Key Highlights

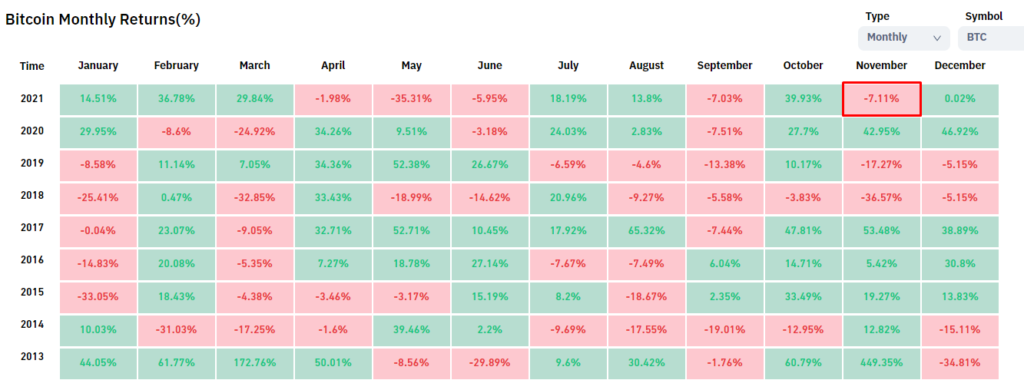

- Bitcoin corrected after an all-time high near $69,000, breaking the year-end pattern.

- Metaverse sector tokens continued to rise, with gaming platforms drawing a substantial user base.

- Since the London upgrade, the Ethereum network has burned more than 1 million ETH. The pace at which ETH is removed from circulation is increasing.

- Bitcoin futures open interest reached a peak as prices hit new highs.

- Total value locked in DeFi hit an all-time high above $275 billion.

- Trading volume on DEXes reached $113 billion, the second-largest on record in their history.

- The main driver of growth for Layer-2 solutions was the Boba Network project. Its TVL in November rose by 2,700% — aided by the BOBA token airdrop.

- Aggregate market capitalization of stablecoins reached $133 billion, with USDC’s issuance pace outpacing USDT.

Movement of Leading Assets

- In the first half of November, leading cryptocurrencies hit all-time highs.

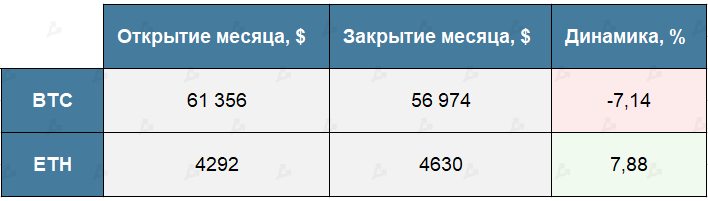

- Bitcoin traded at $69,000, and Ethereum at $4,868.

- Bitcoin fell 7.14% in November, while Ethereum rose 7.88%.

- Bitcoin broke the usual year-end pattern — PlanB’s Stock-to-Flow model author admitted the model’s worst-case scenario was untenable, which predicted Bitcoin would hit $98,000 in November. PlanB gave the Floor model one more month and reminded that Stock-to-Flow remains relevant.

- Best performers among mid-cap projects in November were GameFi tokens Sandbox (SAND), Decentraland (MANA) and newcomer Gala (GALA) — all hit new highs ($8.4, $5.9 and $0.84 respectively). Loopring (LRC) also stood out among high-cap projects, rising to a fresh high near $3.85 at month’s start.

- Impressive moves from Avalanche (AVAX) and Crypto.com (CRO) — both hit new highs at $147 and $0.97 respectively.

- Terra (LUNA) fell throughout November and posted a price peak of $60 on the last day of the month, amid votes to allocate $6 million in LUNA tokens for liquidity programs to popularize the algorithmic stablecoin Terra USD (UST).

- Among the laggards were the Cream Finance (CREAM) DeFi token on the verge of multiple hacker incidents and OMG Network (OMG), dumped by investors after the BOBA airdrop, as well as SushiSwap (SUSHI) losing a third of its value.

Crypto-linked Stocks

MicroStrategy (MSTR):

+0.06%

Coinbase (COIN):

-3.01%

Bakkt (BKKT):

-60.66%

Galaxy Digital (GLXY):

-10.48%

Mining Stocks Performance

Canaan (CAN):

+0.69%

Ebang International (EBON):

-31.94%

Riot Blockchain (RIOT):

+36.79%

Hut 8 (HUT):

-11.66%

Marathon Digital (MARA):

-2.43%

Crypto- and mining-related stocks in November mostly declined in line with Bitcoin, with MicroStrategy bucking the trend after another Bitcoin purchase worth $414 million; Canaan and Riot Blockchain also stood out.

Macroeconomics Backdrop

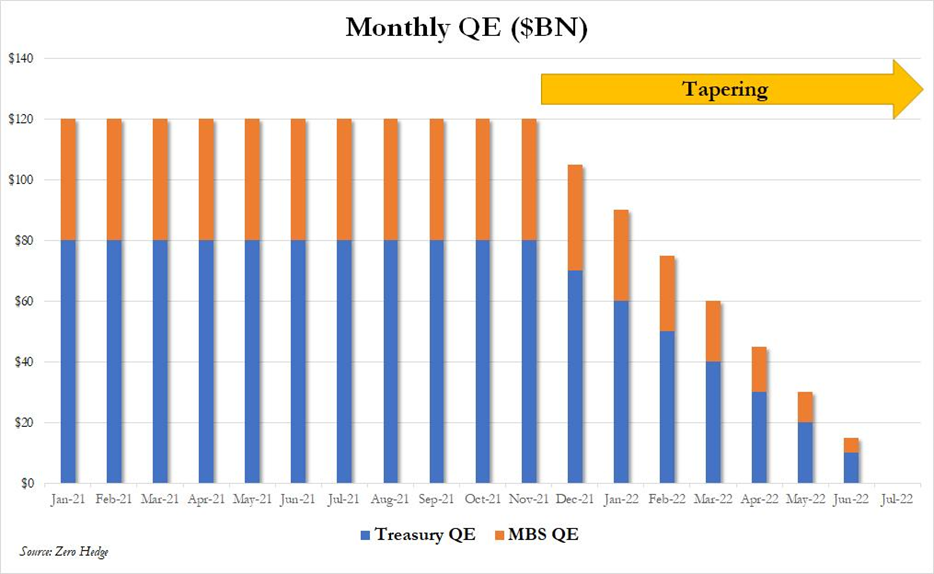

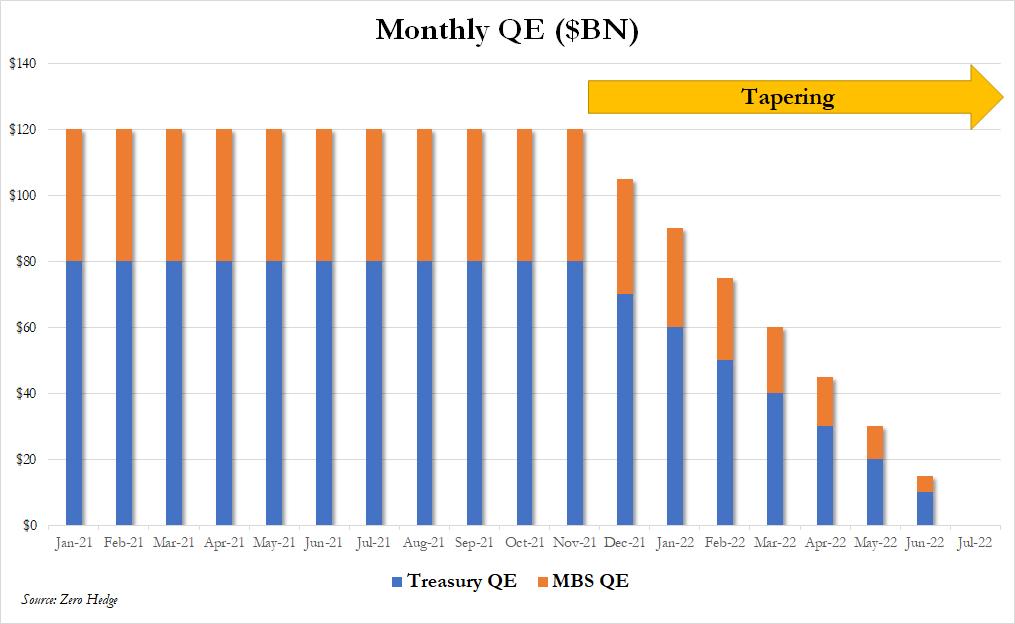

- As a result of the November 3 meeting, the Fed announced the start of tapering asset purchases by $15 billion per month — from November to June 2022.

- Inflation accelerated in October to 6.2%, a 30-year high, prompting a tougher stance on policy normalization from U.S. central bankers.

- In a November 30 Senate appearance, Chair Jerome Powell rejected the characterization of the inflation surge as temporary. He also signaled the possibility of winding down asset purchases “earlier than expected” for several months.

- Such statements emerged as the Omicron variant appeared, which had previously contributed to expectations of slower policy normalization by the Fed.

- Powell explained that ahead of the December 14-15 meeting, the committee would receive an assessment of risks from the new variant and macro data with the jobs report.

- Powell’s remarks tempered the Omicron-driven perception of timing for rate hikes. By the end of November, investors began pricing in September 2022 as the first hike rather than June, and they reduced the number of expected moves for the year from three to two.

- The prospect of quicker policy tightening by the Fed nudged traditional markets and Bitcoin toward a moderate correction.

Market Sentiment, Correlations and Volatility

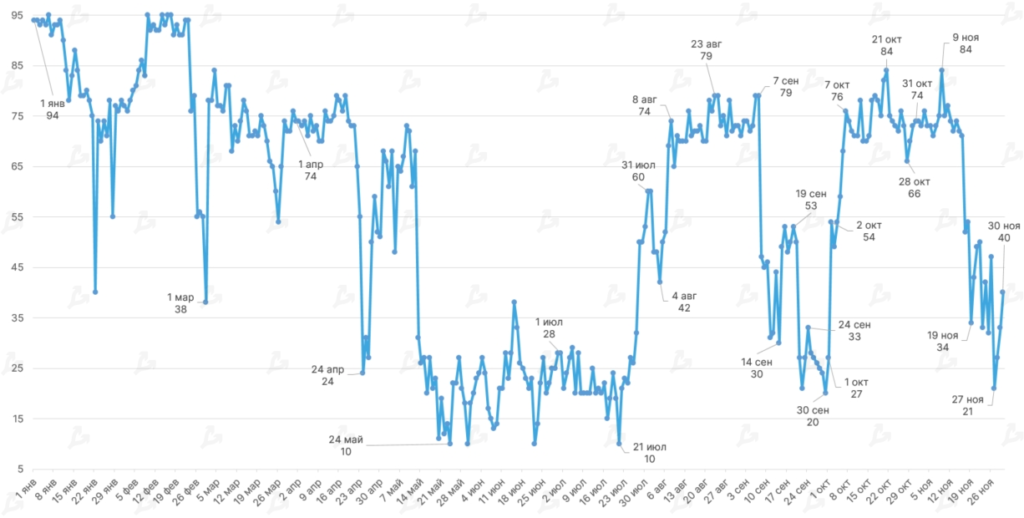

- Early in the month, market sentiment was bullish. On November 9, the Fear & Greed Index peaked at 84 — the same day Bitcoin climbed above $68,500. But the index began to drop afterward, foreshadowing Bitcoin’s moves.

- On November 27, the index fell to a two-month low of 21 — Bitcoin briefly traded around $53,500.

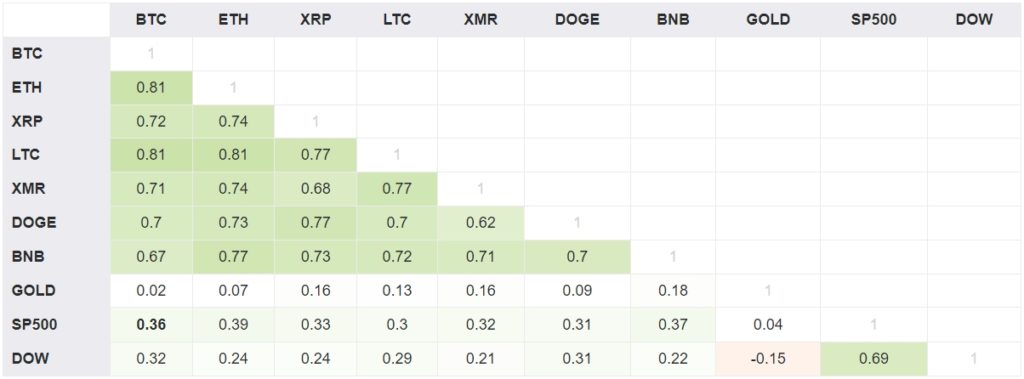

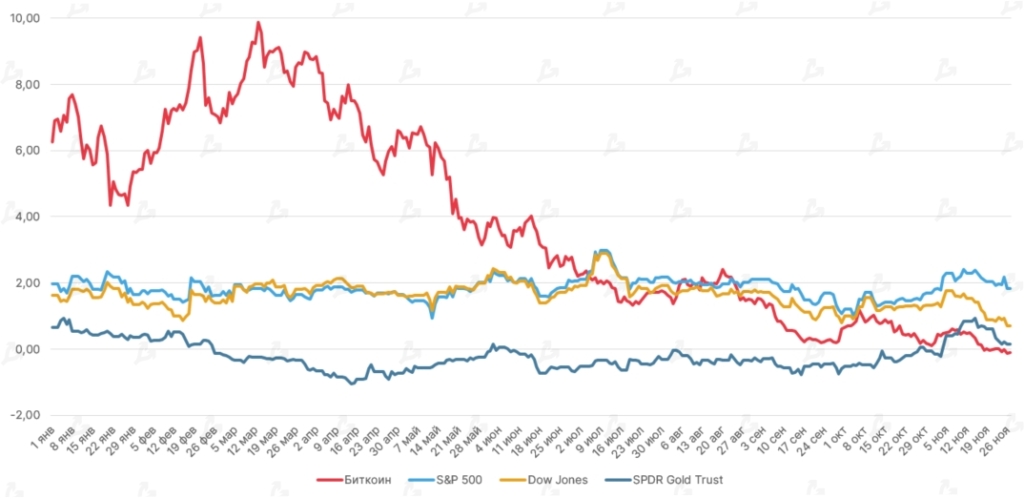

- Bitcoin’s correlation with gold turned positive, but the statistical linkage remains modest (0.02).

- The price movements of Bitcoin and the S&P 500 and Dow Jones indexes stay in the same direction, a trend that has strengthened for the third straight month. Possible reason: the emergence of crypto ETFs in the U.S. market.

- Correlation with the S&P 500 is stronger (0.36; with the Dow Jones — 0.32).

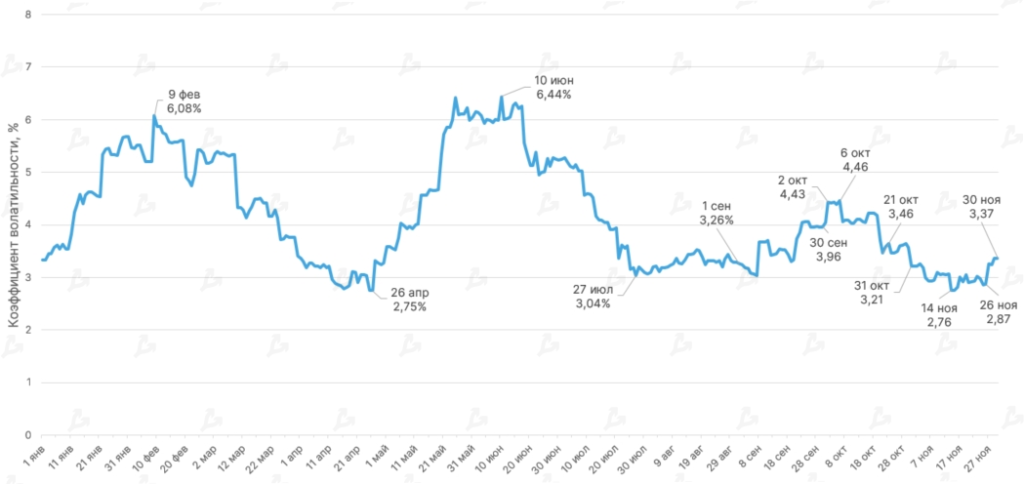

- The Bitcoin historical volatility index hovered in the 2.76% to 3.37% range in November, rising toward month-end. Price volatility remained moderate; during winter rallies or spring corrections it typically exceeded 4%.

- The Sharpe ratio (risk-adjusted return, using two-year US Treasuries as the risk-free rate) for Bitcoin remained above gold all year, but November reversed the trend. Investors’ risk tolerance was well compensated by BTC’s high returns.

On-Chain Data

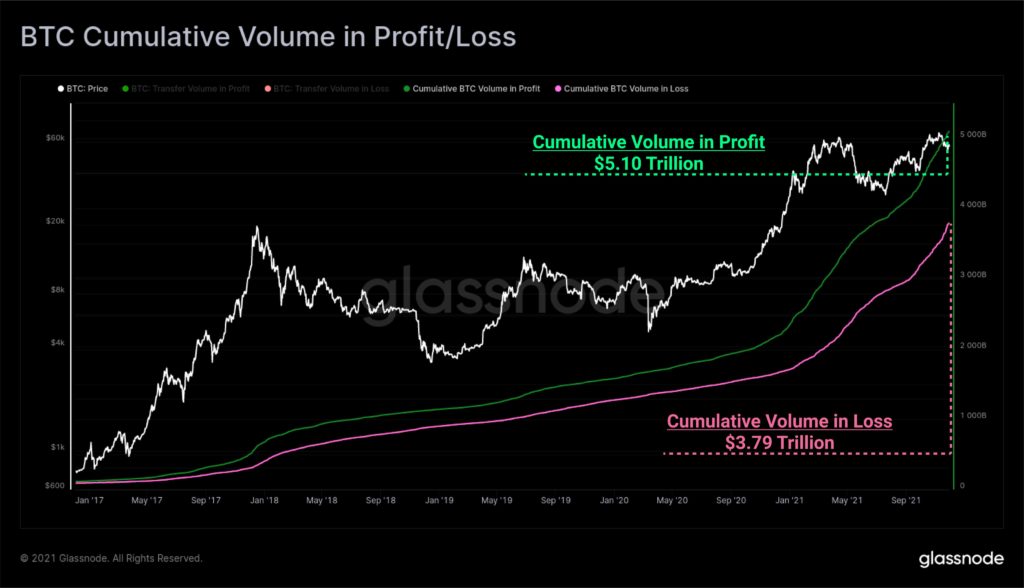

- Since the creation of the first cryptocurrency, the value transferred through its blockchain has reached $8.89 trillion. Of this, the value of profitable coins totaled $5.10 trillion, unprofitable $3.79 trillion.

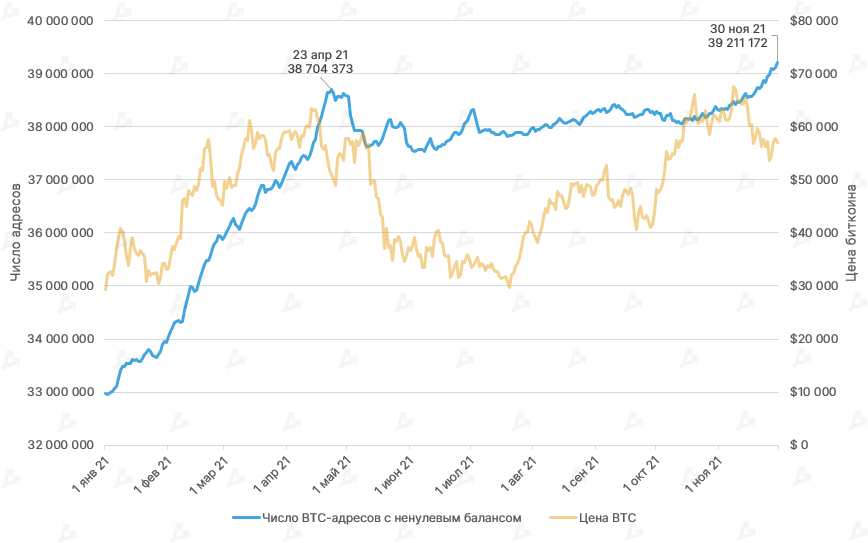

- The number of non-zero balance addresses in November hit a record 39.21 million. The previous high was in April — 38.7 million. The rise may indicate growing retail user activity and overall on-chain activity.

- Since activation of EIP-1559 in August, Ethereum has burned over one million ETH (~$5.12B) — of which more than 362,000 ETH in November (~$1.72B). The pace of ETH burn is rising: September 249,000 ETH, October 297,000 ETH.

- In the first half of 2022, Ethereum’s supply could reach a maximum of 119.7M ETH, after which the cryptocurrency could become deflationary.

- The trend of decreasing ETH balances on centralized exchanges (CEX) continued for a third month alongside rising ETH price. In November, ETH on exchanges fell by 3.5% since the start of the month and by 13.3% year-to-date.

- The share of ETH locked in smart contracts of decentralized apps remains high — since August, the share has not fallen below 26%.

- The reduction in CEX balances coincides with ETH price growth; over the past 30 days, ETH rose by 9.65%.

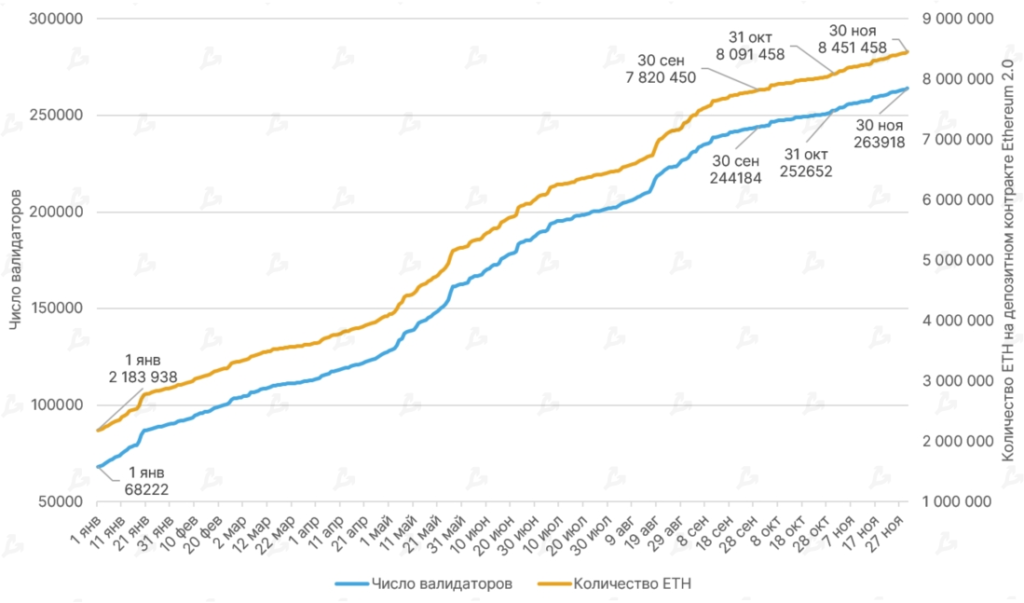

- In November, the Beacon Chain validators approached 264,000. Community members interacted more actively with Ethereum 2.0; the number of validators grew by 4.5% month-on-month (October: 3.3%).

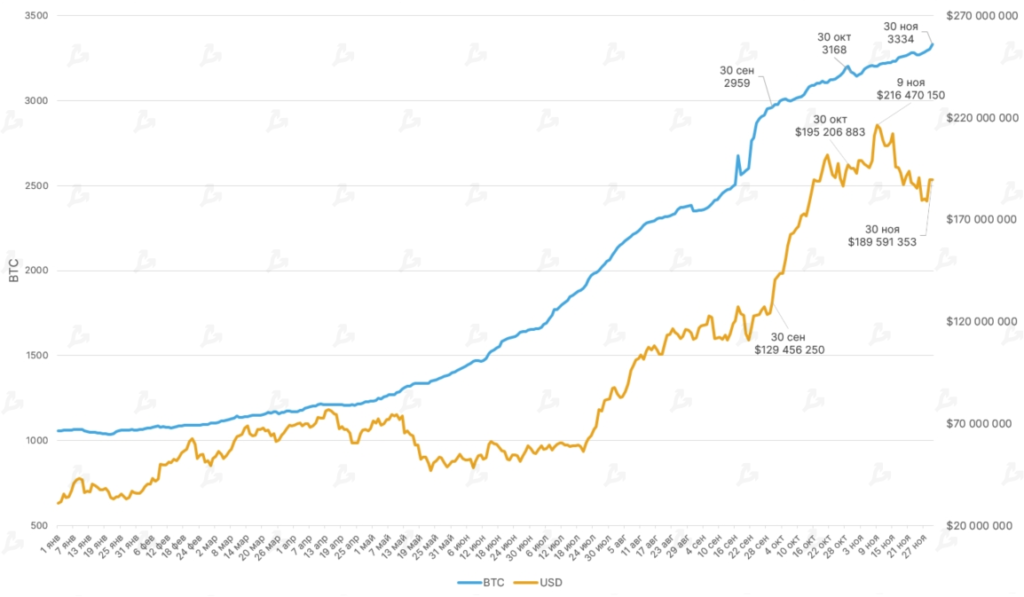

- The number of ETH on the deposit contract rose to over 8.45 million (+4.5% month-on-month). The total value of this ETH is around $40 billion.

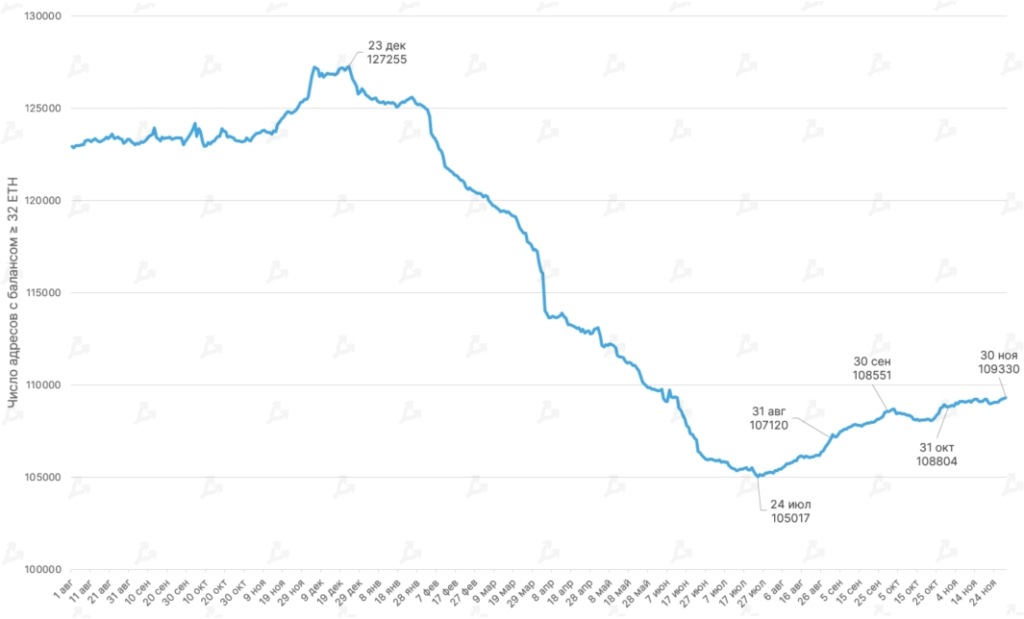

- The number of addresses with balance ≥ 32 ETH rose for the fourth consecutive month; by November 30, it reached 109,330.

Lightning Network

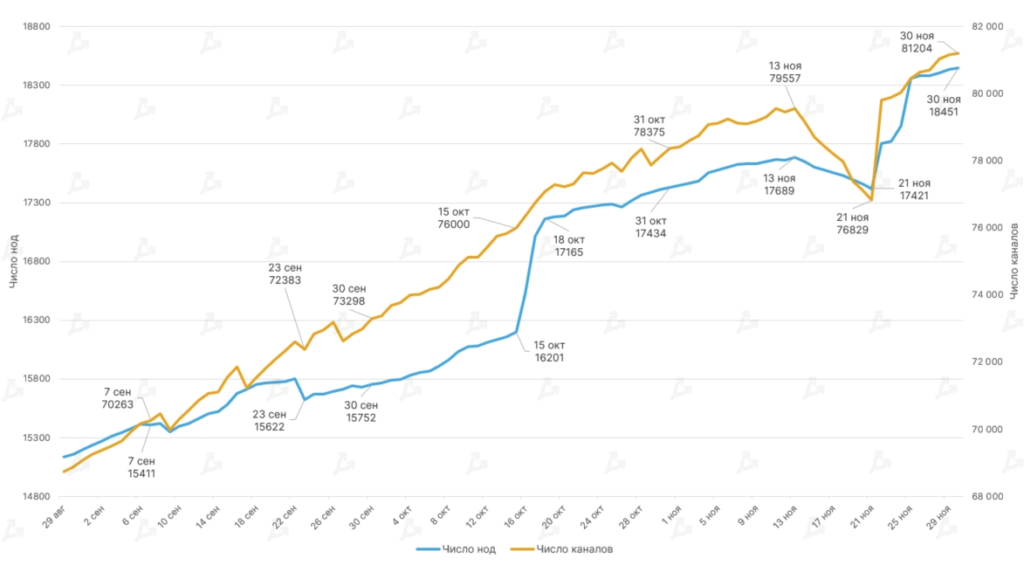

- In November, LN’s number of nodes and channels continued to grow: the first metric rose 6% and the second 3.6%. October gains were 10.5% and 7%, respectively.

- During November LN capacity rose by 5.2% to 3334 BTC. In the previous month the growth was 6.9%. Both metrics lagged September’s, when capacity expanded by 25% after the legalisation of Bitcoin in El Salvador.

Mining, Hashrate, Fees

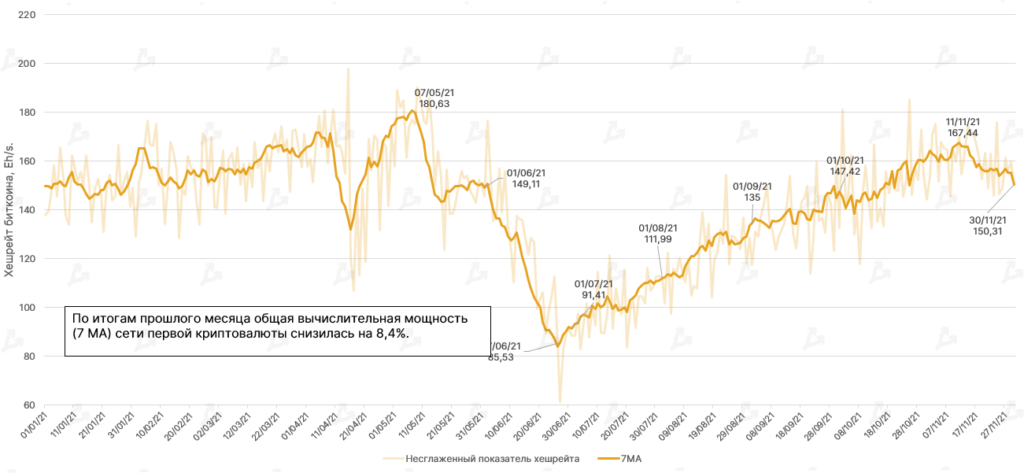

- Bitcoin hashrate broadly declined by 8.4% month-over-month (smoothed over a 7-day average).

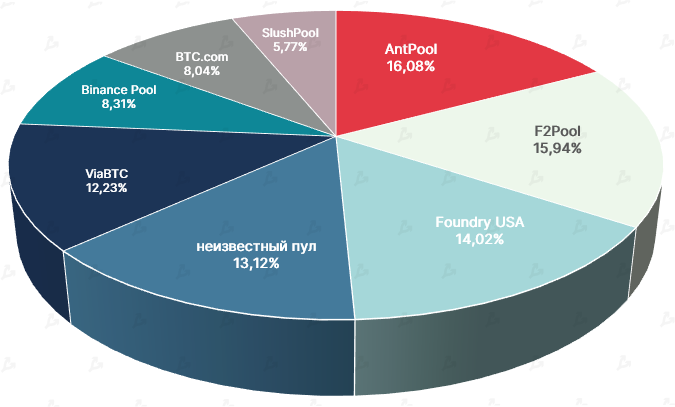

- The largest share of hashrate comes from AntPool. Mid-month, American mining pool Foundry briefly led, its share briefly exceeded 21%.

- At the last re-calculation (28 November) Bitcoin difficulty dipped 1.49%. The metric had risen in the previous nine periods.

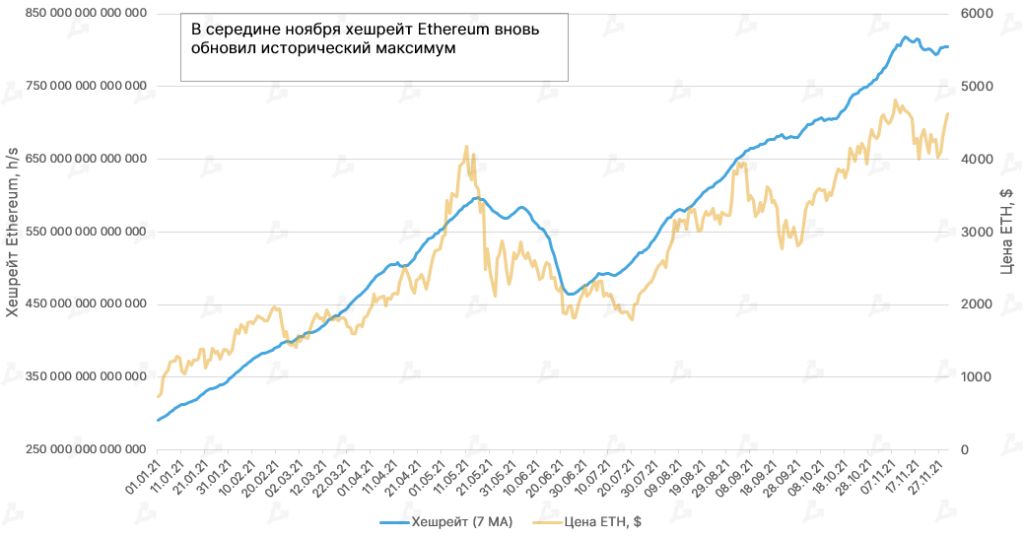

- By 12 November, the smoothed seven-day average Bitcoin hash rate reached a record 818.39 TH/s, following the rise of ETH above $4,700.

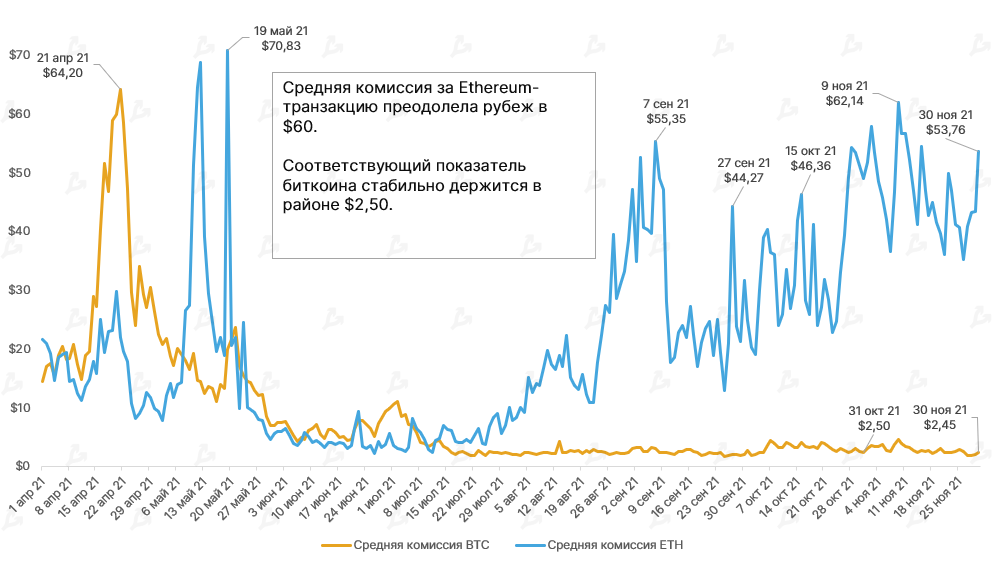

- In early November, the average ETH transaction fee surpassed $60, a level not seen since April and May.

- In the first half of November, the average Bitcoin transaction fee hovered around $3–$4. After the Taproot activation, it briefly rose above $3 on November 20, generally staying near $2.50.

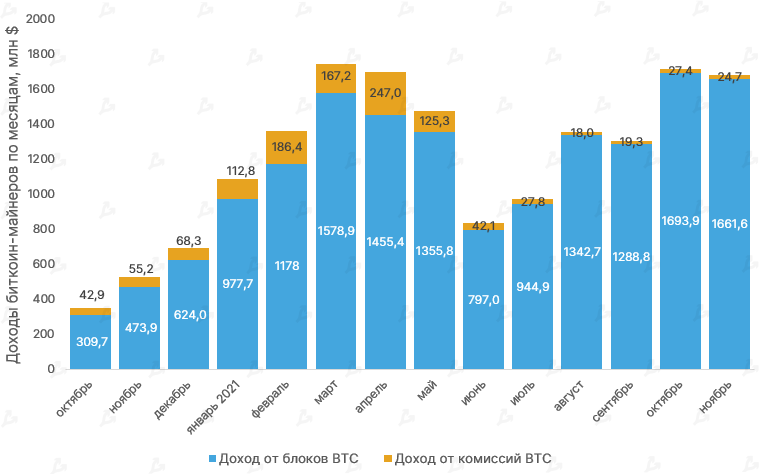

- Bitcoin miners earned $1.68 billion. This was 2% lower than the previous month. The share of fees in total revenue was only 1.48%.

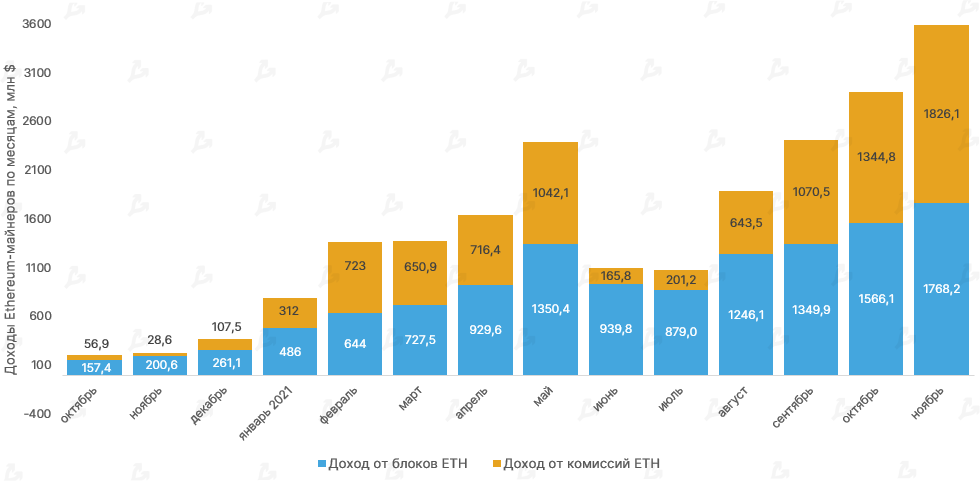

- November’s Ethereum miners’ revenue was a record $3.59 billion. Fees from ETH transactions accounted for more than half of total revenue — $1.82 billion.

- The last time such a ratio occurred was February. The high share of fees underscores the ongoing scaling challenge for Ethereum.

Trading Volume

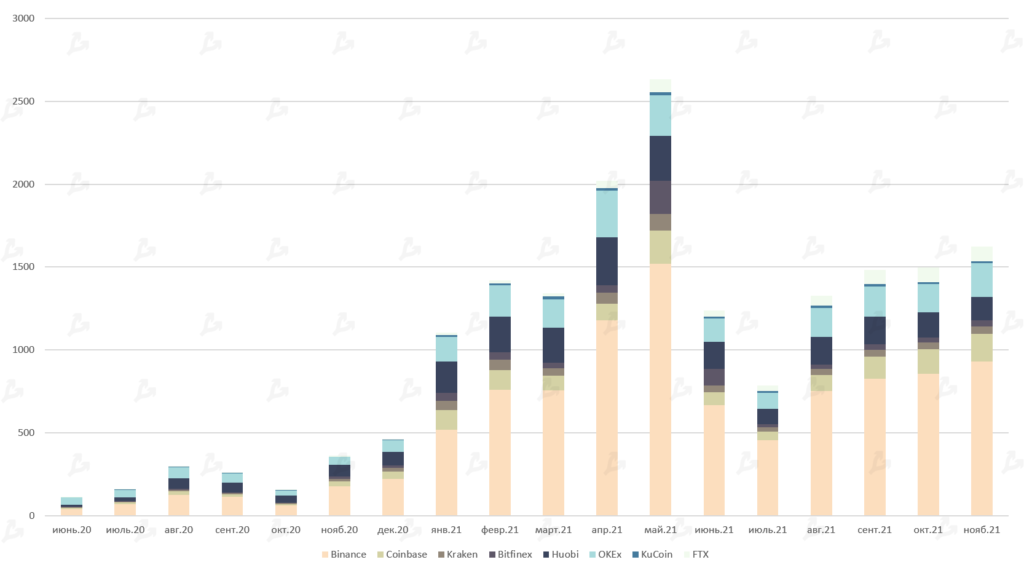

- November saw a continued recovery in trading volume on leading crypto exchanges. The total reached $1.62 trillion, the third largest figure in 2021.

- Coinbase displaced Huobi to third place in the ranking ($167B vs. $143B). The top two places remained Binance ($931B) and OKEx ($204B).

Futures and Options

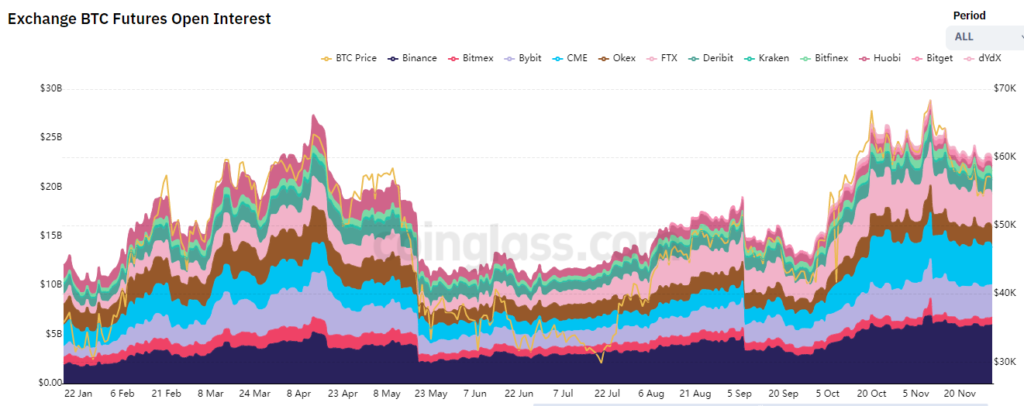

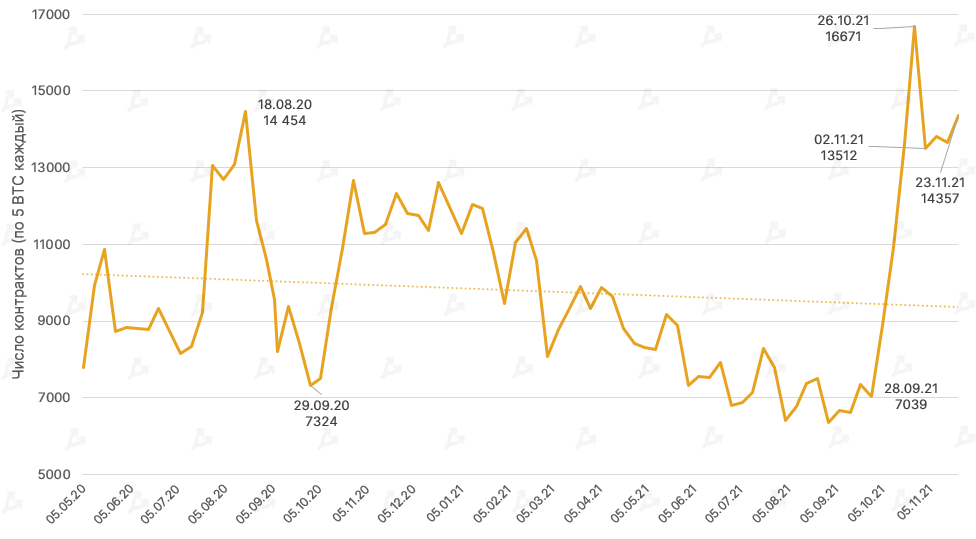

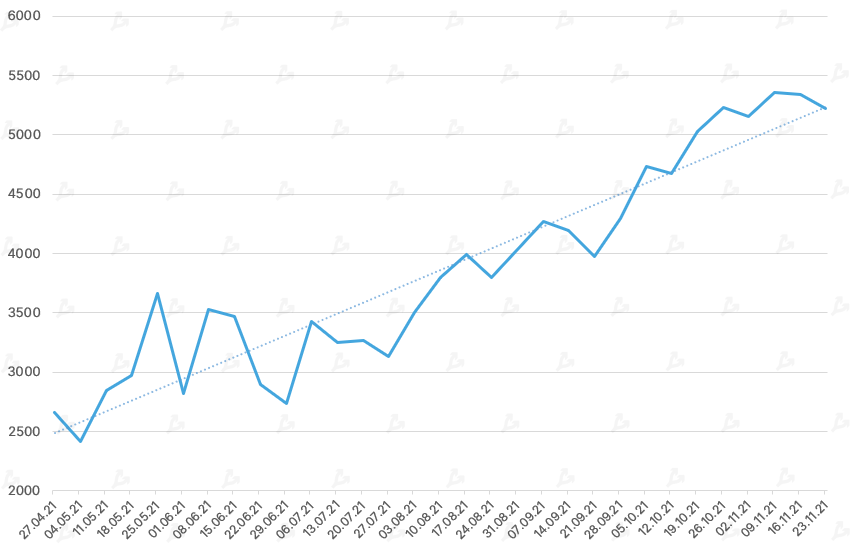

- Total open interest (OI) in Bitcoin futures in November hit a new high — November 10 it reached $28.8B. Bitcoin also posted a fresh high above $69,000.

- By month-end OI had declined by 20% to $23B. CME now holds the second-largest share ($3.8B), while Binance leads with $6B.

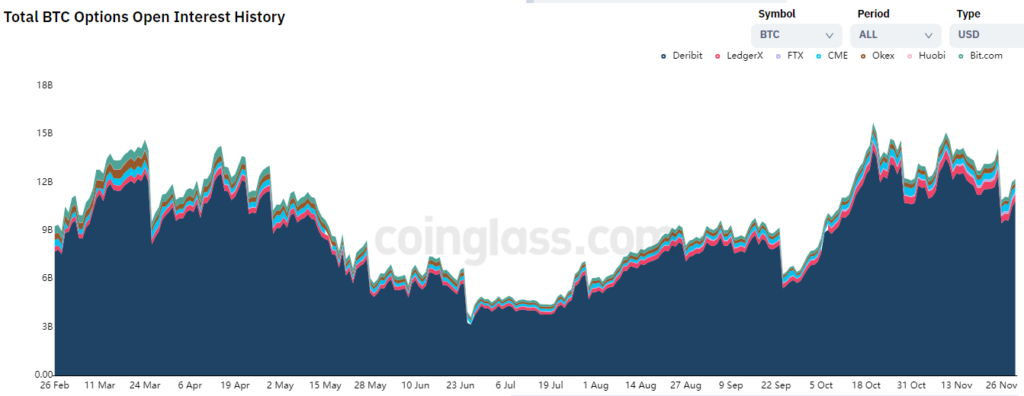

- November’s total Bitcoin options volume reached $25 billion. Deribit remained the leader, accounting for 88% of activity.

- Open interest in Bitcoin options approached October’s record ($15.7B) and declined by more than 20% during the expiry of contracts in the last week of November.

DeFi

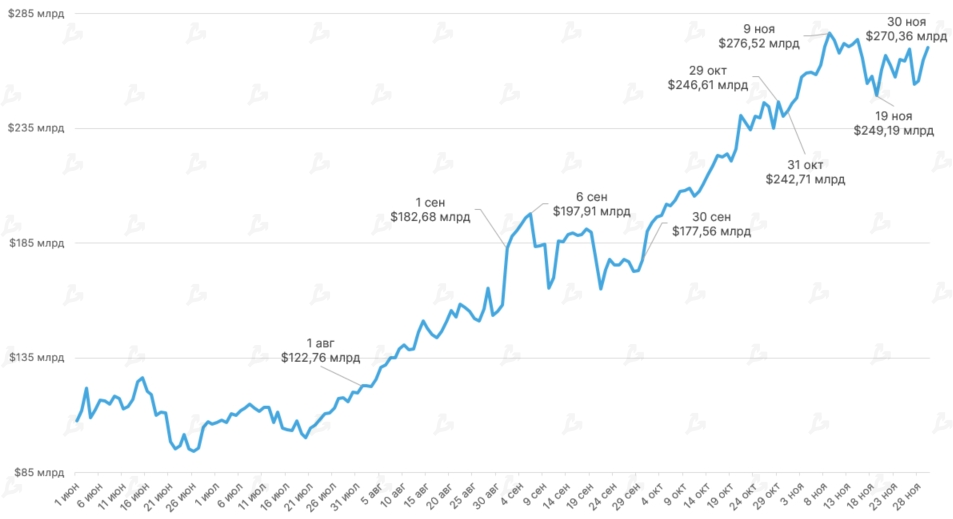

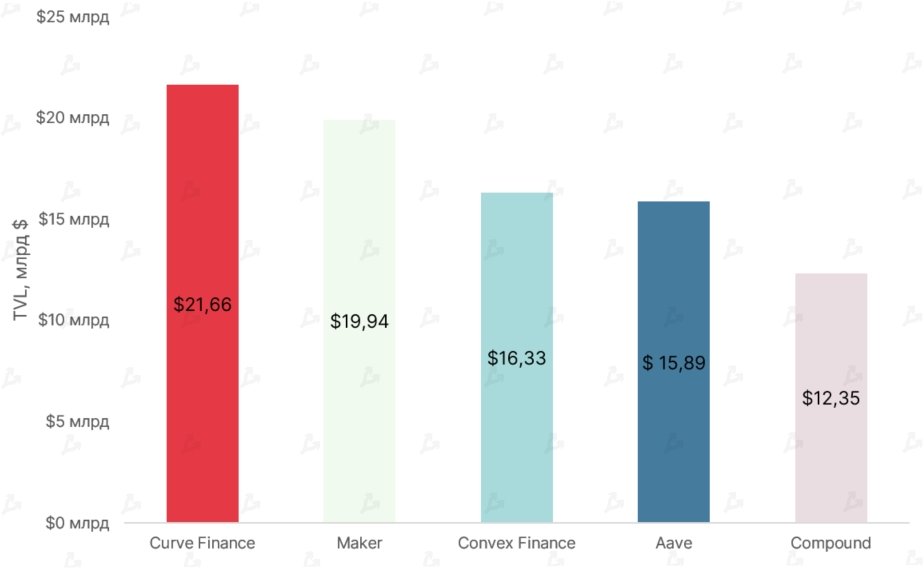

- In November, TVL in DeFi reached a new high above $275B. Over the last 30 days, the metric rose 11.4% to finish at $270.36B.

- Curve Finance remains the leader with TVL of $21.66B (+12% month-on-month). Ethereum accounts for most of the TVL ($19.18B), followed by Avalanche ($1.15B).

- Compound returned to the fifth spot in Ethereum-based projects, displacing InstaDApp.

- Convex Finance TVL rose 18% to $16.33B, with a new entrant taking third place in this ranking.

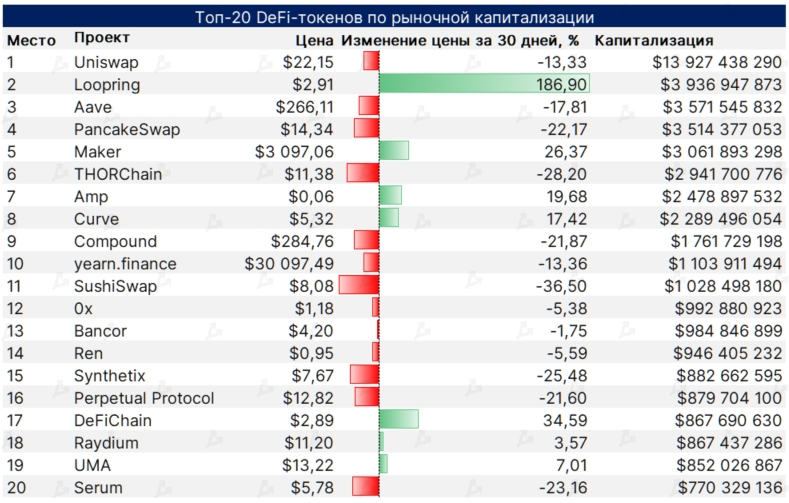

- Amid ongoing speculative chatter around Loopring’s partnership with GameStop, its native token continued to rally, up nearly 187% in 30 days. The high fees on Ethereum may have contributed, as Loopring offers gasless trades and monthly volume exceeded $3B.

- The Maker token MKR rose more than 26%. The MKR rally was accompanied by more addresses with non-zero balance and increased on-chain activity and decentralization.

- The DeFiChain native token surged over 34%, entering the DeFi top-20 by market cap. Factors included more masternodes freezing DFI for a 10-year period and rising TVL ($1B+ in November). As of Nov 1, the project’s community had locked more than 40 million DFI.

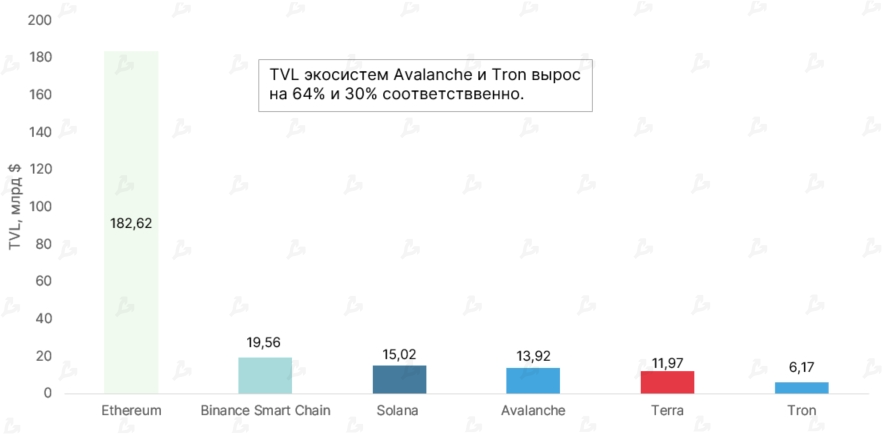

- TVL for the Ethereum ecosystem rose 11% in November — it remains dominant in DeFi with a figure of $182.62B.

- Strongest inflows occurred in Avalanche (+64%) and Tron (+30%). This enabled Tron to surpass Fantom, whose TVL barely changed in November (+0.18%), ranking it 6th.

- Fantom’s modest performance may reflect a decline in TVL for lending platform Geist Finance. After launching in October, its TVL surged to $3.59B but finished November at only $870M.

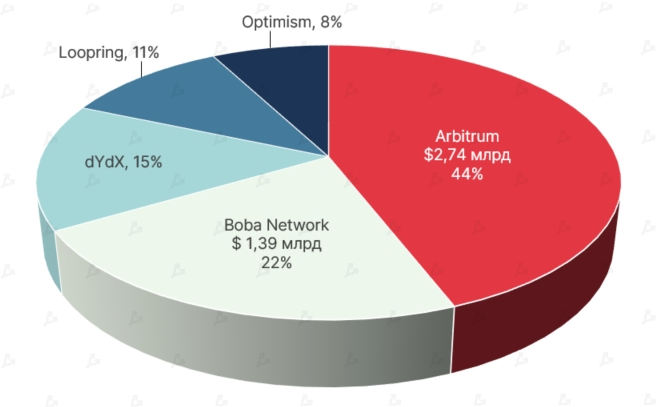

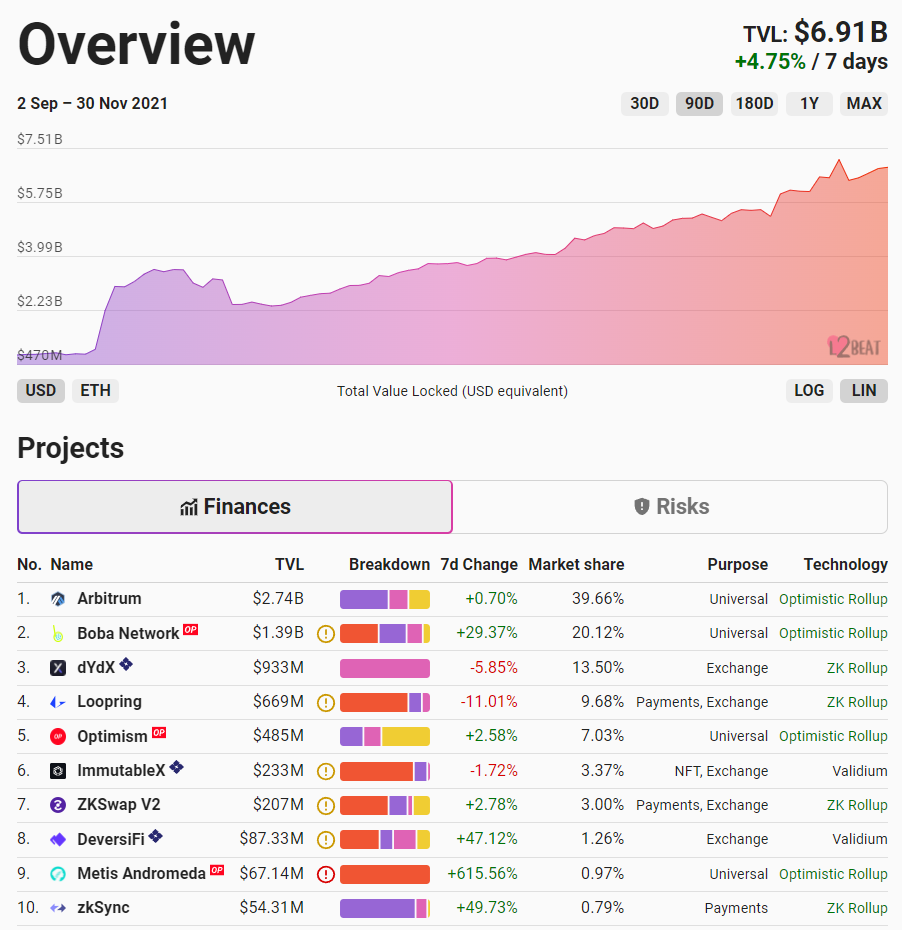

- Aggregate TVL for Layer-2 scaling solutions in November surpassed $7B, led by Arbitrum, whose monthly figure dipped slightly to $2.74B from $2.8B in October, with Boba Network driving growth.

- Boba Network — an Ethereum Layer-2 solution based on Optimistic rollups launched in August 2021 — TVL reached $1.39B, up 2,700% in November. This was aided by the BOBA token airdrop supported by Binance and FTX.

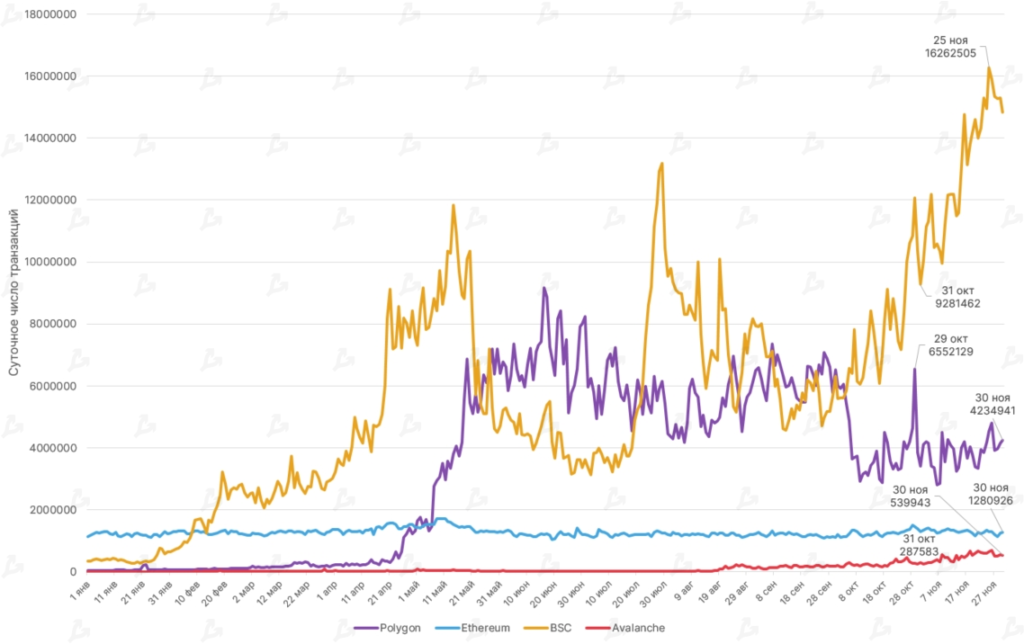

- Binance Smart Chain (BSC) remains the leader in daily transactions, handling about 13 million transactions per day in November (vs 7.76 million in October).

- Average transactions on Avalanche rose almost twofold in November — 482,000 vs 252,000 in October. The network also saw almost a twofold increase in unique addresses in its contract chain during the reporting period.

DEX and L2

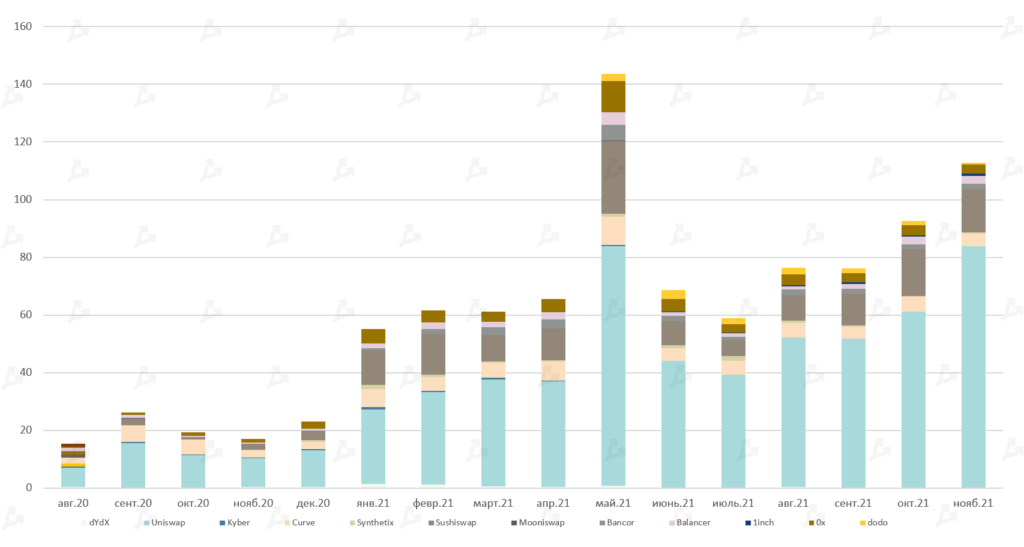

- Total trading volume on Ethereum-based exchanges in November reached $113B — second-largest in 2021.

- Uniswap remains leader among DEXs with $83.8B; SushiSwap and Curve follow with $15B and $4.2B, respectively.

- New Boba Network and ImmutableX projects helped sustain L2 scaling solutions’ growth; total TVL of L2s surpassed 1.5 million ETH, approaching $7B in November.

- TVL leaders Arbitrum and dYdX remained roughly flat at $2.7B and about $1B respectively, but Boba Network took second place. On November 12, BOBA tokens airdropped to OMG Network (OMG) holders, after which OMG fell roughly 30%.

- November saw the launch of the Ethereum scaling project ImmutableX (IMX), with its token price climbing to $9.5. The L2 project Loopring (LRC) also posted positive momentum.

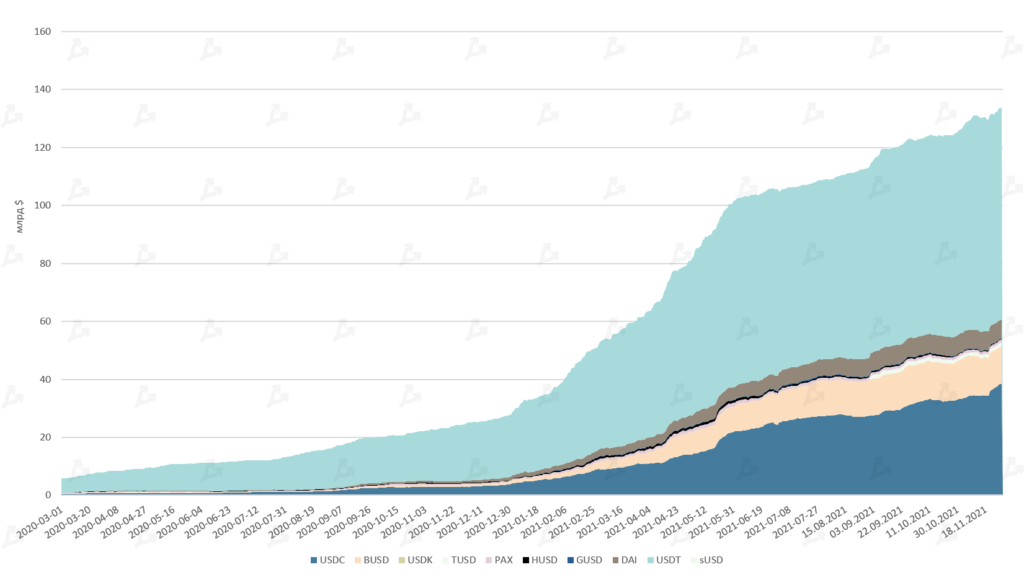

Stablecoins

- On the back of Bitcoin’s rally, the aggregate stablecoin market cap rose to $133B.

- USDT market cap exceeded $73B, and USDC stood at $38B.

- USDC’s issuance pace in November outpaced USDT’s — USDC up by $5B, USDT by $3B.

NFT and GameFi

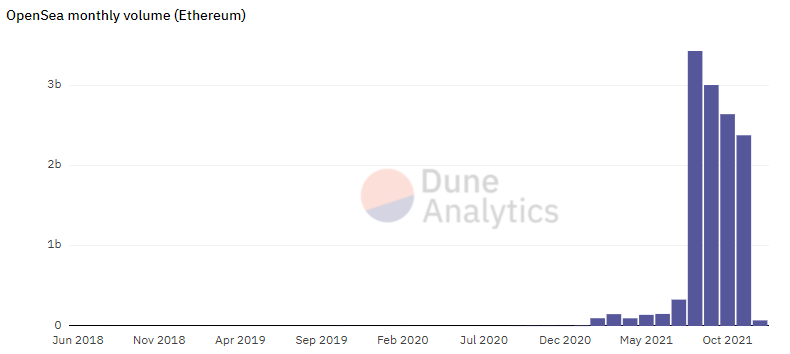

- NFT trading volume on the OpenSea marketplace continued to decline — November volume fell to $2.37B.

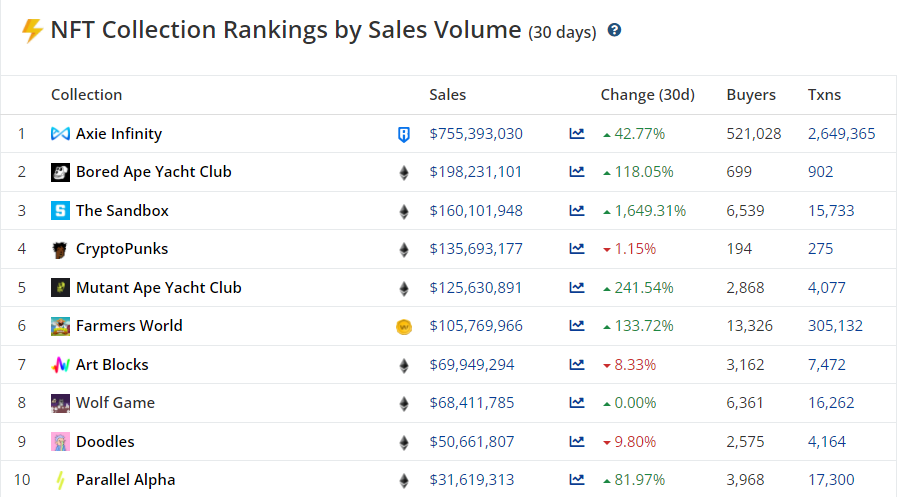

- However users remain interested in non-fungible tokens. Volumes across most leading projects rose by tens or hundreds of percent — Axie Infinity, Bored Ape Yacht Club and Mutant Ape Yacht Club.

- Prices of virtual items on alternative chains rose. One NFT player purchased a land plot for 550 ETH (~$2.4M at the time), while a CryptoPunks sale fetched 500 ETH (~$2.3M at the time).

- The Sandbox NFT platform’s trading volume surged by 1649% in November on the alpha-launch date, aided by a partnership with Adidas. The native token SAND hit multiple price highs, peaking at $8.50.

- Enjin launched a $100M fund to invest in metaverse projects within the Efinity ecosystem — ENJ rose 35% and EFI 84% in November.

- Grayscale analysts predicted that annual revenue from the Web 3.0 metaverse sector could reach $1 trillion.

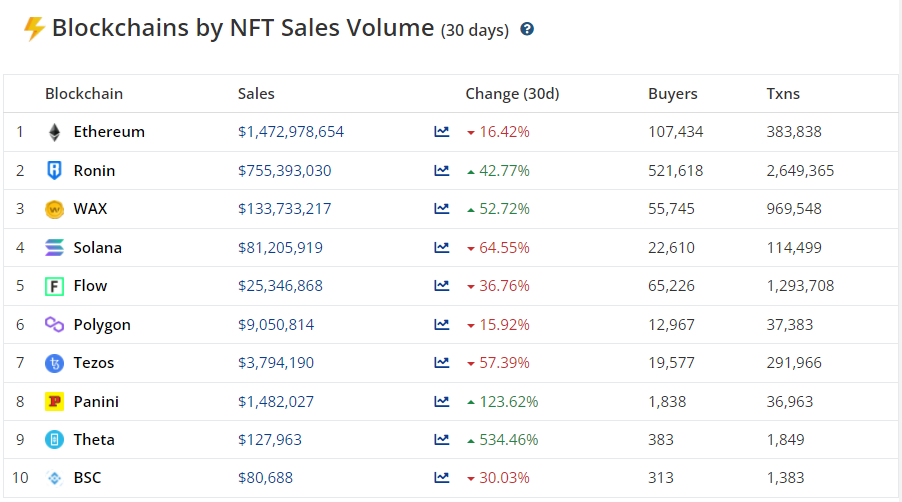

- Despite a drop in Ethereum NFT sales, the second-largest crypto network remained dominant in this segment, accounting for $1.47B in November.

- Ethereum-side chains like Ronin (used by Axie Infinity) and the Wax blockchain posted 42% and 52% growth respectively; November NFT sales on Wax reached a record ($133M).

- NFT projects on Solana and Flow faced dampened user interest.

Activity of Major Players

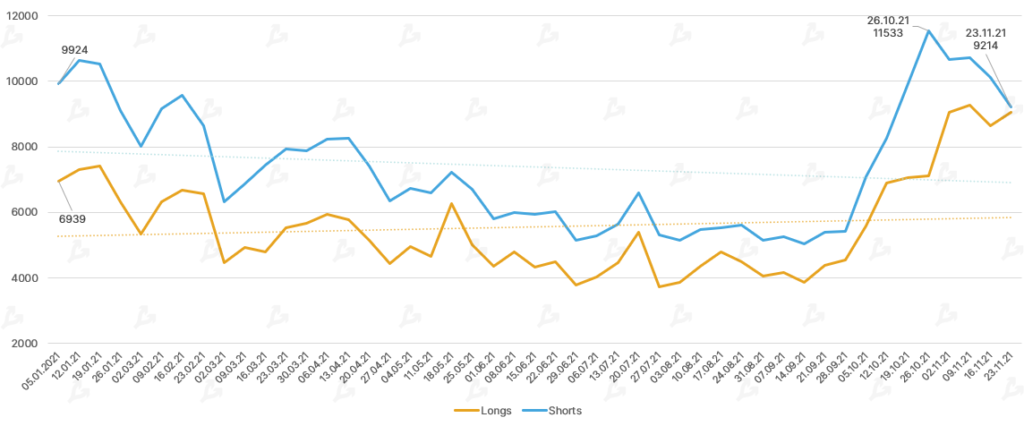

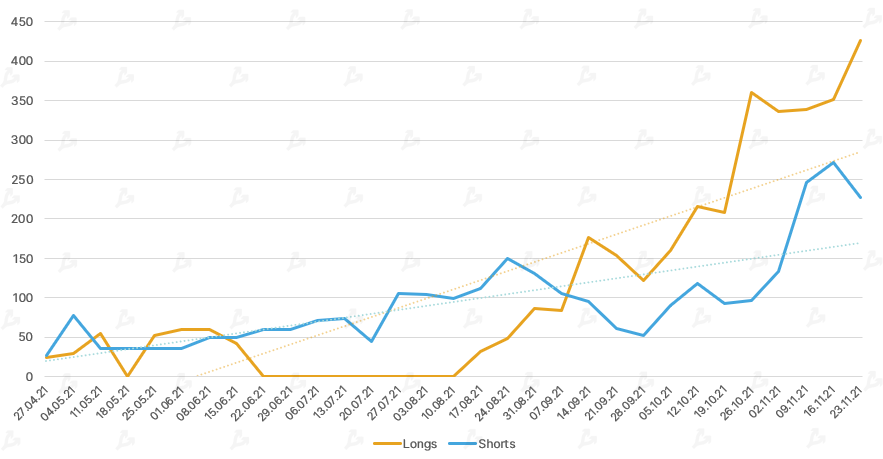

- In November, open interest in CME Bitcoin futures retraced from the early-month high. According to the latest CFTC report, the indicator was 14% below October’s peak.

- Hedge funds and other major Non-Commercial players reduced shorts, while longs were increased among Commercials.

- For the first time in a while, Non-Commercials’ short positions outpaced the longs. The likely reason is Bitcoin’s price correction that persisted for most of the month.

- Institutions (Commercial), conversely, continued to build longs amid a decline in shorts. This is presumably linked to demand for the first U.S. Bitcoin futures ETF (BITO) by ProShares, which accounts for over 95% of the total AUM among three SEC-approved ETFs.

- Analysts at Glassnode highlighted the growing dominance of CME in the Bitcoin futures market. CME’s share of OI rose from 10% at the start of September to 19.3% currently. In terms of trading volume, CME’s share rose from 1.4% to 6% over the same period.

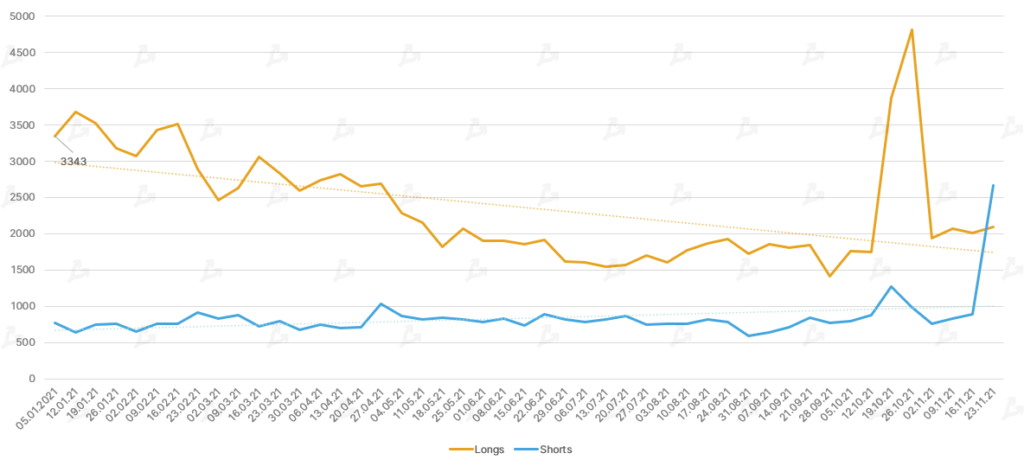

- Open interest in CME Ethereum futures continues to rise. Non-Commercials remain short, while Nonreportables stay long. Institutions (Commercial) have been building longs since September.

- Positive Ethereum futures dynamics may reflect expectations of an ETH-based ETF to be launched. Applications were filed with the SEC by firms including Kelly Strategic Management, WisdomTree and Kryptoin.

- MicroStrategy bought 7,002 BTC in November. As of now, its treasury holds 121,044 BTC worth about $6.9B.

- Marathon Digital substantially increased its Bitcoin reserves—from 6,695 BTC to 7,453 BTC. The company announced a bond offering for up to $500M to fund ASIC purchases; later Marathon raised its target to $650M.

- Hut 8, Riot Blockchain, Bitfarms, and Argo Blockchain also expanded their BTC reserves by 11.5%, 13%, 30% and 44% respectively.

- El Salvador’s Bitcoin fund bought an additional 100 BTC. The fund’s balance now stands at 1,220 BTC (~$70.2M at the time of writing).

Major Venture Rounds

$725 mln

Forte, a provider of blockchain solutions for game publishers, in Series B. Backers include Andreessen Horowitz, Tiger Global, Solana Ventures, Animoca Brands and others.

$555 mln

MoonPay, a crypto-payments startup, in Series A. Led by Tiger Global Management and Coatue; investors valued the project at $3.4B.

$536 mln

Bitkub, a Bitcoin exchange. Siam Commercial Bank (the oldest bank in Thailand) acquired a controlling stake (51%).

$400 mln

Gemini, a crypto exchange operator. In a round led by Morgan Creek Digital, the company was valued at $7.1B.

$350 mln

Celsius Network, a crypto lending platform. The investment continued the Series B round, valuing the company at $3.25B.

$300 mln

Niantic, the team behind Pokemon Go. The company was valued at $9B and will invest in building a metaverse.

$260 mln

CoinSwitch Kuber, an Indian Bitcoin exchange, in Series C; firm valued at $1.91B.

$175 mln

DeFi project 1inch Network in Series B with Amber Group, Alameda Research, VanEck and others.

$152 mln

Sky Mavis, the team behind Axie Infinity, in Series B. Valuation of the startup reached $3B.

$150 mln

Mythical Games, NFT game developer. In Series C led by Andreessen Horowitz, company valued at $1.25B.

$150 mln

Zepeto, metaverse platform from South Korea’s NAVER in Series B.

$93 mln

The Sandbox, gaming blockchain platform, in a round led by Vision Fund 2 of SoftBank.

K Regulatory Developments

- Representatives of several ministries backed the idea of equating mining to entrepreneurship. Head of the State Duma Committee on Financial Market Anatoly Aksakov stated that a working group on crypto-mining regulation would start soon.

- In LDPR, there was a strong wish from miners to pay taxes — the faction will draft a bill regulating digital asset mining.

- In the State Duma proposed Irkutsk region as a pilot for moving miners out of the “gray zone.” Its governor said he was ready to allocate industrial power.

- Deputy director of the Federal Financial Monitoring Service (Rosfinmonitoring) German Neghlyad stated about upcoming regulation of exchange offices for virtual currencies.

- The Prosecutor General’s Office proposed to deem cryptocurrencies and other virtual assets as property for criminal proceedings.

- President Kassym-Jomart Tokayev ordered to regulate mining without delay.

- Local parliament member proposed additional criteria for regulating mining amid country-wide power outages.

- Local exchanges and brokers became subjects of financial monitoring.

- Joe Biden signed a $1.2 trillion infrastructure bill with an expanded definition of “broker.” An advocacy group sent a new bill to Congress reflecting crypto-industry-favorable amendments.

- U.S. Treasury published a report on stablecoins’ risks, proposing to treat issuers as depository institutions with required insurance and related regulation.

- A cross-agency group including the Fed, FDIC and OCC, under the U.S. Treasury, will present guidance for regulator interaction with cryptocurrencies in 2022.

Other Regions

{kind=link}

{kind=link}

Notable November Events

On November 14, at block #709632, the long-awaited Taproot upgrade was activated. The upgrade aims to boost network scalability and user privacy through Schnorr signatures and MAST (Merkle-tree trees), increase Bitcoin’s block size, and reduce transaction fees.

Read more about Taproot in ForkLog’s educational cards.

On November 15, liquidity-aggregator ParaSwap released the PSP governance token and airdropped 150 million tokens to 20,000 wallets. Many users did not receive tokens despite using the platform. The team abandoned “bounty-hunters” intent on exploiting airdrops, setting a precedent.

In the first auction, the Acala project won, locking over 32.5 million DOT (~$1.33B) of the total 87.55 million DOT.

The second slot went to Moonbeam. In favor of Moonbeam, 35.7 million DOT were locked.

Both auctions had little impact on Polkadot’s price (DOT).

Apple CEO Tim Cook stated that he personally owns cryptocurrencies, using digital assets to diversify his investment portfolio.