The past few years have been hard on most decentralised-finance (DeFi) protocols. Many well-known players have significantly cut staff, and some shut down altogether.

Early 2024 was uneventful for DeFi. Despite a nascent market recovery and spot ETFs already coming into view, the segment was in no hurry to surge. In January its TVL hovered around $50bn, on par with March 2021 levels.

Few were optimistic about a quick rebound in decentralised finance given the sector’s lacklustre metrics and a sluggish crypto market overall. Yet in early March, Bernstein analysts expressed hope for an accelerated DeFi recovery on the back of bitcoin’s rise and hefty ETF inflows.

- The last bear market stress-tested DeFi, spurred consolidation and strengthened core technologies.

- Layer-2 solutions and Solana’s rise became key drivers of recovery and ecosystem scaling.

- DeFi’s aggregate TVL doubled in 2024, with projects on Ethereum, Solana and new L2s setting the tone for further growth.

Bear market and consolidation

From mid-autumn 2021 to roughly February–March 2024, the market was bearish. Recession gave way to grinding stagnation, most crypto assets fell, and regulatory uncertainty bred investor scepticism. This period, however, stress-tested decentralised finance and strengthened its foundations.

Ethereum, the bedrock of DeFi, faced a series of challenges. Despite being the most decentralised, it continued to grapple with scaling.

The rapid growth of layer-2 (L2) solutions eased the load on the network behind the second-largest cryptocurrency. It also had drawbacks: liquidity fragmentation and barriers to composability across protocols.

Amid these issues, Solana surged in popularity for fast, low-cost transactions and, alas, periodic outages. The chart below shows the ecosystem’s sharp TVL rebound in 2024 after the FTX-induced collapse.

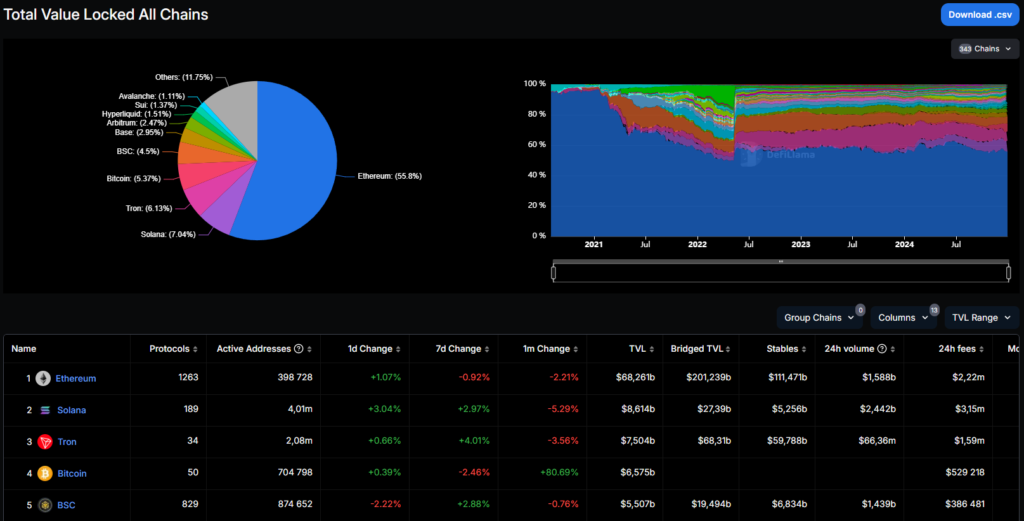

As of 29 December, Solana ranks second on DeFi Llama, behind only Ethereum, though the gap remains wide. Its TVL has grown more than sixfold since the start of the year.

A new landscape and a DeFi renaissance

Despite depressed metrics through the bear market, development continued. DeFi veterans such as Maker, Aave and Uniswap held firm, offering investment opportunities and fresh technology. New projects and even entire ecosystems appeared, intensifying competition.

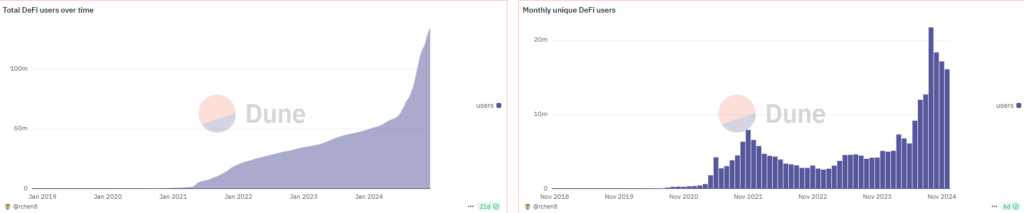

Against this progress and a gradual market recovery, DeFi’s user base has shown accelerating growth since early 2024.

Roughly half a year after bitcoin’s fourth halving, the crypto market revived, lifting the aggregate TVL in decentralised finance.

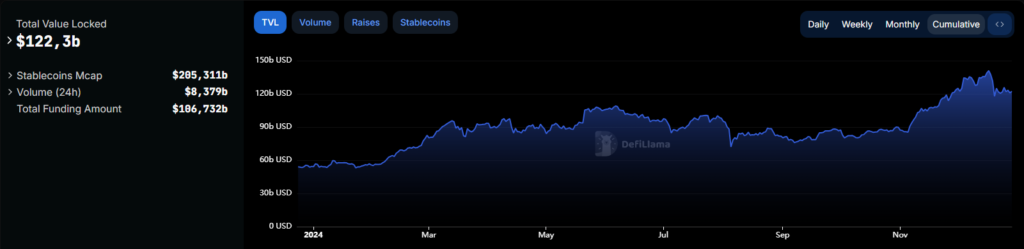

In early November the figure topped $100bn, more than double its level at the start of the year.

As of 29 December, DeFi’s total TVL is about $122bn—still some way off the November 2021 peak above $170bn.

Ethereum layer 1

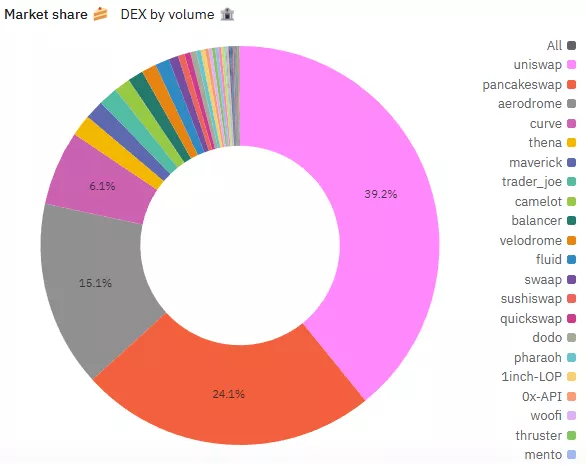

Among Ethereum-based DEXs, Uniswap remains the clear leader. The platform’s turnover accounts for nearly half of aggregate volumes across other major non-custodial exchanges.

Competition has intensified, and Uniswap’s market share has been slipping.

The developers have hardly been idle: they have long been working on the fourth version of the largest DEX. Uniswap v4 will introduce an innovative “hooks” system—plug-ins that add new features to liquidity pools, such as dynamic fee adjustment or various order types.

Another key novelty is “flash accounting”, which will cut costs for liquidity providers. Activated via EIP-1153, it optimises on-chain storage and lowers fees.

At the end of November, Uniswap Labs said it was ready to pay up to $15.5m for critical vulnerabilities in the v4 smart contracts—the largest bug-bounty reward to date.

In October the team opened direct swaps of native tokens and stablecoins across nine networks via its interface and wallet. The solution is built on the permissionless Across Protocol, which uses a decentralised network of liquidity pools and relayers.

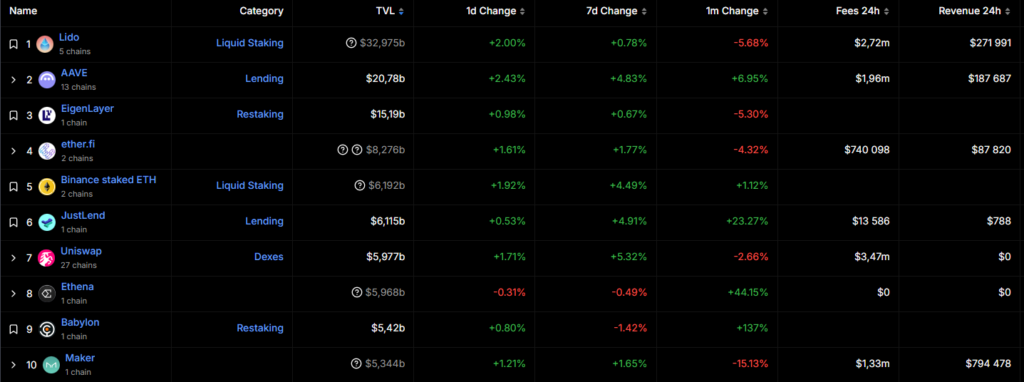

Another key DeFi project—Aave—has also held its ground. TVL on the leading lending platform has topped $20bn; on DeFi Llama’s overall ranking it trails only Lido.

The lending service operates across 13 networks. In July 2023 the developers launched the decentralised stablecoin GHO; a year later it debuted on Arbitrum.

Other notable developments include:

- MakerDAO’s rebrand—the service became Sky;

- the launch of a fully overhauled third version of the Synthetix synthetic-assets platform;

- Lido consolidating its lead as the largest liquid-staking protocol—its TVL is nearing $40bn despite rivals such as Rocket Pool and mETH Protocol;

- the rise of restaking, with a clear leader—EigenLayer—with TVL above $16bn;

- the emergence of a derivative sector—liquid restaking—where key players include Ether.fi, Renzo, EigenPie and others, with TVL peaking at $18bn;

- the advent of Ethena’s USDe synthetic dollar, whose market cap is nearing $6bn;

- the growth of decentralised lending protocols such as Morpho, offering high capital efficiency, flexibility and relatively low transaction costs;

- a TVL surge at Pendle, a platform for trading future yields on crypto assets.

Ethereum L2s

In March, the Dencun upgrade went live, which dramatically cut fees for layer-2s, especially rollups.

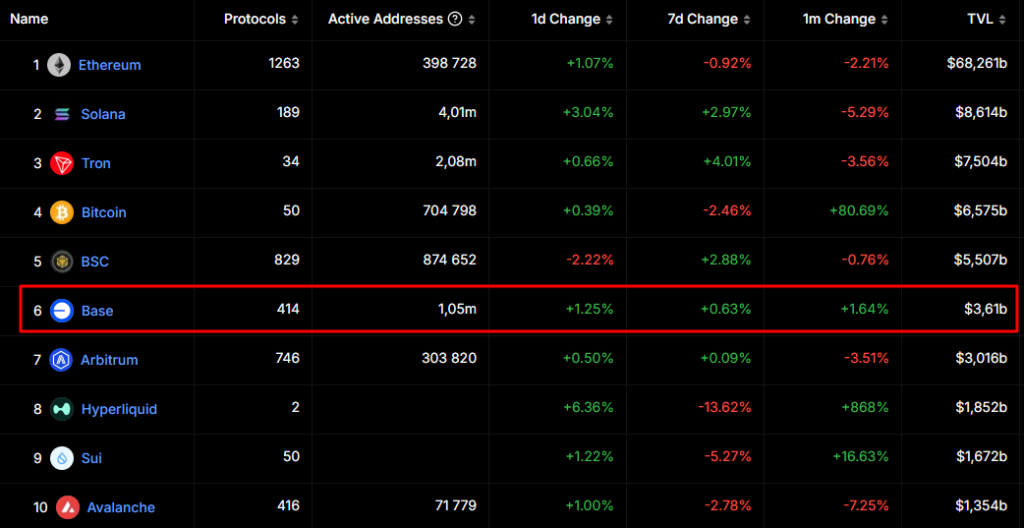

Coinbase-backed Base has overtaken Arbitrum by TVL—as of 29 December it tops $3.6bn.

The metric rose alongside surging on-chain activity and heavy DEX volumes.

The leading Base DEX remains Aerodrome, whose TVL and daily turnover exceed $1bn.

Other well-known L2s—OP Mainnet, Linea, ZKSync, Starknet and Scroll—continue to push forward, vying to cement their positions and keep users loyal.

Solana

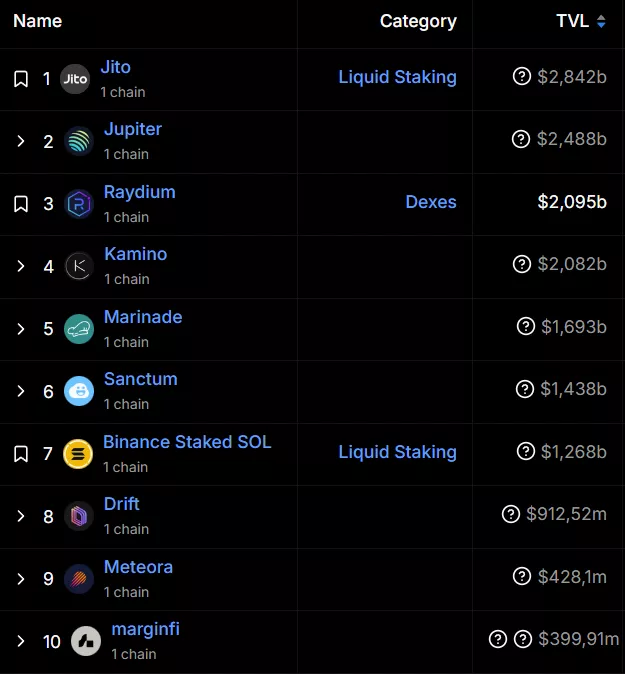

As noted, Solana’s ecosystem has grown strongly. As of 29 December its TVL stands at about $8.6bn.

The largest protocols include:

- Jito—liquid staking;

- Jupiter—non-custodial trading (spot and perpetuals);

- Raydium—an AMM DEX.

“DEXs and aggregators such as Orca, Raydium, Jupiter and Drift managed to emerge from the bear market’s shadow. Fueled by the hype around memecoins, they started ramping up trading volumes and ultimately surpassed decentralised exchanges on Ethereum,” noted the developer and founder of Finematics under the nickname Jakub.

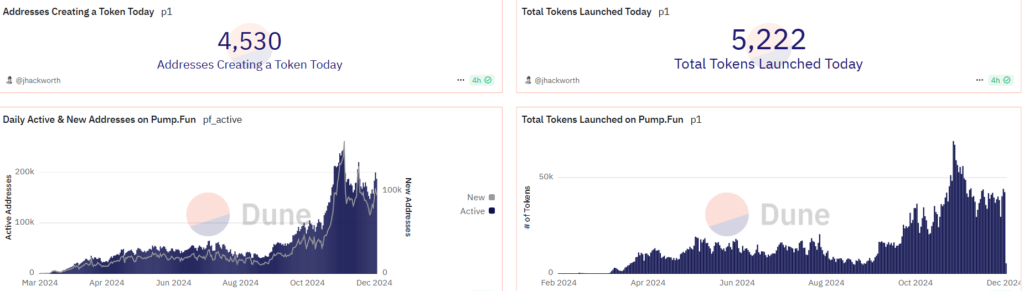

Pump.fun has established itself as a simple, convenient platform for launching new memecoins. Despite problematic content and contentious moderation, it continues to contribute significantly to Solana’s on-chain activity.

Below are some key Pump.fun metrics as of 27 December:

- daily number of token-issuing addresses—4,530;

- number of tokens issued per day—5,222;

- daily active and new addresses—>200,000;

- number of tokens issued on the platform per day—>40,000.

According to a Dune dashboard by Hashed, more than 5m memecoins have been launched on Pump.fun to date.

Among Solana lending projects, Kamino stands out. Its TVL recently crossed $2bn.

DeFi’s prospects

Major Ethereum upgrades are expected, and there is already a large cohort of L2 networks whose competition will likely intensify.

Vitalik Buterin is convinced that as layer-2 solutions evolve, overall network throughput can reach an impressive 100,000 transactions per second (TPS).

In his words, “no other network has come close to Ethereum’s current level of decentralisation.”

Among other priorities, Buterin highlighted:

- greater decentralisation, censorship resistance and quantum resilience;

- better scaling;

- surpassing 100,000 TPS through L2 solutions;

- the development of applications such as social networks and payments;

- lowering the staking threshold from the current 32 ETH to make running a node easier and more accessible.

The community may adopt Beam Chain, a proposal by developer Justin Drake to overhaul Ethereum’s consensus layer from scratch.

The initiative bundles the latest ideas from the research roadmap.

According to Drake, Beam Chain targets faster slot times, smaller validator assignments, chain snarkification and, ultimately, post-quantum security.

He framed the potential transition as part of Ethereum’s evolution—from PoW to PoS and towards a potential ZK-based Ethereum consensus.

Sketching a rough timeline, Drake said specification work could start next year, with implementation in 2026.

The upgrade could materially increase Ethereum L1 TPS, “completely eliminating the need for rollups”.

Drake is confident L1 innovation will proceed step by step, with improvements rolling out and becoming available every year for many years.

Projects offering new technical approaches are emerging—from novel execution environments and languages to enhanced virtual machines.

For instance, the decentralised perpetuals platform Hyperliquid stands out for speed and a high degree of decentralisation. Its L1 blockchain with a native DEX module uses a modified Proof-of-Stake consensus called HyperBFT. According to the team, throughput reaches 200,000 TPS, making it one of the fastest platforms on the market.

At the end of November the project conducted one of the largest airdrops in crypto history. Shortly after, the decentralised trading platform with three protocols in its ecosystem entered DeFi Llama’s top 10 by TVL. Within five days of the TGE, the HYPE token tripled in price.

In December the Avalanche team released the Avalanche9000 upgrade, cutting Subnet deployment costs by 99.9% and C-Chain transaction fees by 25x for Ethereum-compatible smart contracts.

Innovation is arriving on “layer two” as well. Consider MegaETH, an L2 focused on high-speed execution. The project has backing from Vitalik Buterin, Joseph Lubin, Dragonfly Capital and others.

The team positions MegaETH as the first Ethereum-compatible “real-time blockchain”, aiming for 100,000 TPS.

In October, Uniswap Labs unveiled its own Ethereum L2, Unichain, geared to DeFi. It is built on Optimism’s OP Stack within the Superchain ecosystem.

Unichain will enable cross-chain interoperability and a decentralised validator network. At launch, block time will be one second, later dropping to 250 milliseconds. The developers foresee transaction costs falling by 95% versus Ethereum, and eventually even further.

The network uses a block builder created with Flashbots based on a trusted execution environment (TEE). This speeds operations, orders transactions and reduces the chance of failures.

Unichain is designed as a modular blockchain, allowing functionality to expand via new components while improving decentralisation and user experience.

Eclipse is an Ethereum L2 that uses:

- SVM as the execution environment;

- Celestia for data availability;

- RISC Zero for zero-knowledge proof generation.

In March the team closed a $50m Series A round.

Stylus is an upgrade to the leading L2, Arbitrum, enabling developers to write smart contracts in Rust, C or C++ without sacrificing EVM compatibility.

Another crucial driver of DeFi adoption is better user experience. A key path is broad adoption of account abstraction (AA). This can expand wallet capabilities and improve security.

Other benefits include:

- account-recovery options in case of key loss;

- batched transactions (eg, approve and execute a swap in one click);

- gas payments in stablecoins;

- scheduled and bundled transactions;

- alternative signing schemes;

- automation: portfolio rebalancing, dollar-cost averaging strategies.

For the Solana ecosystem, a key milestone will be the forthcoming launch of Firedancer, a new validator client from Jump Crypto. It aims to dramatically boost throughput and reliability, which could be supportive for SOL.

An early version, Frankendancer, went live in September.

Innovative projects such as NeonEVM are also progressing. This is the first “parallelised” EVM on Solana, combining strong compatibility with high throughput.

According to the project’s website, a token transfer or swap costs just $0.003. The chain can process over 2,000 transactions per second.

Developers of “parallelised” L1 rivals to Solana are also busy—Aptos, Sui and Sei are all pushing ahead. New entrants are appearing too:

- Monad—a layer-1 smart-contract platform with innovative scaling approaches;

- Berachain—a modular, EVM-compatible L1 using Proof-of-Liquidity consensus.

Interesting shifts are under way in the bitcoin ecosystem, reinvigorated by the Taproot upgrade. Alongside Lightning Network, other L2 scaling solutions are developing, as are “inscriptions” markets and BRC-20s.

The bitcoin staking protocol Babylon has gained traction. Its TVL has exceeded $5bn.

Co-founder Fisher Yu said DeFi on bitcoin barely existed until recently—staking or wrapping coins via dapps necessarily involved trust. In his view, “true DeFi” means trusting only the blockchain or the smart contract.

Tokenisation is another promising area. Despite regulatory uncertainty, the RWA segment continues to grow rapidly; its capitalisation has surpassed $20bn.

“It is hard to predict timing, but in the future we will likely see the overwhelming majority of the world’s assets tokenised and tradable in decentralised finance. This includes stocks, bonds, commodities, real estate and other financial instruments,” Jakub suggested.

He added that the pace of DeFi innovation is unlikely to slow. The sector will keep developing: infrastructure will become more robust, transactions faster, user experience better and cross-chain interoperability more efficient. DeFi will also integrate more deeply with artificial intelligence, gaming platforms and other promising fields.

Conclusions

The last bear market was not merely a downturn but a pivotal phase in the evolution of decentralised finance, laying the groundwork for its future.

DeFi is displaying resilience, innovation and growth. Despite crises, hacks and regulatory uncertainty, the segment has not only recovered but opened new avenues for financial technology.

Protocols such as Uniswap, Aave and Sky have not just survived; they have shipped advanced features, underscoring the ecosystem’s strength and potential.

Layer-2 projects including Arbitrum, Base and OP Mainnet are tackling scaling and attracting new users.

Solana is consolidating its position, while new layer-1s are jostling for attention.

DeFi is reshaping finance, making it more accessible, flexible and interconnected. Relentless progress promises more opportunities—and more innovation—to come.