The number of companies holding the “digital gold” in reserves keeps rising—along with the size of their balances. The trend is attracting attention from investors and tightening supply, fuelling demand.

At first the approach looked experimental. Interest surged after 2020, when Strategy (formerly MicroStrategy), founded by Michael Saylor, went all in—aggressively buying the first cryptocurrency with equity and debt financing.

The bold move signalled to other businesses seeking protection against fiat debasement, portfolio diversification and a shot at profits from a rapid rise in the price of digital gold.

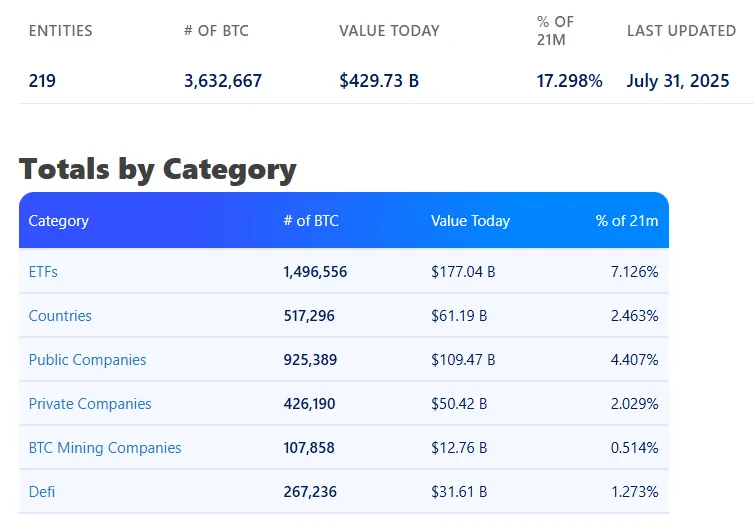

Today more than 200 public and private companies worldwide have adopted similar tactics, amassing over 1m BTC in aggregate.

Like any market, crypto moves in cycles, only with greater volatility and less predictability. The bear phase is not far off, and it will soon reveal the frailties of the “Strategy strategy” and how exposed lesser-known copycats really are.

Bitcoin proxies

According to BitcoinTreasuries, as of July 31 public and private companies hold more than 1.35m BTC worth over $160bn—>6.4% of the total issuance of the first cryptocurrency.

Such firms are often dubbed “bitcoin proxies”, as their share prices tend to correlate closely with the price of digital gold.

“The logic is simple: if the first cryptocurrency appreciates, the companies’ securities rise as well, giving investors indirect exposure to the digital asset,” — the Cointelegraph piece explains.

Owning such stocks can be a way to profit during crypto bull phases. Bitcoin’s price strength improves corporate financials and attracts investors who want upside without buying coins outright.

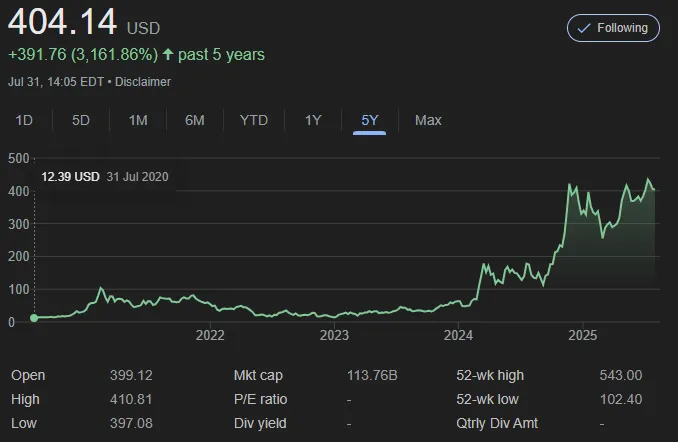

Strategy’s market capitalisation has multiplied many times since August 2020—when the Nasdaq-listed firm first added bitcoin to its balance sheet.

Yet such rapid ascents come with hefty risks. Bitcoin remains highly volatile, even if the rollercoasters are less frequent. That raises questions about Strategy’s financial resilience and, even more so, about its many followers.

Capital dilution

In June 2025 Matthew Sigel, head of digital assets at VanEck, flagged risks tied to the “fashion” for corporate bitcoin treasuries.

No public BTC treasury company has traded below its Bitcoin NAV for a sustained period.

But at least one is now approaching parity.

As some of these companies raise capital through large at-the-market (ATM) programs to buy BTC, a risk is emerging: If the stock trades at or near…

— matthew sigel, recovering CFA (@matthew_sigel) June 16, 2025

In particular, he pointed to the threat of “capital dilution”—a situation in which a company’s value falls despite holding bitcoin on its books.

An important factor, he said, is how firms fund purchases: by issuing new shares or by taking on debt.

If shares trade at a premium to net asset value (NAV), additional issuance can be accretive—because the company raises more than it is worth. That is how Strategy proceeded, issuing stock and debt to top up its bitcoin reserves.

But the model holds only when asset prices are high. As the share price nears NAV, new issuance dilutes existing holders without adding value. Prices then fall—bitcoin holdings alone are not enough to prop up the stock.

Semler Scientific: when a bitcoin bet backfired

US medtech firm Semler Scientific drew plenty of attention—its shares surged right after it bought several hundred bitcoins, mimicking the new trend.

In May 2024, company representatives called digital gold “the primary treasury reserve asset” because it is “a reliable store of value and an attractive investment.”

By year-end the stock peaked above $70, but by mid-2025 it had dropped by more than 45%, despite the first cryptocurrency’s advance.

As of August 1, Semler Scientific holds 5,021 BTC, ranking 15th on BitcoinTreasuries. Its bitcoin reserves are worth roughly $576m, while the firm’s market capitalisation is about $491m.

This is a serious signal of investor distrust: the market values Semler below the worth of its bitcoin assets.

The episode underscores the risk of overreliance on a volatile asset. In an upswing it can boost corporate reserves, but it also magnifies instability and can weaken the company’s position, including its share price.

Absent a turnround, Semler will struggle to raise capital via new stock. At depressed prices, that would dilute existing shareholders.

“As a rule, when companies issue new stock they sell at the prevailing market price. If the price is low, it can dilute existing shareholders,” explained Cointelegraph analyst Dilip Kumar Patayrya.

Such a scenario arises when a company’s financial strategy ends up reducing its overall value, he added.

“In essence, the company risks losing investor trust, which can undermine its ability to grow and execute its business strategy for a long time,” the expert stressed.

Hidden risks

Sharp crypto-market crashes are not rare—they are statistically common. Corporate treasuries are exposed not only to the dominant asset’s volatility but to industry-wide failures.

“Systemic blockchain risks often stay out of sight. Mass liquidations, token interdependencies and outages at centralised exchanges can spark abrupt price collapses. These threats are rarely factored into traditional liquidity and treasury management,” noted Patayrya.

To operate successfully in such an environment, companies must keep a clear head and build robust risk frameworks. Otherwise the odds rise of capital erosion, shareholder dilution and even outright strategic failure, the expert warned.

Lehman’s collapse and the 2008 crisis in retrospect

On the eve of the 2007–08 financial crisis many banks chased rapid growth, leaning on borrowed money. Lehman Brothers and Bear Stearns, for instance, piled into risky mortgage paper and derivatives, relying on leverage.

When asset prices fell, the giants faced liquidity shortfalls and could not meet obligations—triggering a market chain reaction.

In September 2008, Lehman filed for bankruptcy. Bear Stearns, facing acute liquidity stress, was forced into a fire sale to JPMorgan Chase. Models predicated on rising prices worked only while markets headed north. When the trend turned, the system collapsed.

Companies buying bitcoin by issuing new equity and/or taking on debt face similar hazards. If crypto prices tumble, access to capital shrinks, debt burdens swell and room to manoeuvre vanishes. Banks and big insurers like AIG once found themselves in a comparable bind—having bet on complex derivatives, they ended up seeking state support.

The chief lesson: dangerous are not only excessive debt and leverage, but also euphoria. Confidence in endless gains dulls risk perception—fertile ground for severe destabilisation when markets move the “wrong” way.

A grim forecast

On-chain analyst James Check predicted that many Strategy imitators will crash. In his view, capitalisation built on corporate bitcoin reserves may be less robust than assumed.

For most recent entrants, it may already be “too late,” Check noted. Devotees of the “Strategy strategy” will find it harder to raise capital, as investors favour earlier adopters.

The expert agreed with Taproot Wizards co-founder Udi Wertheimer: many companies see bitcoin as a quick-profit tool, without engaging with its foundational idea.

A Blockware report notes that the most active buyers of digital gold are either new ventures or little-known loss-making firms.

“The corporate race for bitcoin is led mainly by either new companies or dying ones you have never heard of,” the analysts said.

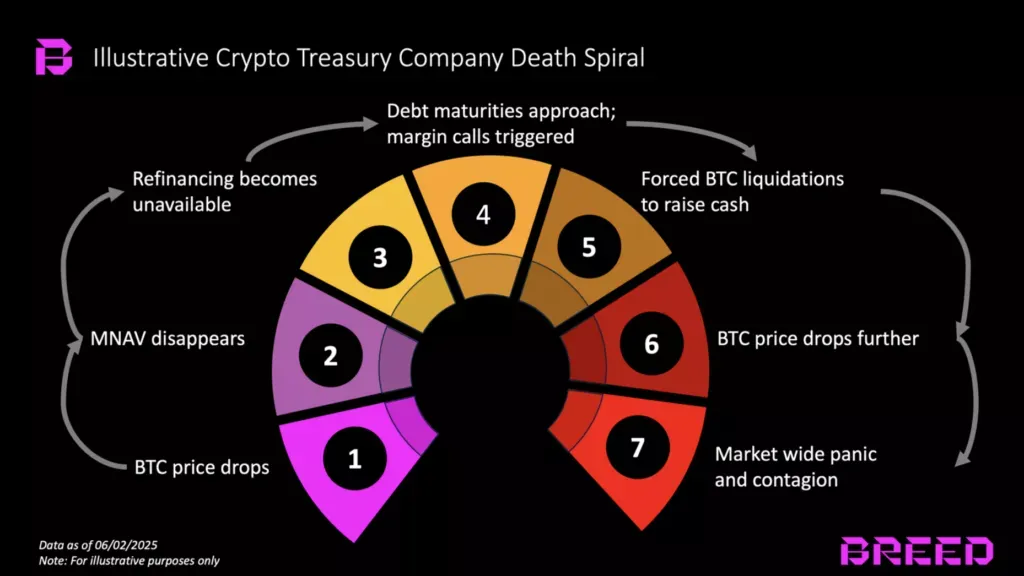

Venture firm Breed noted that only a handful of companies with bitcoin treasuries will remain resilient and avoid a “death spiral”. The latter threatens firms whose shares trade near NAV.

The need to refinance debt while capital-raising windows narrow will force such companies to sell reserves. Those sales would pressure bitcoin’s price and could set off a cascade, the authors believe.

I think we’re in a fairly advanced stage of the Bitcoin treasuries saga.

I’m also pretty confident they’ll play a key role in the next bear market.

The music stops when the NAV premium starts to slowly fall (or even turn negative with ATMs), and raises become smaller or fail… pic.twitter.com/tce5zjFMqY

— Saint Pump (@Saint_Pump) July 12, 2025

“I’m sure they [crypto reserves] will play an important role in the next bear market,” wrote the crypto trader known as Saint Pump.

Hyperbitcoinization

Blockstream chief Adam Back believes that, for speculators, investing in listed companies with bitcoin treasuries could be a lucrative alternative to altseason.

Such firms, he says, regularly add to their holdings of the first cryptocurrency, nudging their share prices upward and making the stocks appealing to investors.

Although proceeds are not always deployed straight into bitcoin, they allow companies to keep buying, which supports demand.

In April, Back said that corporate treasury purchases of the first cryptocurrency are driving steady “hyperbitcoinization”, lifting its market capitalisation to $100–200 trillion.

Blockware researchers expect at least 36 new public companies to add the first cryptocurrency to their balance sheets by end-2025.

“This is only the beginning. Over the next six months we expect no fewer than three dozen companies to put bitcoin in their treasuries,” the analysts suggested.

VanEck’s advice

VanEck’s Matthew Sigel urges “hyperbitcoinised” companies to act pre-emptively to avoid capital erosion. His proposals include:

- pause additional issuance. If the company’s shares trade for ten straight days below 95% of NAV, halt new offerings to avoid diluting shareholders;

- buybacks. If the share price lags bitcoin markedly, consider a buyback—to reduce the discount to NAV and concentrate ownership among fewer investors;

- rethink the approach. If shares trade below NAV for an extended period, it may be time to reimagine the business strategy. Options include a merger, a split or abandoning the current model altogether;

- align executive incentives. Management pay should depend on per-share value, not the absolute number of bitcoins on the balance sheet. That discourages over-accumulation and keeps focus on sustainable growth.

For his part, Dilip Kumar Patayrya recommends:

- be ready for volatility: bitcoin’s price can turn into a rollercoaster, especially amid global financial shocks or even announcements of “liberation tariffs” by Donald Trump;

- assess risk: despite its potential, bitcoin remains a high-risk asset, so it is unwise to concentrate an entire portfolio in it;

- avoid chasing quick wins: if you are investing for long-term growth, do not react impulsively to temporary drawdowns (though sharp drops can indeed inflict heavy losses);

- plan risk management: define your playbook in advance: set key levels and outline entry and exit points.

Conclusions

Companies holding bitcoin in treasury draw media attention and are often seen as more innovative and promising.

Semler’s example shows that even in a bull phase shares can fall. Without a thoughtful plan, “hyperbitcoinization” risks sizeable financial losses.

VanEck’s advice is grounded not in guesswork but in experience from both traditional finance and crypto.

In the end, it is not who holds the most digital gold that matters, but who can endure the downturn and consolidation while preserving the company’s fundamentals.