In 2021, the DeFi segment continued its rapid growth. Against the backdrop of Ethereum scalability issues, a multitude of alternative protocols and second-layer solutions emerged, offering fast and inexpensive transactions.

Active development of the sector opened up new use cases: fixed-yield protocols, algorithmic stablecoins, concentrated-liquidity managers and decentralised indices. The “DeFi 2.0 concept” gained popularity, focused on capital efficiency, stability of the native token and the building of cohesive communities.

ForkLog summarised the main aspects and trends in DeFi development in 2021, with a focus on the segment’s future prospects.

Key Points

- The DeFi sector continues to grow — new, often complex projects constantly appear. Many involve interaction with different protocols and second-layer solutions.

- A strong momentum to development came from algorithmic stablecoins, wrapped assets, yield aggregators and privacy-oriented solutions like Tornado Cash.

- Despite the abundance of new products, lending and decentralised exchanges remain core elements of the DeFi ecosystem.

Macro View

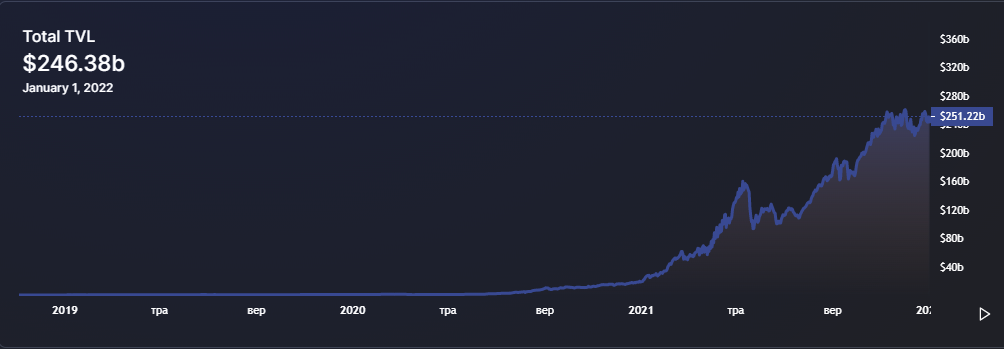

The total value locked in DeFi protocols (TVL) since the start of the year rose more than tenfold — from $18.65 billion to $246.38 billion (as of 1.01.2022).

Despite the rapid development of structured products in the “financial LEGO”, the majority of user assets remain concentrated in relatively straightforward lending protocols and liquidity pools on decentralised exchanges based on the automated market maker mechanism (AMM).

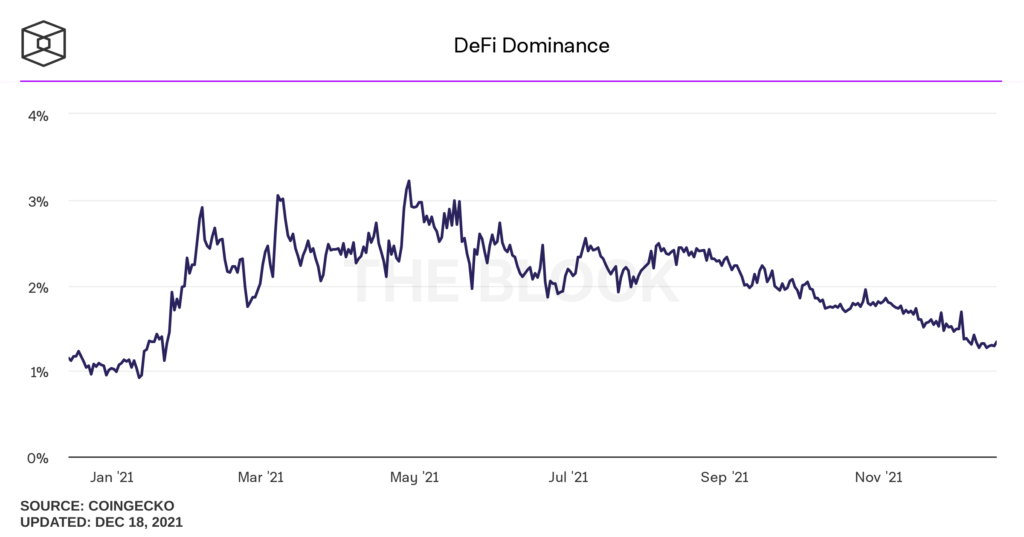

The aggregate market capitalisation of DeFi tokens relative to the overall crypto market remains modest — below 1.5%. Yet this could signal substantial growth potential for the sector.

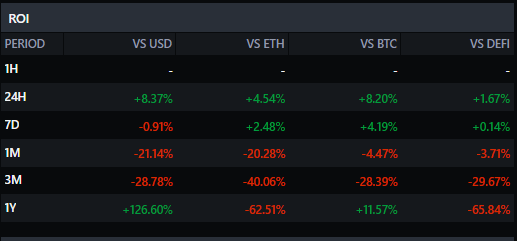

DeFi Pulse Index (DPI), consisting of the DeFi blue chips (AAVE, BAL, UNI, MKR, COMP, etc.), outpaced Bitcoin growth for most of the year, while lagging Ethereum.

The surge in ETH price in 2021 was largely driven by DeFi. This is because the second-largest cryptocurrency is used to pay gas. And as activity in the sector grows, so does demand for ETH.

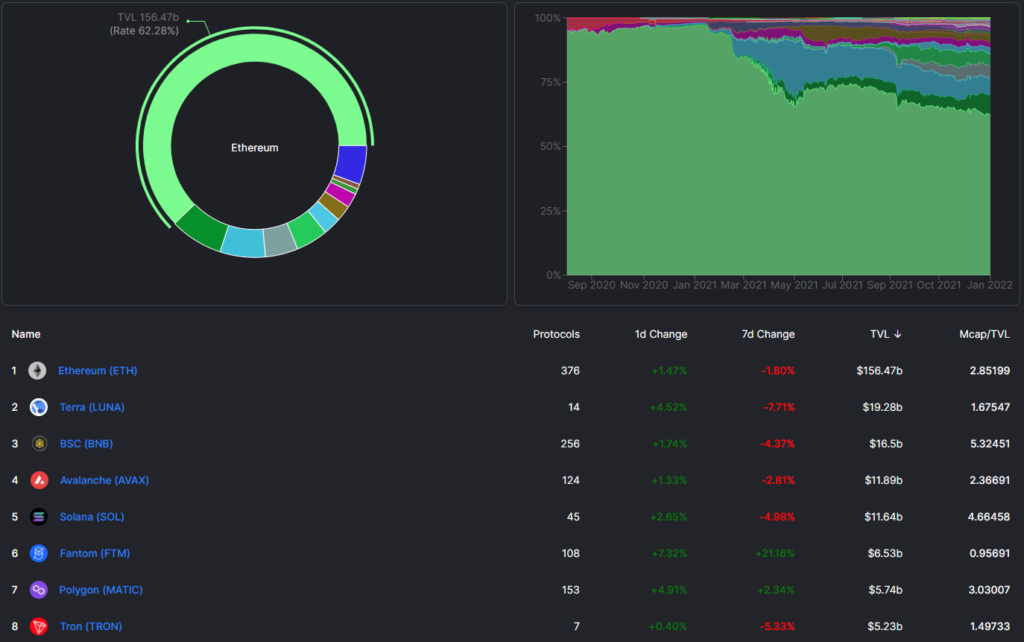

Ethereum remains the backbone of DeFi, but alternative ecosystems such as Binance Smart Chain (BSC), Terra, Avalanche, Solana, Polygon and Fantom are gaining traction.

Capital flows between protocols are boosted by cross-chain bridges. They enable users to move funds across platforms built on different technologies, selecting pools with higher yields.

Decentralised Exchanges

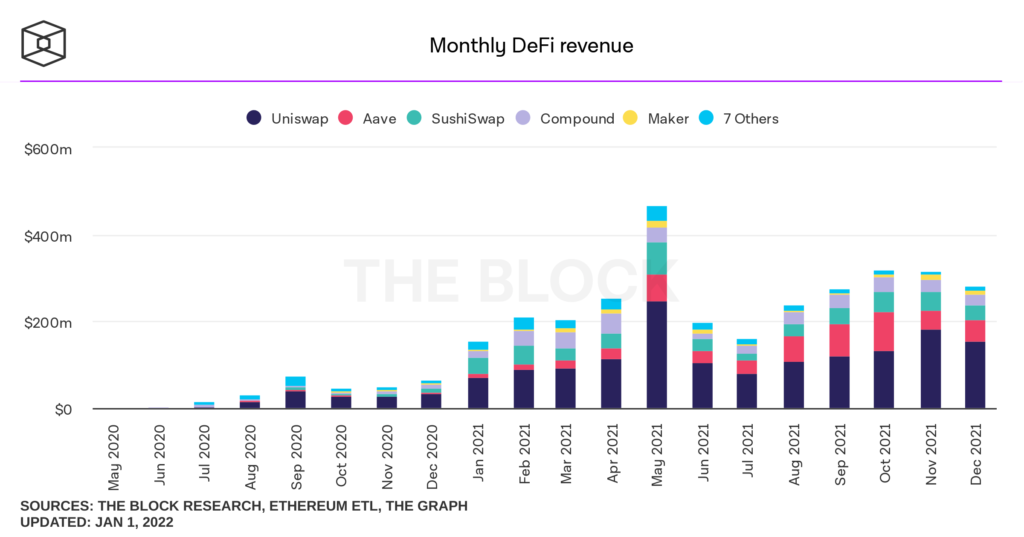

The decentralised exchange Uniswap plays a central role in the DeFi sector, being one of the first to implement and popularise the automated market maker mechanism.

Active users on the leading DEX exceeded 1 million for the first time in May. The platform 1inch achieved this milestone in December.

Uniswap consistently outperforms other popular protocols in terms of revenue.

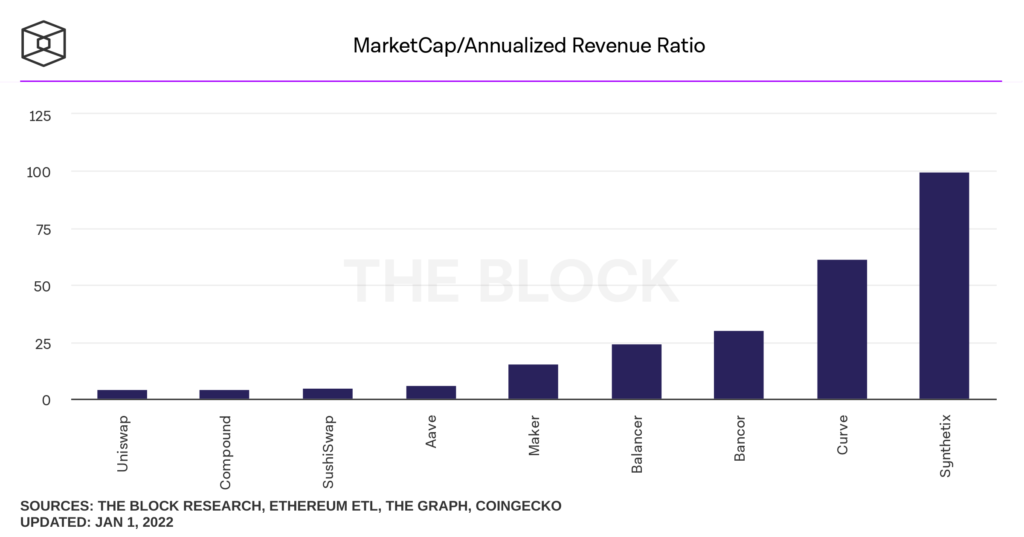

Along with SushiSwap, Uniswap has one of the lowest market-cap-to-revenue ratios among major protocols. This suggests the protocol is actively used, generates stable income, and that the UNI token is unlikely to be overvalued.

In the second half of the year Curve, which supports multiple networks, overtook Uniswap by TVL. Competition with PancakeSwap — the largest DEX ecosystem on Binance Smart Chain — also intensified.

Yet a potential new growth driver for Uniswap could be its integration with the Polygon protocol, which in early October surpassed Ethereum in active addresses.

🗳 The Uniswap community has voted to deploy v3 on @0xPolygon through the governance process.

⚡️ Uniswap Labs will deploy Uniswap v3 contracts within a few days.

👀 Stay tuned. pic.twitter.com/LwVLwEngPl

— Uniswap Labs 🦄 (@Uniswap) December 18, 2021

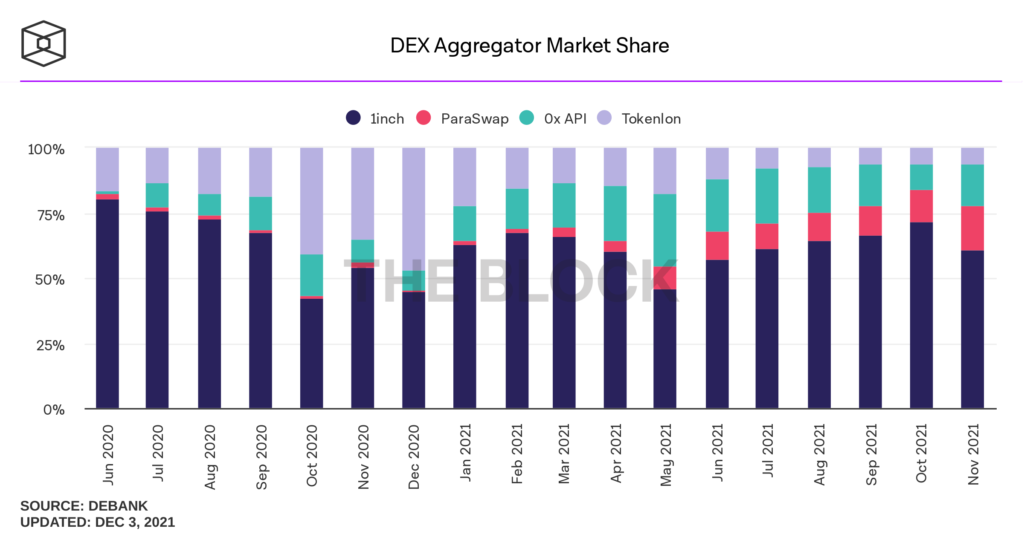

Among users, liquidity-aggregator platforms are popular, led by 1inch.

However, the market share of ParaSwap is growing, which in November conducted a controversial airdrop of its native token.

Lending Protocols

Lending protocols remain among the core components of DeFi. They offer passive income on invested funds and allow borrowing crypto assets (mainly stablecoins) at rates suitable for developing markets.

As of 2.01.2022, the top three lending protocols are:

- Aave with TVL of $14.4 billion, supporting Ethereum, Avalanche and Polygon;

- Anchor ($9.04 billion) on Terra;

- Compound ($8.85 billion) — a veteran on Ethereum.

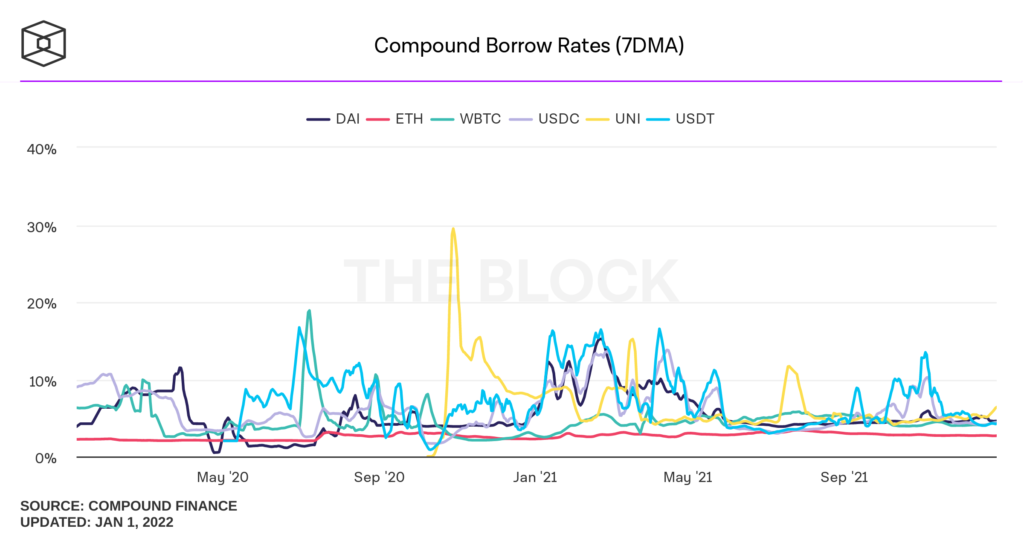

As the chart below shows, at the start of the year lending rates on Compound were relatively high and volatile.

As the market cooled toward mid-year, volatility declined. It is also notable that lending rates on stablecoins are markedly higher than those for ETH, WBTC or UNI.

In the crypto-lending space, traditional platforms offering “over-collateralised” loans dominate. Yet second-generation protocols such as Alchemix and Abracadabra are gaining traction. They aim for higher capital efficiency and fewer liquidations.

Progressively, protocols with fixed rates are developing, but their share of the market remains small.

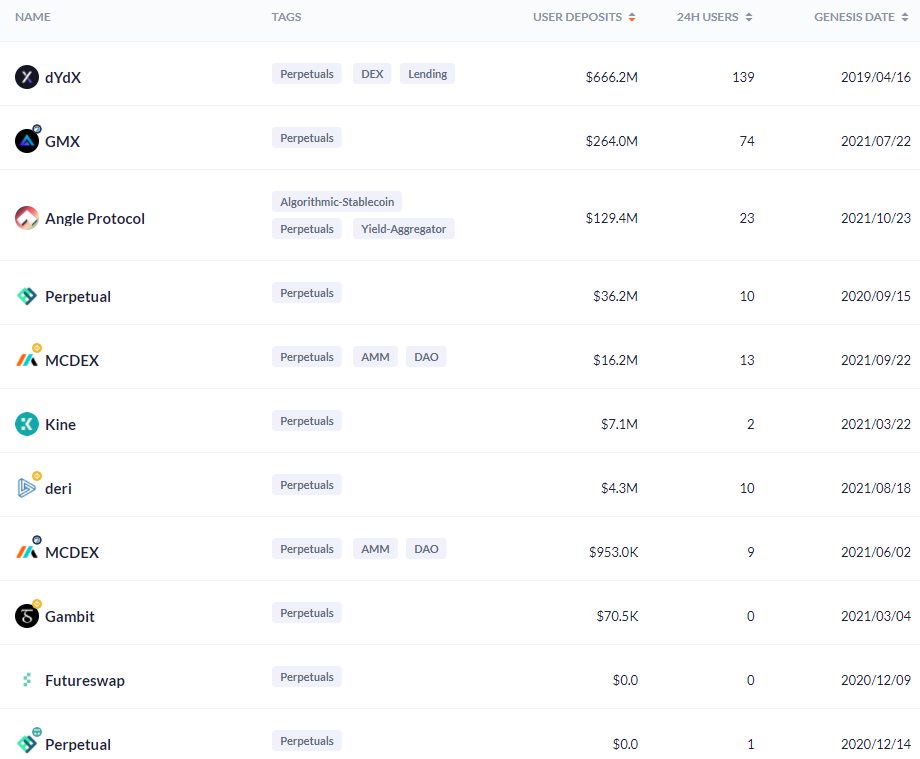

Derivatives

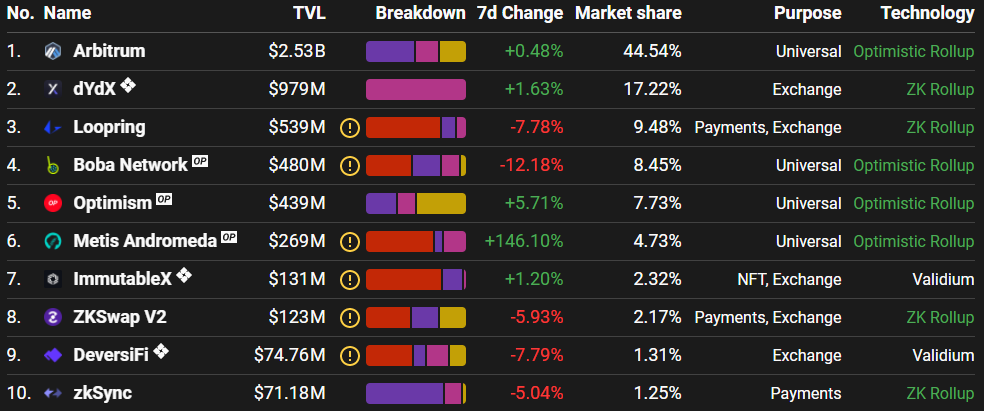

Among decentralised derivatives protocols, dYdX is the undisputed leader, with the highest liquidity and user counts.

dYdX also ranks highly for TVL among second-layer solutions.

The platform’s success owes much to a generous airdrop and the preceding launch of perpetual swaps on a second-layer protocol. In September, dYdX surpassed Coinbase by trading volume, echoing Uniswap’s earlier success.

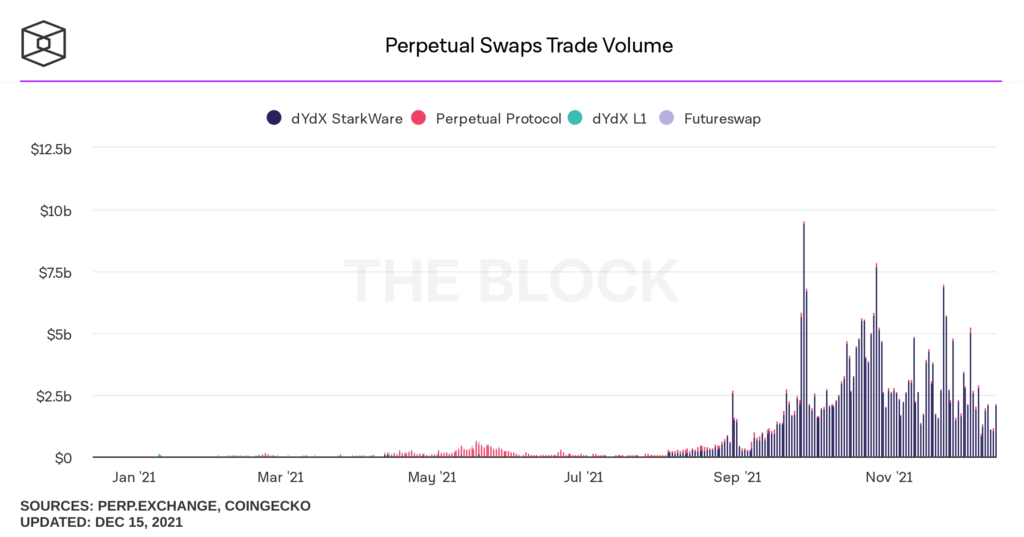

The chart below shows that among crypto-derivative platforms, May saw Perpetual Protocol leading in volume, while August saw dYdX take the lead.

Notably, autumn has brought a decline in turnover for dYdX, Perpetual Protocol and Futureswap. Relatively small TVL figures exist for decentralized options protocols. The top three are Ribbon Finance, Opyn and Lyra.

Decentralised options — though fairly complex, they are interesting instruments. For sophisticated investors they open new strategies, and for projects — broad opportunities for integrations.

Interfaces on some platforms are not user-friendly yet. It is also clear that many services lack liquidity.

Nevertheless, decentralised options are a natural stage in the evolution of the crypto industry and DeFi. These platforms still must mature and prove themselves as effective hedging and speculative tools.

Structured Products

As DeFi develops, more advanced tools emerge, including second-order protocols. This category includes overlay projects that sit on top of other services. Such platforms are designed for:

- automation of certain functions;

- increasing yield, for example through compounding accrued interest;

- expanding the functionality of base platforms.

In this sector Convex Finance leads as a yield aggregator. Launched in May, the protocol reached a TVL of $20 billion.

Convex Finance — a decentralised staking service built on the Curve protocol. It enables liquidity providers to increase staking yields without locking CRV tokens.

yEarn Finance, from the renowned Andre Cronje, was one of the first yield aggregators in DeFi. However, its TVL by the end of 2021 was much smaller than Convex Finance — “just” $5.69 billion.

A substantial rise in popularity occurred in the second half of the year for Tranchess, offering structured products for investors with varying risk appetites. Among BSC platforms the project ranks 3rd by TVL.

Into a separate category fall position optimisers for concentrated liquidity like Charm, Gelato and Popsicle Finance. These platforms aim to boost yields for Uniswap v3 liquidity providers and reduce impermanent losses.

Algorithmic Stablecoins and Wrapped Assets

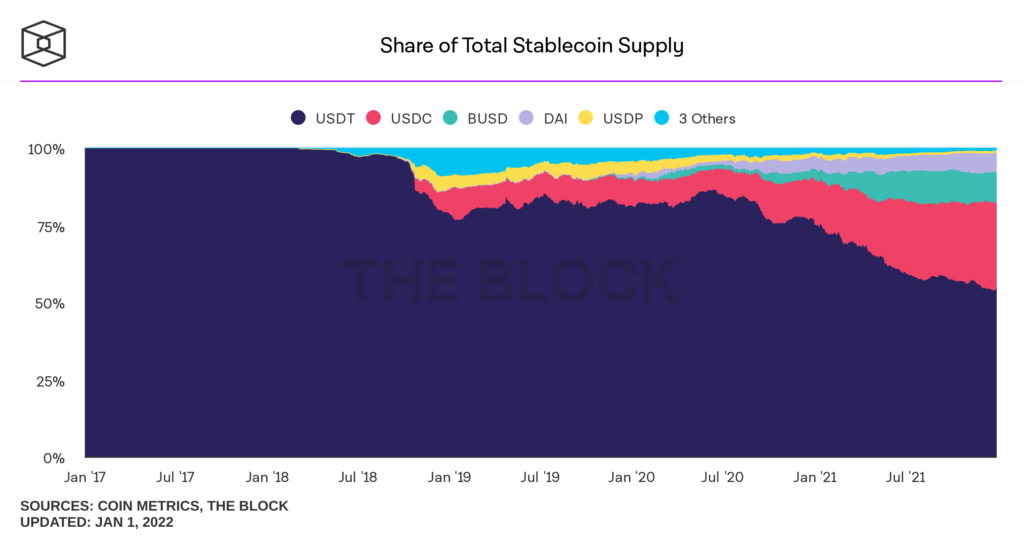

In the DeFi space centralised stablecoins such as USDT, USDC and BUSD dominate. Also popular are decentralised alternatives — DAI from Maker and MIM from Abracadabra.

Centralised stablecoins carry regulatory risks and counterparty risk. In September, the US Senate stated the need for full collateralisation of stablecoins with cash and equivalents and for regular audits.

Counterparty risk means that users must trust the issuer to back the tokens with reserves held by a reliable custodian.

DAI tokens are effectively a collateralised debt position at MakerDAO. The system is characterised by low capital efficiency, since collateral always exceeds the loan size. In other words, to generate a certain amount of DAI you must lock up a much larger amount in other crypto-assets.

In response to regulatory risks and inefficiencies of centralised and over-collateralised stablecoins, algorithmic “stablecoins” have emerged.

Projects resembling automated central banks use algorithms to manage the supply of assets and their underlying economics.

The indisputable leader in this sector is the Terra project’s UST — an asset-backed stablecoin pegged to the LUNA ecosystem. Unlike many other algorithmic stablecoins such as AMPL, BAC, UST benefits from high market capitalisation ( more than $10 billion) and price stability.

However, even UST can detach from its peg. For example, during May’s LUNA collapse, the stablecoin price dipped 3.8% before returning to parity with the dollar.

With ecosystem development and strong demand for Terra’s stablecoin, the native token LUNA rose to the 9th place in market-cap rankings, overtaking Avalanche, Polkadot and Dogecoin.

Beyond stablecoins, development of so-called “low-volatility tokens” continues, including RAI from Reflexer and OHM from Olympus DAO. The latter’s market cap exceeds $2 billion. These assets feature supply-control mechanics that respond to demand shocks.

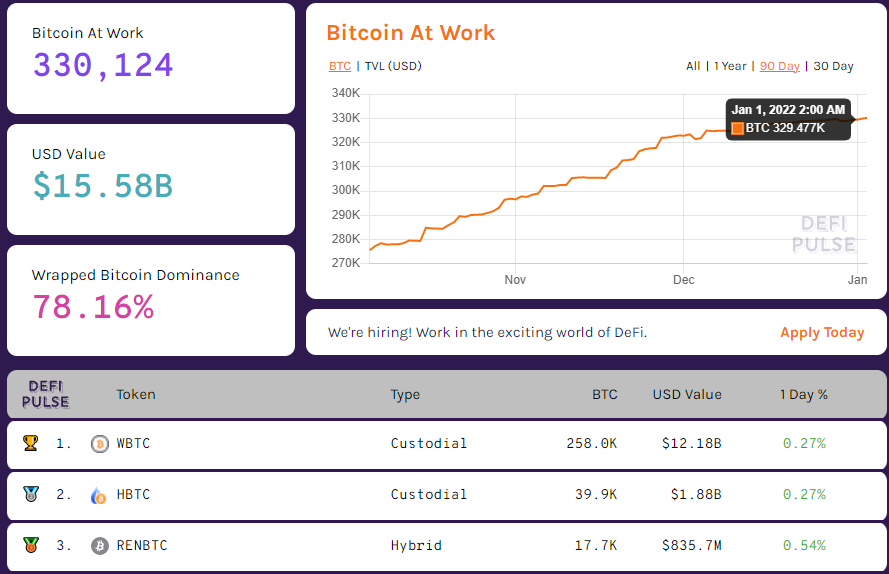

The tokenised BTC segment also continues to grow. Its supply rose from 140,000 to 329,477 since year-start (as of 1.01.2022). This accounts for 1.74% of Bitcoin’s circulating supply. The combined market cap of “BTC on Ethereum” exceeds $15 billion.

The share of Wrapped Bitcoin (WBTC) among leaders in the segment stands at 78.16%. A significant portion of WBTC is locked as collateral in lending protocols such as Maker, Compound and Aave.

The BTCB token — a BEP-20 token pegged to Bitcoin — gained notable traction in 2021. In early November its market cap surpassed $7 billion. More than 10% of BTCB supply is locked in the lending protocol Venus. Its TVL is around $2 billion. BTCB also plays a key role in Tranchess, with TVL above $1 billion.

Developing Segments

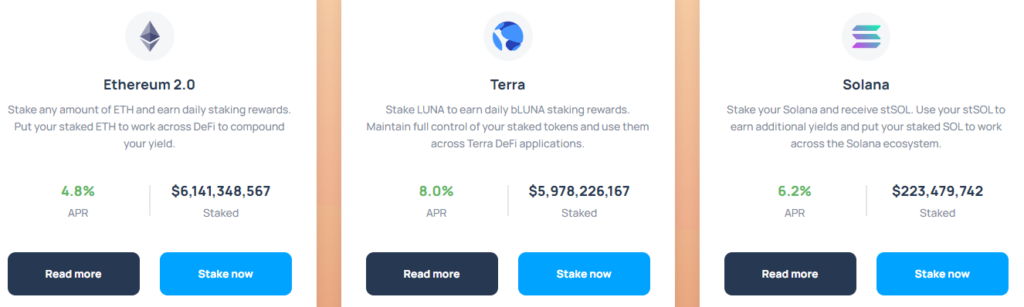

On 1 December 2020, the launch of Ethereum 2.0 Phase Zero occurred, marking the start of Ethereum’s gradual transition to a Proof-of-Stake consensus. Users can deposit ETH into the staking contract, becoming validators or delegating to other network participants.

Since the launch, users have sent 8.86 million ETH to the deposit contract. As of 2.01.2022 they are valued at about $33.28 billion.

Liquid Staking

Alongside the deposit contract, solutions for liquid staking emerged. One of the largest services — Lido — offers the ability to unlock ETH staked in order to use it in DeFi apps. The project uses the native token sETH, representing a tokenised version of the staked assets in the Ethereum 2.0 ecosystem.

The total value of assets staked in Lido exceeds $12 billion. In addition to Ethereum 2.0, the service allows staking LUNA to obtain bLUNA with an 8% annual yield. It is also possible to lock Solana to obtain stSOL.

MEV

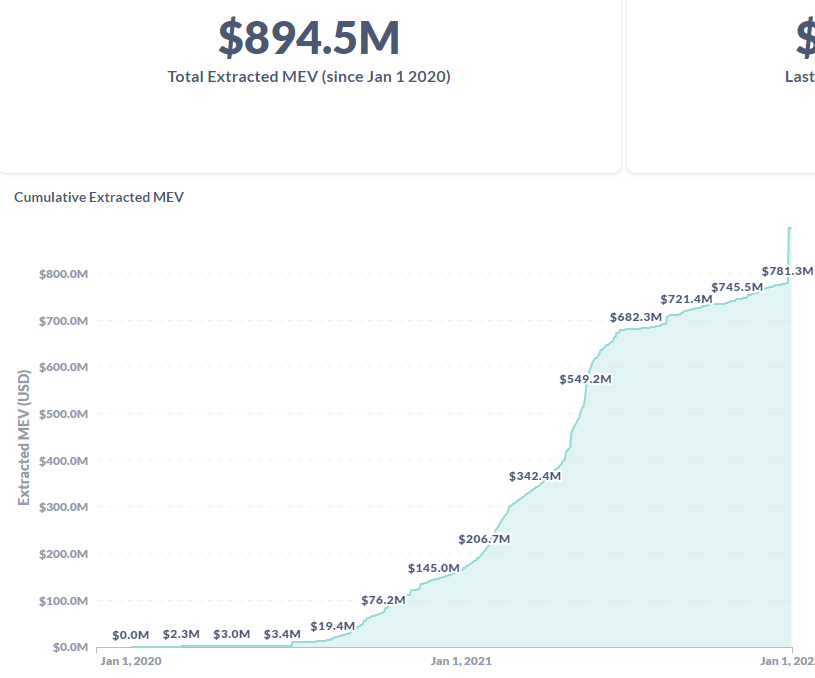

Among other developments, the Miner Extractable Value (MEV) concept — sometimes called the “invisible tax” on Ethereum — gained traction.

MEV refers to profits miners can earn by including, excluding or changing the order of transactions in blocks they produce.

According to MEV-Explore, since the start of 2020 market participants have extracted MEV worth almost $900 million.

In the MEV revenue mix, more than 97% comes from arbitrage using multiple liquidity pools across DEXs. The remaining 3% comes from liquidation strategies and their combinations.

Various services have emerged to minimise MEV-related losses. Among them:

- decentralised exchange CowSwap on the basis of Gnosis Protocol v2;

- KeeperDAO, using a private virtual mempool named Hiding Book;

- cross-chain platform Secret Swap on AMM;

- BackRunMe, a tool enabling confidential transactions resistant to front-running and sandwich attacks;

- TaiChi Network — a privacy-tinted transaction service managed by the SparkPool pool;

- mistX.io from Alchemist — a DEX built on Flashbots technology.

- MEV solution Fair Sequencing Services by Chainlink.

Privacy

Tornado Cash — one of the most popular Ethereum mixers. The service’s TVL rose from $55.5 million to $588 million (as of 2.01.2022). The peak was reached on 21 October at $1.17 billion.

The service’s popularity was boosted by airdrops of native TORN tokens, and by integration with the second-layer solution Arbitrum. Recently the Tornado Cash team rolled out the Nova pool, which allows depositing and withdrawing arbitrary amounts of ETH.

Insurance

This remains one of the few DeFi sectors showing lacklustre dynamics.

A significant share of the market in this sector is held by two protocols — Armor and Nexus Mutual. TVL for each is close to $600 million (as of 2.01.2022), a relatively small figure compared with leading DEX and lending protocols.

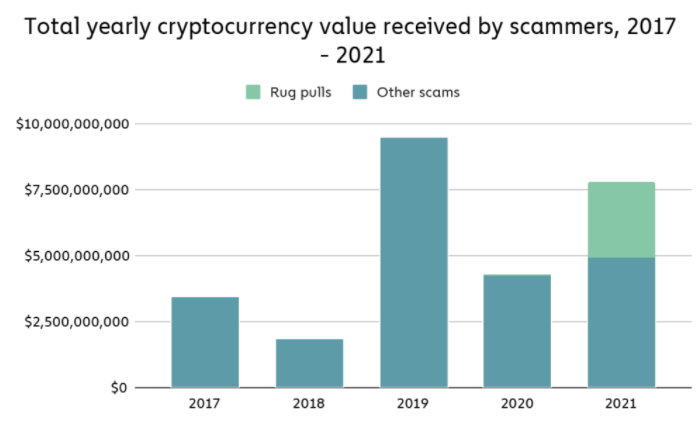

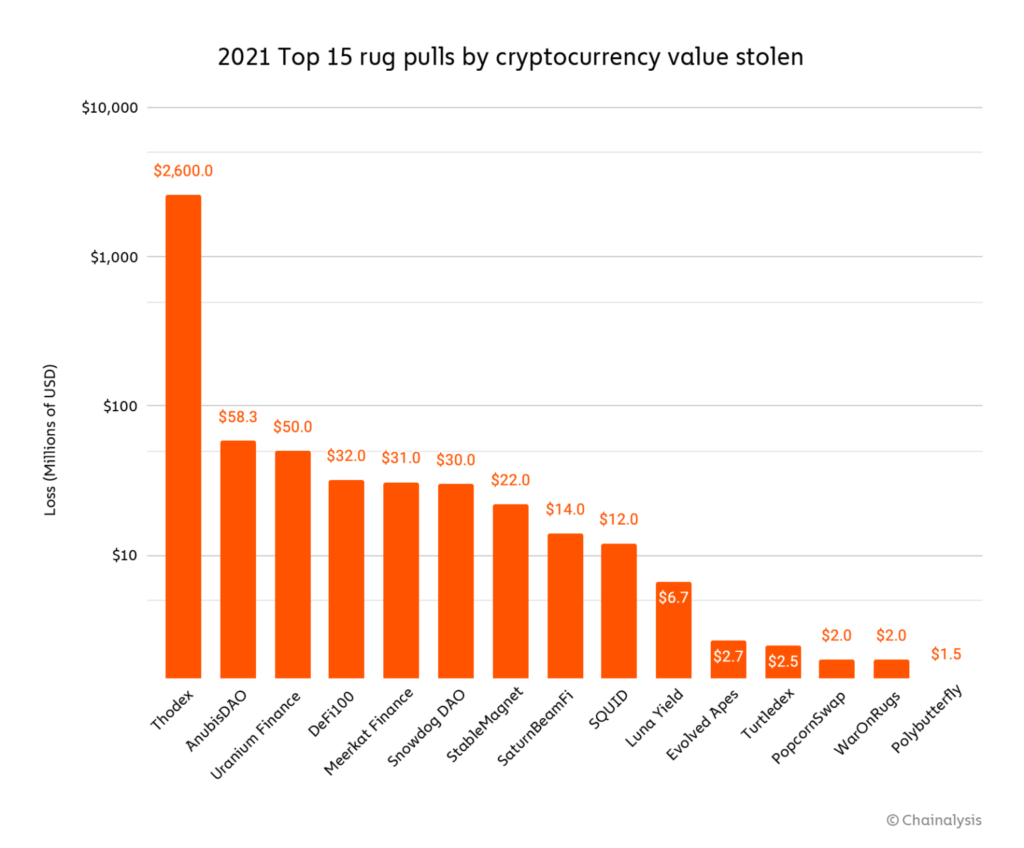

According to Chainalysis, in 2021 criminals stole more than $7.7 billion in cryptocurrencies. More than a third of this was from rug pulls.

Cybercrime in crypto markets rose by 81% versus 2020.

Rug-pull schemes spread widely across the DeFi ecosystem, accounting for more than $2.8 billion in losses in 2021. That represents 37% of all crypto-fraud revenues, compared with only 1% in 2020.

Chainalysis urged users to avoid new tokens that have not undergone code audits.

Conclusions

DeFi continues to evolve — new protocols, second-layer solutions and cross-chain bridges are drawing capital into the ecosystem.

The lending and DEX sectors remain the largest elements of the broad DeFi ecosystem. TVL in both sectors stays high thanks to ongoing liquidity inflows and a clear value proposition for many users. However, activity metrics on decentralised exchanges have lagged somewhat behind the May peaks.

Demand for perpetual swaps platforms and yield-optimisers remains strong. In these sectors, dYdX and Perpetual Protocol lead, while Convex and yEarn Finance are prominent in their respective niches.

We are witnessing the evolution of structured products, with yield aggregators playing a notable role. It remains to be seen how robust liquidity will prove in a bear market for these complex platforms.

Users of DeFi have seen the emergence of nascent sectors, including liquid staking, MEV and privacy tools. Yet not all areas saw growth — synthetic assets and insurance showed stagnation amid an overall uptrend.

In 2021, algorithmic stablecoins and “low-volatility tokens” appeared. Not all of them proved viable, as shown by significant price volatility.

Demand for established centralised stablecoins and tokenised BTC continued to grow. This signals healthy expansion for the DeFi sector and the broader crypto market alike.

Subscribe to ForkLog’s channel on YouTube!