the token is not used for staking, but only for governance.

TVL of the BarnBridge project stands at $23.1 million, according to DeFi Llama as of 23.10.2021.

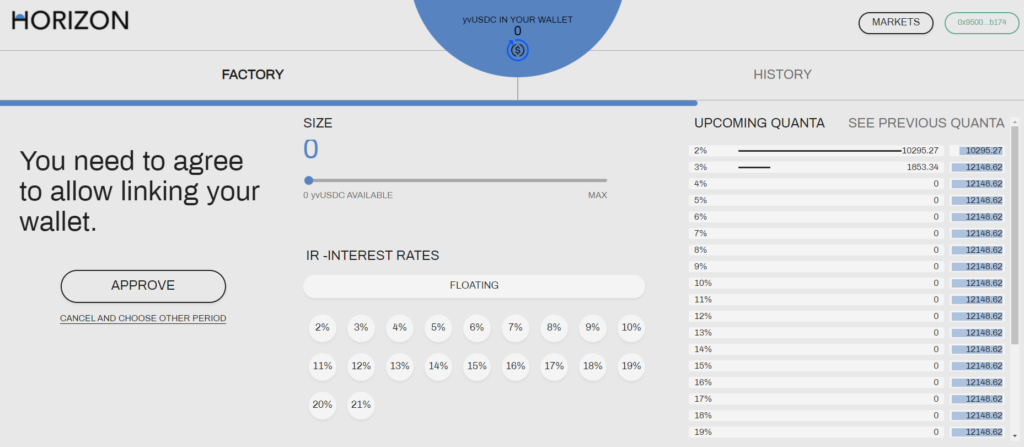

There are also FIRPs based on game theory — for example, Horizon. Users deposit collateral into a liquidity pool that interacts with lending protocols like Compound. Then market participants are invited to place hidden bids on fixed rates (serving as upper yield limits), or on floating rates for different rounds.

After each round bids become visible, creating a semblance of an order book.

The protocol ranks bids from lowest to highest and distributes proceeds from the lending protocols accordingly. Surplus funds (if any) flow into the floating-rate pool.

As noted, the posted bids eventually become visible. This allows users to actively compete, identifying the most popular rates. Additionally, market participants can freely adjust their bids, setting a floating rate if desired. Horizon can thus be viewed as a forecasting protocol.

The platform can only be considered FIRPs-like, since interest rates are not truly fixed. Yet the system rewards users who correctly forecast future yields. Those who stake too high a figure or opt for a floating rate risk underperforming or earning nothing.

The project remains in beta. The team plans to launch a native token HRZ, though its purpose remains unclear.

Among the platform’s investors are: Alameda Research, Framework Ventures, Mechanism Capital, DeFiance Capital, Spartan Group, NGC, Incuba Alpha, Ruby Capital, Robot Ventures, ASResearch.

There are also other variants of protocols offering fixed-term loans. For example, a key feature of Ruler Protocol and Timeswap is the absence of liquidations.

Advantages and drawbacks of FIRPs

The projects described above are quite complex to grasp. FIRPs are unlikely to win broad popularity among newcomers to the industry or even among more experienced users accustomed to AMM and lending platforms.

Interfaces of Yield Protocol and Notional appear to be relatively intuitive. The tools they offer are straightforward and share much with zero-coupon bonds. However, the TVL of these projects remains small compared with DeFi Llama’s leaders. This is probably due to the comparatively low rates offered to users.

Substantial sums of money flow through 88mph. Clearly this is achieved via liquidity mining — MPH tokens are generously distributed on top of a conservative fixed rate.

Attracting sufficient liquidity is arguably the main challenge for FIRPs. Additional incentives such as liquidity mining programs may partially and temporarily ease this problem. However there must be organic demand for new DeFi instruments, on which effective interest rates depend.

FIRPs may gain popularity thanks to lower transaction costs from second-layer solutions, integration of new protocols such as Polygon and Avalanche, and refinements of user interfaces, most of which remain not particularly intuitive.

It is also possible that interest in fixed-rate protocols will rise during a bear market, the onset of which is inevitable. However, FIRPs in that case face competition from custodial platforms such as Celsius Network or Compound Treasury.

Notably, Compound Treasury allows non-bank and other fintech firms to convert USD to USDC. Stablecoins are used in Compound at a guaranteed 4% interest, far above what companies typically earn in traditional bank savings accounts (around 0.7% per year).

***

The DeFi space is developing rapidly and becoming increasingly complex. Alongside decentralised options are emerging even more intricate instruments — fixed-rate protocols.

Developers face several tasks: creating intuitive interfaces and attracting sufficient liquidity. Projects may also encounter regulatory risks as the SEC and CFTC turn their attention to DeFi and derivatives on digital assets.

Nevertheless, FIRPs could appeal to conservative investors during a downturn, becoming a key element of the DeFi landscape thanks to more attractive rates relative to the traditional market.

Subscribe to ForkLog news on Telegram: ForkLog Feed — the full news feed, ForkLog — the most important news, infographics and opinions.