In 2025 the sector of decentralised derivatives became the main driver of the DeFi market. In September alone, total monthly trading volume on perp-DEX exceeded $1 trillion. By comparison, over the whole of last year the top ten venues processed $1.5 trillion in orders.

Yet behind these numbers lie not only technological breakthroughs but also old marketing tricks: incentives such as airdrops farming and, at times, dubious metrics.

ForkLog traces the evolution of crypto-derivatives exchanges and examines what underpins the perp-DEX trend.

A centralised foundation

The popularity of daily liquidation-volume metrics owes much to crypto futures.

In 2016 the centralised crypto-derivatives exchange BitMEX became the first venue to offer trading in perpetual contracts (perpetual swaps). Since then, 100x leverage on bitcoin using the XBTUSD contract has been the platform’s calling card.

Founded in 2014 with the involvement of Arthur Hayes, the exchange initially targeted professional traders and offered margin and settlement in BTC only, with 3x and 5x leverage. Since 2022 it has also supported USDT.

Hayes adapted principles from interest-rate swaps and cash-and-carry arbitrage in traditional markets. The key to perpetual contracts is the funding rate—a mechanism that keeps futures prices aligned with spot.

The funding rate in crypto trading is a periodic payment exchanged by holders of long and short positions on a contract. The mechanism requires traders holding the dominant side to pay a percentage to the opposite side every eight hours.

With a positive funding rate, longs pay shorts; with a negative rate, shorts pay longs.

Over nine years BitMEX lost its lead amid intense competition and a series of lawsuits and criminal investigations targeting its top managers. According to Coingecko, at the time of writing the CEX ranks 33rd by open interest among crypto-derivatives exchanges, with around $1 billion in daily turnover.

In 2019 Changpeng Zhao (CZ) launched a BitMEX analogue—Binance Futures. Within weeks it raised leverage on BTCUSDT to 125x, overtaking Hayes’s firm. On October 8, 2025, daily trading volume on Binance Futures neared $120 billion.

Borrowing the best

2020 was the year decentralised finance blossomed. From May to September the sector’s TVL rose from $1 billion to $10 billion as users flocked to DEXs and lending platforms such as Aave and Curve. The “DeFi summer” culminated in the launch of yEarn Finance and a generous airdrop of UNI.

In October 2020 a criminal case alleging violations of bank secrecy and AML/KYC procedures against BitMEX sparked widespread attention. Market participants realised that regulation could reach anyone. Against this backdrop DeFi looked even more attractive, operating in a “grey zone” that left legal loopholes.

That same year saw the release of the first perp DEXs, whose chief aim was to combine non-custodial storage with convenient UX.

Decentralised futures platforms had to embed their mechanics in a blockchain without the server farms of a CEX. First-wave projects managed to squeeze order handling, margin, PnL and liquidations into Ethereum blocks. The network became the base of DeFi, but its throughput and high transaction costs were both a weakness and a spur to build the next generation using L2 and dedicated blockchains.

The first two perp DEXs—dYdX and Perpetual Protocol—set the tone, splitting development into two branches:

- order book. dYdX used a modified CEX-style order-processing model, relying on external services, such as “liquidation execution”. Developers of the popular Hyperliquid on its own L1 took a similar path;

- vAMM. Perpetual Protocol used a mechanism that mimics an AMM without holding real token reserves. A vAMM creates virtual liquidity via parameters in smart contracts, without the need for direct liquidity providers. GMX adopted such an approach.

Porting Perpetual Protocol v2 to Optimism proved pivotal: fees fell by orders of magnitude and the UX moved closer to centralised solutions. In 2024 dYdX, after experimenting on Ethereum L2s, launched its own network based on the Cosmos SDK with an independent order book.

Other protocols adopted hybrid architectures: off-chain orders combined with on-chain settlement, with some adding AMM mechanics. In dYdX v4, to maintain high order-intake speed, the order book is processed off-chain while positions and settlement are recorded on-chain.

Thus a new generation of fast, modular perp DEXs emerged.

Speed, convenience or safety

In effect, all perp DEXs aim to be as fast and convenient as CEXs while enabling self-custody and avoiding KYC.

In competing with leading centralised exchanges, developers have found a compromise in the HotStuff consensus mechanism, used in various iterations by blockchains such as Plasma, Monad, Aptos, Sui. This architecture enables record throughput but does not match Ethereum’s security.

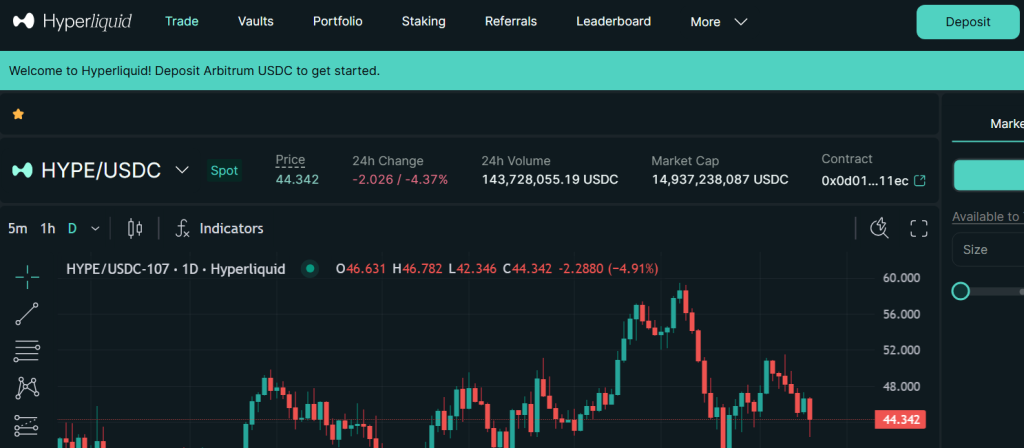

Using such a consensus, Hyperliquid has become the flagship of the new perp-DEX wave. It has approached CEX-like speed on its own L1 network based on the Cosmos SDK. Notably, the team managed to deploy the order book fully on-chain. The design has delivered depth of liquidity for large traders. The interface recalls popular venues such as Binance and Bybit.

Unusually for a DEX, there is a “deposit” button, as most operations on decentralised platforms are executed directly from MetaMask or Phantom. Registration creates an operational wallet with restricted token-transfer functions and no fees. It is built solely for trading, which also benefits order-processing speed. Funds in USDC can be bridged from Arbitrum. The venue supports native Bitcoin and Ethereum.

In its first year Hyperliquid faced a string of problems and scandals. There were accusations of validator centralisation, DAO governance issues and contentious management decisions.

Other teams in DeFi have also taken unpopular steps after feeling the limitations of L2s and the insufficient security of sidechains.

In June 2025 the L2 Synthetix decided to return to basics because of fragmented liquidity and the difficulty of designing an economy across multiple networks.

In turn, Synthetix concluded that to win it must fully control the user experience: offer an order book instead of an AMM and deploy on Ethereum mainnet rather than an L2.

“Despite years of attempts to make on-chain AMMs work for perpetual contracts, order books provide better liquidity and a more comfortable experience for traders. While order books cannot yet be fully implemented on L1, Ethereum remains the best venue for asset custody and settlement, without bridge risks and liquidity fragmentation”, — the Synthetix blog says.

To return to mainnet with a new perp DEX, the team will apply an architecture unlike previous ones: off-chain order matching with secure on-chain custody.

In August 2025 it also was reported that the gaming blockchain platform Ronin was returning to Ethereum. The team made the decision after a string of cross-chain bridge hacks, one of which was the largest in history.

Old marketing

The success of the leading perp DEX Hyperliquid stems above all from a well-executed airdrop. Average rewards ran to thousands of dollars, and users were in no hurry to part with their HYPE. The team restored users’ faith in the power of airdrops.

After Hyperliquid’s successful case, a wave became a trend. The decentralised exchange for perpetual contracts Aster, with CZ’s help, managed to overtake the leader by trading volume.

The venue used tried-and-tested point-based user-acquisition mechanics, and Zhao’s involvement lent weight to the campaign. Within days of its September launch, the market capitalisation of the ASTER token reached several billion dollars, sparking a noticeable frenzy.

The exchange attracts users with trading in US stock-market equities. A standout feature was leverage of 1001x on the BTCUSD contract, beating previous records by a wide margin.

Such an approach raises many questions, chief among them the speed of decision-making. Even at earlier highs of 100–200x, humans struggle: leverage can drain an inexperienced trader’s wallet in seconds.

Perhaps the functionality is aimed at future AI-driven trading, already visible on exchanges via automated strategies. Aster plans to build a high-performance layer-1 blockchain focused on anonymity.

The founder of TRON, Justin Sun, also joined the trend, announcing on October 1 the launch of the futures platform SunPerp.

Amazing first day!🙌

Great to see @Trondao lead the way as Title Sponsor at @Token2049 and get the opportunity to share the launch of @Sunperp_Dex with the community today! https://t.co/R8Z8UQYp8O

— H.E. Justin Sun 👨🚀 🌞 (@justinsuntron) October 1, 2025

The hype was picked up by the Lighter exchange, which uses ZKP technology for verification. On October 2 the team announced the launch of mainnet on Arbitrum. Notably, many perp DEXs have placed their trust in this blockchain, starting with GMX.

During Lighter’s activity-farming campaign, points surged on pre-sales markets. On October 9, the price per point in season two nearly reached $100.

Pacifica—a new perp DEX in testing on Solana—aims to deliver trading performance with AI-based tools. Its points programme is slated to last roughly six months. Early access is by invitation.

The other side

On October 5 Aster was suspected of inflating trading statistics. As with Hyperliquid, numerous instances of platform manipulation did not reverse the overall trajectory. As long as perp DEXs offer profits, the community pays little heed to problems. A few are worth noting:

- centralised order matching. Despite some claims of on-chain trading, parts of the process often run off-chain. Operators’ servers accept orders and carry out liquidations without a public record. If a node is unavailable or an attacker reorders priority, the user has no evidence;

- liquidation mechanisms and funding rates. Protocols use their own algorithms for rates and liquidation thresholds. The lack of a single standard raises the risk of sudden “cascading liquidations” during volatility spikes;

- incentives as a toxic engine. Trading bonuses and fee rebates create false liquidity. When incentives end, volumes often drop sharply;

- regulatory uncertainty. For the CFTC, perpetuals remain full-fledged derivatives. On-chain execution does not remove potential liability. Regulators may look away for now, but the dYdX case showed that once volumes near centralised levels, watchdogs start to pay attention.