Against a backdrop of a volatile macroeconomic environment the Terra collapse triggered a deep crisis in the cryptocurrency industry.

Several major players, including Celsius Network and Three Arrows Capital (3AC), filed for bankruptcy; miners faced difficulties servicing debts and accessing capital, and the market saw a wave of liquidations.

Some draw parallels between the current situation and the 1907 banking panic. At the time, a string of poor decisions by lending institutions caused a frenzied withdrawal of deposits by savers and threatened to crash the US economy.

In the 20th century, the situation was “saved” by on the rise — wealthy financiers who put up their own money to support the American credit system. In 2022, this role was undertaken by the industry’s crypto titans.

ForkLog examined what goals crypto billionaires pursue by investing in troubled companies.

- Banking Panic of 1907 threatened to collapse the US economy, but the crisis was averted thanks to the efforts of John Morgan and other bankers. At the same time these figures became the main beneficiaries, wiping out rivals and expanding their own capital.

- The Terra collapse and the ensuing wave of bankruptcies among centralized market participants created a “perfect storm” for industry consolidation. Successful firms gained the chance to grow by absorbing weaker players.

- The “saviors” act in their own interests, providing funding to companies advantageous to themselves.

- As of writing there is no verified information on the concrete actions of players previously declaring readiness to invest in troubled industry participants. An exception is Sam Bankman-Fried and affiliated entities.

A Veil Before the Eyes

In the first decade of the 20th century, the US economy was on the rise — bountiful harvests, low unemployment, high corporate profits.

1906 proved so successful that American lending institutions borrowed about $500 million on European markets. The money was lent to corporations pursuing opportunities to buy out rivals.

Meanwhile a number of events in the US dented stock-market stability:

- In 1833 President Andrew Jackson refused to renew the charter of the Second Bank of the United States (which expired in 1836), the de facto lender of last resort;

- In July 1906 the Hepburn Act was passed, allowing the ICC to set maximum railroad tariffs. The act reduced the market value of sector shares;

- In November that year, the case against Standard Oil by John D. Rockefeller began. The company was accused of violating antitrust law.

The combination of these factors and corporate approaches to business put the financial system at risk — as the market consolidated, debt levels rose.

Banks underwriting bonds for companies also contributed, providing the liquidity that underpinned current lending.

Banking Panic

A banking panic is a mass withdrawal of deposits from lending institutions amid doubts about their financial stability.

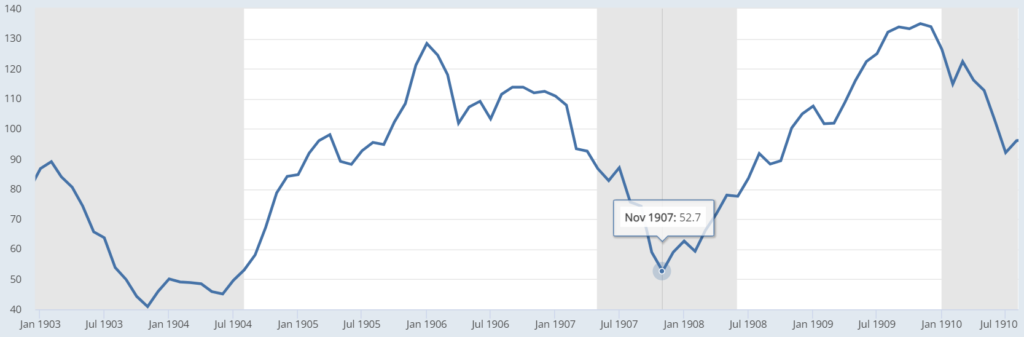

The Panic of 1907 began in October with copper-market manipulation. Otto Heinze, brother of United Copper Company owner August Heinze, together with banker Charles Morse, sought to execute a scheme to aggressively buy the company’s shares.

However, Otto’s plan collapsed, and his brokerage Gross & Kleeberg went bankrupt. Almost simultaneously, the State Savings Bank of Butte, Montana — owned by August Heinze — declared insolvency.

Depositors began withdrawing funds from banks tied to Heinze and Morse.

Contagion spread rapidly to other sectors. By October’s end, the New York Stock Exchange index had fallen 58% from its 1906 peak.

In November markets began to recover, and the aforesaid John Morgan played a key role, not only investing part of his own fortune to quell the crisis but also persuading other bankers to provide the liquidity needed.

The Mightiest of Them All

Within the context of “saving” distressed market participants, the founder of JPMorgan & Co. is the most conspicuous figure. His role in resolving the 1907 crisis is described by some as “almost godlike”.

At the onset of the panic, Morgan’s house wielded tremendous influence and a large liquidity cushion. Founded in 1901, United States Steel Corporation became the world’s first publicly traded company with a market capitalization exceeding $1 billion.

By 1907 the corporation controlled not only the steel business but a sprawling railway network. It owned lands whose total area was greater than the state of Massachusetts, and over 180,000 workers were employed at its plants.

“In 1906, U. S. Steel Corporation paid its employees $128 million — more than the United States spends on its army or navy. Fifty of its mines produced a sixth of all the world’s iron ore. At its plants, more steel was produced than in Britain and Germany combined — a quarter of world production,” wrote journalist Herbert Casson.

John Morgan, then in Richmond, understood that the banking crisis was spreading and would soon engulf healthy institutions.

However, apparently he was in good spirits. As Harper’s Magazine editor Frederick Allen wrote, on his way to New York the millionaire “was in excellent spirits” and “whistling some tune.”

The Good Reason and the Real Reason

Back in the US financial capital, Morgan joined George Baker (president of the First National Bank of New York) and James Stillman (chairman of the National City Bank of New York). They formed a committee to decide which institutions could still be saved and which should be sacrificed.

For these aims, the bankers allocated about $30 million, including $10 million borrowed from John D. Rockefeller. The capital was used to lend to other lending institutions.

At the same time, Morgan launched a series of aggressive M&A deals. Primarily, JPMorgan absorbed Mercantile Trust and six other trust companies and banks.

The financier seized the opportunity to buy shares of rivals, across the maritime, railway and steel sectors. The campaign’s crowning achievement was the purchase of Tennessee Coal and Iron — a direct competitor to U. S. Steel Corporation.

The deal came perilously close to violating antitrust law (the Sherman Act). To close the process, Morgan turned to President Theodore Roosevelt, who agreed to look the other way.

Ultimately, Morgan’s actions and those of his allies helped quell the panic, and by year’s end the economy had stabilised. Yet the main “savior” ended up being the crisis’ chief beneficiary.

This did not escape the attention of politicians. In January 1913, congressman Arsène Pujo conducted an investigation and issued a detailed report on JPMorgan’s activities.

Morgan and a number of other influential bankers gained consolidated control over numerous industries and monopolised them. No fewer than 18 large financial corporations were under the control of a consortium led by JPMorgan.

Morgan, Baker and Stillman personally controlled more than $2.1bn through seven banks and trust companies. In addition, JPMorgan employees sat on the boards of 112 corporations with a combined market capitalisation of $22.5bn — at the time, the total value of all New York Stock Exchange shares was about $26.5bn.

Despite the extensive evidentiary base and a wide-ranging investigation, no one named was held to account. Not surprisingly, some formed a view that the banking panic was artificial. After all, Morgan himself once said:

“A man always has two reasons for doing anything. A good reason and a real reason.”

The Domino Effect

In 1907 the crisis lasted just under a month and plunged the US economy into recession. It is unclear how things would have ended if Morgan had not stepped in.

In 2022, events in the digital-asset market unfolded more gradually and largely depended on macroeconomic factors, not solely on the actions of industry players.

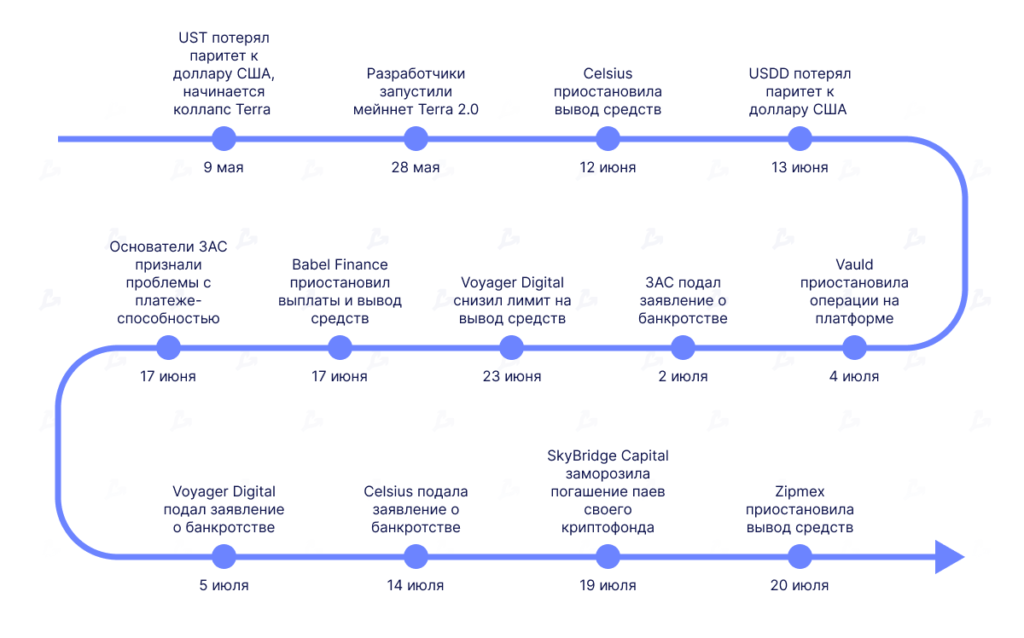

The Terra collapse occurred as the local bullish trend broke. The loss of the USD peg for UST triggered a cascade of liquidations in decentralized services. The final collapse of the ecosystem of one of the largest cryptocurrencies became the catalyst for the downturn.

When the dust settled, it was clear that the incident had infected the crypto industry. A number of major market participants used the Anchor protocol to stake UST and held positions in LUNA.

The Terra problems, the market downturn and the subsequent depeg of stETH triggered a wave of bankruptcies among centralized participants, who parked client funds in decentralized services for extra yield.

The situation is further compounded by the prevalence of leverage in the industry, which participants had previously overlooked. According to Binance CEO Changpeng Zhao, because of the leverage, the sector is facing a protracted crisis. He explained that debt positions of large funds and DeFi protocols are hard to unwind quickly. Yet such events trigger a cascading effect that spreads slowly.

The industry appeared to be tearing at the seams — the bankruptcies of major players like 3AC and Celsius undermined confidence and hit their creditors, while accompanying fire sales hurt retail investors and miners.

In an interview with Protocol, Logan Allin, founder and managing partner of Fin Venture Capital, described the situation as a “perfect storm that will lead to the consolidation of the entire industry.”

Sam Bankman-Fried is doing a personal (and personally lucrative) bailout of the crypto financial system like JP Morgan personally bailed out the US banking system in the panic of 1907. … by 1913 the federal reserve was created as a reaction to this crisis. https://t.co/fmxLySvQ2Z

— Will Diamond (@wdiamond_econ) June 30, 2022

“Bankman-Fried is personally (and for personal gain) saving the crypto-financial system the way John Morgan personally saved the banking system during the 1907 panic,” said Will Diamond, finance professor at the Wharton School.

Be John Morgan

For players with deep pockets, the crisis is, of course, a golden opportunity to expand. After all, the sector’s valuations have fallen sharply.

OTC valuations I received vs. last valuation (unsolicited):

+ FTX, Animoca -> 25% off

+ Blockchain, ConsenSys, Kraken, OpenSea -> 50% off

+ Celsius -> 90% off pic.twitter.com/ToPCbc1KLr— Ryan Selkis 🥷 (@twobitidiot) July 1, 2022

That’s why not only Bankman-Fried proclaims himself a “savior” — other industry giants have announced plans too.

In June, Changpeng Zhao noted that crypto winter is an ideal time for acquisitions. In the same month he declared that Binance is “obliged” to protect users and help the rest of the industry survive. He stressed that some companies and products are poorly designed, managed and exploited. He argued that newer, better projects will replace them, so there is no need to rescue them.

In particular, Zhao criticised Alameda’s deal with Voyager Digital, saying he would never have agreed to such a deal — and that a loan from Bankman-Fried would not save the broker — and he was right: the firm eventually filed for bankruptcy.

So, 3AC owes Voyager a few 100m, went bust. FTX/Alameda gives 3AC $100m, but didn’t save it.

Alameda invests in Voyager, then takes a $377 million loan from Voyager… ok…

V went bust. FTX didn’t “bail them out” or return the money?

hard to follow?https://t.co/yx6RJjVZrB

— CZ 🔶 Binance (@cz_binance) July 7, 2022

“Bankman-Fried is personally (and for personal gain) saving the crypto-financial system the way John Morgan personally saved the banking system during the 1907 panic,” said Will Diamond, finance professor at the Wharton School.

Becoming John Morgan

For players with large cash reserves, the crisis is an excellent opportunity to expand. Not only Bankman-Fried claims to be a “savior” — other industry giants have announced relevant plans as well.

In June Changpeng Zhao noted that crypto winter is a great time for acquisitions. In the same month he stated that Binance is “obliged” to protect users and help the rest of the industry survive. He stressed that some companies and products are poorly designed, managed and exploited. He argued that newer, better projects will replace these, so there is no need to rescue them.

Specifically, Zhao criticized Alameda’s deal with Voyager Digital, saying he would never have agreed to such a deal — and that a loan from Bankman-Fried won’t save the broker — and he was right: the company eventually filed for bankruptcy.

In July Zhao said that Binance intends to help industry participants who face a “slight liquidity shortage” and is in talks with more than 50 companies.

The billionaire stressed that his platform does not compete with FTX, as the latter is more focused on the U.S. market. Yet since the crisis began the exchange has made no public statements about acquiring or funding any company.

But then Justin Sun claimed he would earmark $5 billion for troubled market participants and said he was approached by several industry representatives — for talks about potential deals he brought in an unnamed investment bank.

However, no public steps followed. At the end of July he announced that Tron DAO would acquire Tencent’s NFT marketplace Huan He, which somewhat aligns with the industry-rescue strategy.

Nevertheless, Sun has his own problems — in mid-July Tron managed to restore the peg of its algorithmic stablecoin USDD to the US dollar. It seems this issue concerns him more than others.

#USDD 👀 pic.twitter.com/YaVs68bEK1

— H.E. Justin Sun🌞🇬🇩 (@justinsuntron) July 27, 2022

Consequences of Consolidation

Speaking with ForkLog, KuCoin chief Johnny Lu observed that the crisis is an excellent moment to explore ways to jointly improve the industry.

“The crypto industry is defined by co-existence and co-creation. Collaboration and mutual support are what ensure the sector and its participants survive. … When the industry faces a crisis, we look forward to responsible builders stepping in to defend it, and we are ready to play that role ourselves,” he said.

But there is another side. Companies and owners pursue very specific goals — namely, to maximise efficiency and profit. So their intentions may not align with the ideals of the blockchain culture.

“The real reason for their investments is something you can understand only by knowing what’s in their heads. But my hunch as a businessman is that they are buying traffic and users,” ForkLog founder Mikhail Chobanian explained.

The US banking panic and the Pujo report led to the creation of the Federal Reserve System. The appearance of a similar structure in the digital-asset market seems unlikely.

What can be expected is increased regulatory scrutiny. However, according to Lu, crypto empires should not fear antitrust lawsuits.

“Whether a company becomes the target of antitrust investigations depends on whether it shows signs of monopolistic behaviour. Neither huge trading volumes nor vast resources can create a monopoly. In a decentralised industry there cannot be monopolists due to its diversity and dynamism. No one will gain from concentrating influence in a small circle,” he said.

Concerns about ongoing reshuffles remain. Lu said consolidation carries systemic risks of centralisation. Yet he noted these are natural processes that would occur regardless of market conditions.

“Consolidation equals centralisation. The same risks stay: switch off one — switch off a third of the industry, a quarter, perhaps one fifth. On the other hand, these are natural processes. Market monopolisation is probably in our DNA,” he said.

Lu added that other companies will later try to prise a share of the market from the moguls. In his view, a cycle of companies and influence will recur worldwide.

History shows that crises have winners and losers. But it is too early to judge how the consolidation wave will end, as there is no reliable information about the actions of major players yet.

Read ForkLog’s bitcoin news on our Telegram — cryptocurrency news, prices and analysis.