The halving dented miners’ revenues, yet hashrate hit record highs, diversification into AI computing became fashionable, and America consolidated its lead in the industry.

A look back at what else defined bitcoin mining in 2024.

- The industry weathered the fourth halving.

- Amid falling revenues, a boom in AI computing offered a ‘lifeline’ to many participants.

- Seismic shifts began among leading manufacturers of bitcoin miners.

- Africa, led by Ethiopia, is emerging as a new global mining hub.

The halving and its consequences

On April 20 at block height #840,000 the fourth halving of the block reward took place, cutting it from 6.25 BTC to 3.125 BTC.

Through 2023 and into 2024 miners prepared for the inevitable revenue drop by reducing debt, upgrading to more efficient hardware and trimming costs.

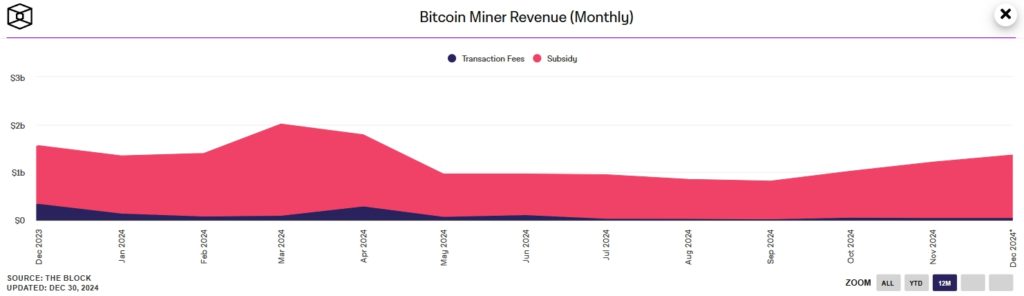

April’s takings were buoyed by a sharp surge in fees after the halving-day launch of the Runes protocol. On April 20 alone miners earned $17.66 million in network fees (7 DMA) — nearly 25% of total revenue of $72.35 million.

For the month, revenue reached $1.79 billion, of which block subsidies contributed $1.5 billion. Fees thus made up roughly 16%.

Once the frenzy around new assets faded, the fee share of bitcoin miners’ revenue had by July reverted to roughly 2.5–3.5%. Cash flow halved compared with March.

In April, CoinShares forecast that industry players would offset the post-halving shortfall by expanding into artificial-intelligence computing and other income streams, while hoping for bitcoin price appreciation.

One of the most visible AI-computing deals was a 12‑year contract Core Scientific signed with CoreWeave to provide 200 MW of infrastructure for hosting Nvidia GPUs.

This morning, $CORZ announced exercise of final contract option by @CoreWeave for delivery of ~120 MW of additional digital infrastructure to host high-performance computing operations.

-Expands total contracted #HPC infrastructure by CoreWeave to ~500 MW of critical IT load at… pic.twitter.com/zUmmfGFhnd

— Core Scientific (@Core_Scientific) October 22, 2024

In September, CEO Adam Sullivan said AI’s potential could deliver ‘exponential growth’, though not all of the firm’s 1.2 MW infrastructure can be repurposed due to technical constraints.

Core’s chief development officer Russell Cann noted the flexibility of bitcoin mining in adjusting power draw — an option AI computing lacks. Some miners participate in demand‑response programmes. Riot Platforms, for instance, earned $12.4 million from curtailments in the third quarter, on top of $19 million in the first half.

Moves into AI were also made by TeraWulf, Hut 8, IREN and HIVE Blockchain. Crusoe Energy Systems announced a 1.2 GW data centre to serve AI companies.

European miner Northern Data chose to divest its Peak Mining unit, whose hashrate should reach 7.9 EH/s by end‑2024, to focus on cloud computing.

In the second half, JPMorgan observed a trend of some miners emulating MicroStrategy: not only holding mined BTC but also buying more using low‑coupon convertible debt. Examples include MARA Holdings, Hut 8 and Riot Platforms.

Analysts at CoinShares estimate that, assuming current market conditions persist, direct investment in bitcoin over the next four years will be roughly four times as profitable as investing in mining.

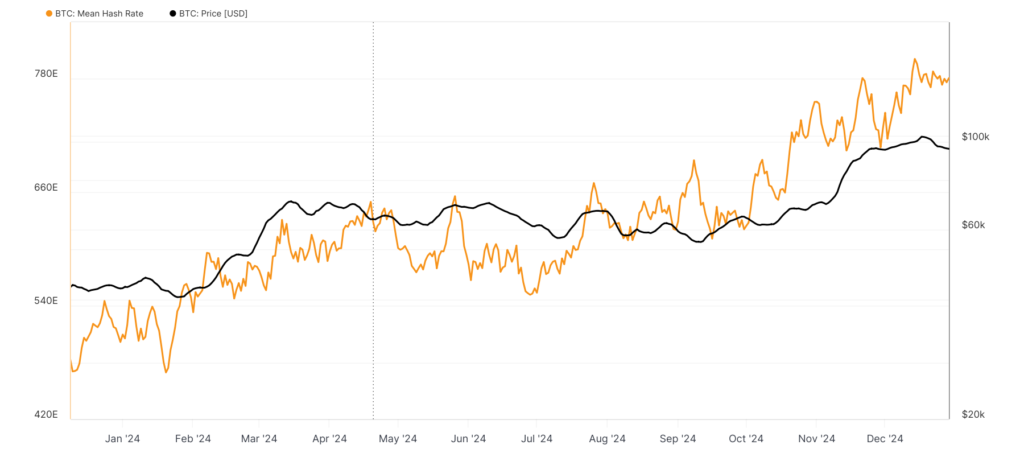

In the autumn, a bitcoin rally supported mining economics, lifting the price to a record above $100,000.

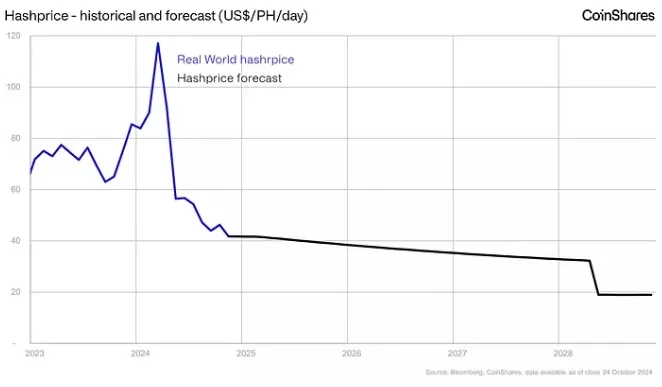

Hashprice (miners’ revenue per unit of network hashrate) rose to about $60 per PH/s per day, then, amid a pullback in bitcoin, eased to around $55. The metric is about 60% above the annual lows seen in August and September but roughly half of March’s pre‑halving levels.

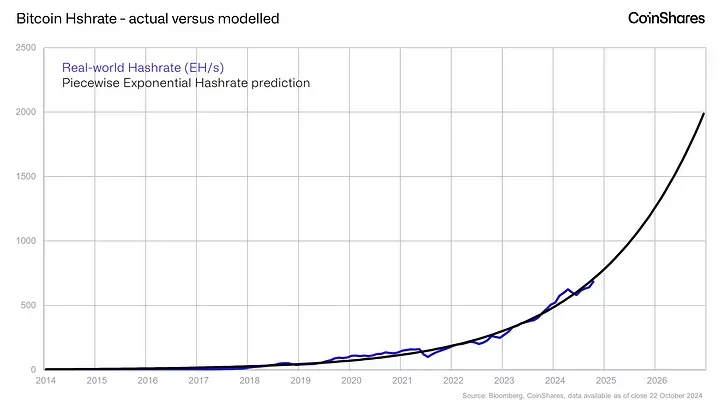

Rising difficulty, tracking hashrate, is putting further pressure on margins.

Rising hashrate puts miners on the brink

In December, bitcoin’s computational power reached a record 801 EH/s (7 DMA), according to Glassnode.

After the halving, some talked up miner capitulation; others, like CryptoQuant founder and CEO Ki Young Ju, disagreed. In July, however, the firm’s analysts conceded that miners had begun unplugging inefficient rigs and selling BTC reserves. A trend reversal followed a month later, signalled by the Hash Ribbons indicator.

In July the hashrate correction after the reward reduction reached its deepest point, then turned higher, outpacing bitcoin’s price. As a result, on December 30 mining difficulty hit a new all‑time high of 109.78 T.

CoinShares noted that network hashrate is rising in line with its exponential model. A continuation would push miners to the edge of profitable operation, the analysts warn.

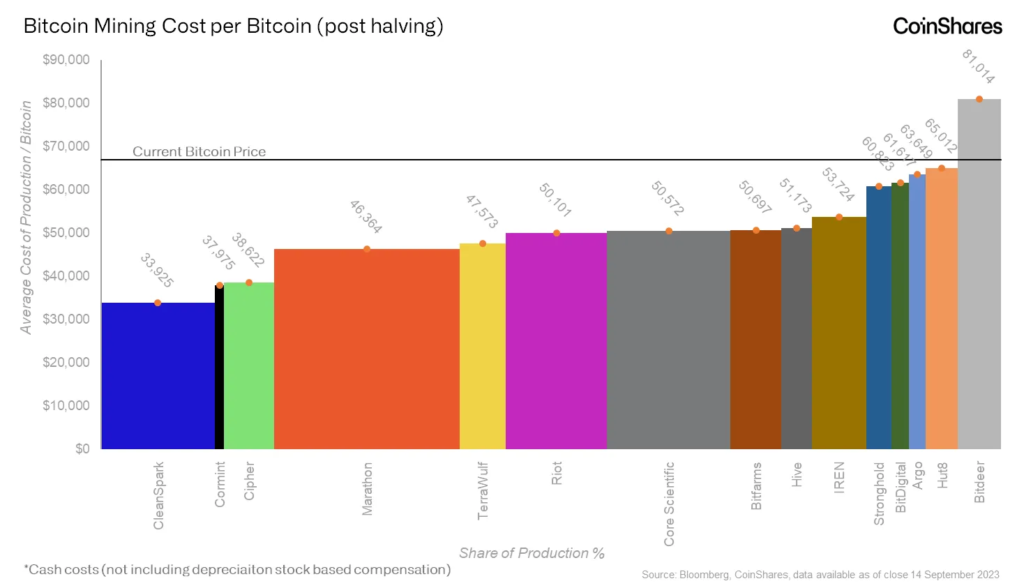

Public miners’ disclosures show that, including all costs, the full cost to mine 1 BTC in September ranged from $33,925 (CleanSpark) to $81,014 (Bitdeer).

Analysts reckon miners have ample resources to sustain profitability until the next halving in 2028. But once the reward drops to 1.5625 BTC, fees would need to make up at least 70% of revenue to keep the sector attractive to investors, especially versus direct bitcoin exposure. That seems unlikely, not least amid community fears about the outlook for on‑chain activity on Bitcoin.

CoinShares’ expectations for hashprice are also downbeat: the metric should gradually drift lower into a $32–50 per PH/s per day range by 2028.

To sustain profitability, miners need to cut costs and leverage, improve governance and raise fleet efficiency, CoinShares says.

Many industry firms are now emphasising energy‑efficiency metrics for their fleets, setting specific targets.

Manufacturers are focusing on the same parameter.

New entrants crowd into the ASIC‑miner market

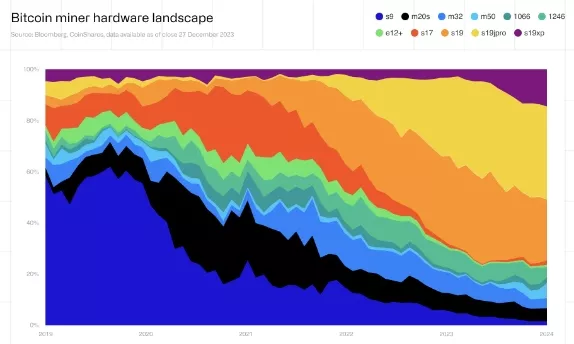

At the start of the year Bitmain’s (Antminer) devices accounted for 50–60% of global bitcoin hashrate. MicroBT (WhatsMiner) had 20–30%, Canaan (Avalon Miner) about 10% — with roughly 10% for others.

Among the latter are Ebang, Bee Computing and Innosilicon — all based in China.

The two leaders unveiled their latest ASIC generations in 2023.

Canaan caught up in May 2024, launching the Avalon Miner A15 line. Its flagship A15Pro delivers 16.8 J/TH energy efficiency.

Bitmain and MicroBT refreshed their line‑ups through the year, steadily improving that metric. The Antminer S21+ Hyd reached 15 J/TH, while December’s WhatsMiner M6xS++ line came in at 15.5 J/TH.

Both manufacturers offer customers the option to swap previously ordered units for the newest models.

According to The Mining Pod, Bitmain is making more bitcoin miners than it can sell, because it must buy a set amount of chips from TSMC under contract.

Bitmain made too many ASIC miners, and no one is buying

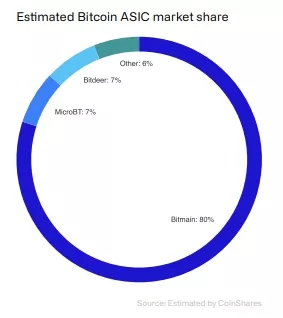

Bitmain is the largest supplier of ASIC units with an estimated 80% of the market. But its buyers aren’t very pleased with the treadmill of new units with more power, at higher efficiency. And there’s a NEW unit that might…

— The Mining Pod ? (@theMiningPod) September 4, 2024

Buyer demand is being curbed not only by miners’ weaker income but also by expectations of even more efficient models. Rumours already point to 13 J/TH, the outlet noted.

Thus, in the race for share, the manufacturer is crimping its own sales — even as Bitmain’s slice of new‑equipment shipments reached 80%, they added.

CoinShares concurs on the data but highlights the end of the ‘big three’ oligopoly. MicroBT held on with 7%, while Canaan was displaced by Jihan Wu’s Bitdeer, which captured the same 7% of sales.

Following its roadmap, the former Bitmain founder’s firm in September completed tests of the second iteration of its 4 nm bitcoin‑mining chip, SEAL02, at 13.5 J/TH. SEALMINER A2 units built on it deliver 16.5 J/TH.

The first version, at 18.1 J/TH, was introduced in March. It powers SEALMINER A1s rated at 20–23 J/TH. In Q4 Bitdeer planned to test SEAL03 at 10 J/TH for its third‑generation miners.

In July, US manufacturer Auradine, backed by MARA Holdings, announced initial shipments of its Teraflux 2800‑series ASIC miners.

@Auradine_Inc

We are excited to announce initial deliveries of the Teraflux™ 2800 series setting new benchmarks in performance, energy, resilience, and operational efficiency. https://t.co/6PwFTxY4xp… #bitcoin? #bitcoinmining #madeinusa #btc?— Auradine (@Auradine_Inc) July 25, 2024

The stated energy‑efficiency of the air‑cooled AT2880 is 16 J/TH; the immersion‑ready AI3680 is 15 J/TH.

That same month, Jack Dorsey’s Block helped chip away at Chinese dominance by signing a deal to supply Core Scientific with 3 nm bitcoin‑mining chips — a transaction Bernstein pegged at roughly $300 million.

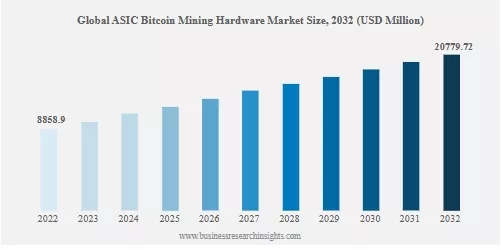

CoinShares puts the 2024 market for new bitcoin miners at $15–30 billion. Business Research Insights is more conservative, seeing a figure just above $10 billion, rising to $20.8 billion by 2032.

Bernstein believes US miners alone will “consume” $20 billion of equipment over the next five years. China’s MicroBT and Bitmain have already set up manufacturing in America, but domestic makers will clearly take a slice too.

Notably, this year also saw the geography of mining expand.

Africa barges into bitcoin mining

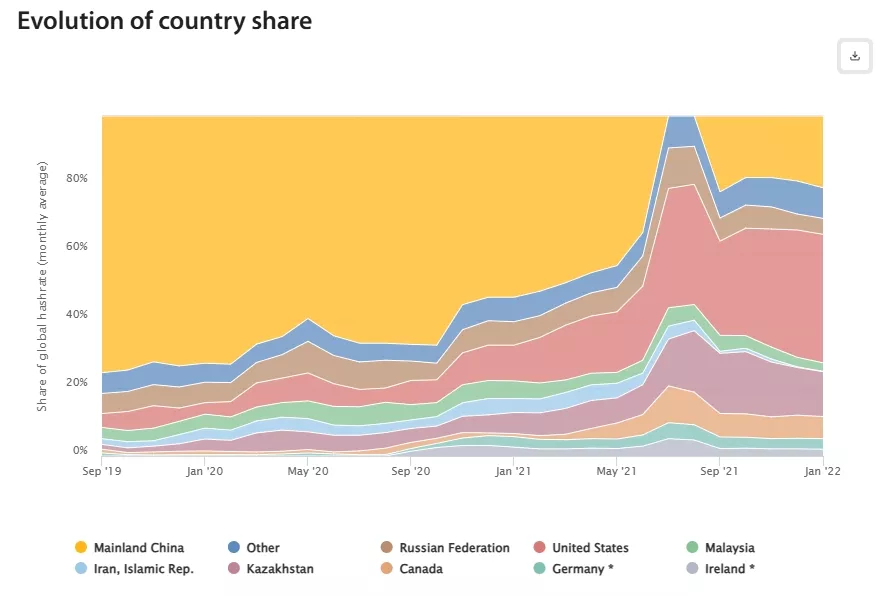

Cambridge’s Centre for Alternative Finance (CCAF) has not updated its country hashrate map since January 2022. Even so, industry experts broadly agree the US still leads with a 37–38% share.

Public miners in the US alone operate around 30 EH/s.

“Based on our client base, we believe that most of the hashrate growth is occurring in the United States,” noted Luxor COO Ethan Vera.

Prospects for America’s further dominance are reinforced by president‑elect Donald Trump’s pledge to support the mining sector.

In Vera’s view, Russia and China follow — with the top three accounting for 60–80% of global hashrate.

In September, Bitriver CEO Igor Runets estimated Russian miners’ power draw at 2.5 GW, implying some 12.5% of hashrate.

Russia adopted mining regulations, and the industry even floated listings by big players. But experts say further growth has run up against infrastructure constraints.

Kazakhstan and Canada reduced their shares of bitcoin hashrate in 2024.

In South America, Paraguay’s grid could not cope with the influx of miners. After tariff hikes, businesses began to leave. Neighbouring Argentina benefited, as the government of Javier Milei pursues industry‑friendly policies.

Against this backdrop, Ethiopia’s share reached 2.5% with clear room to grow. A further roughly 3–6 EH/s across Africa is split among Nigeria, Angola, Libya, Zambia and others — and specialists forecast ‘larger deployments’ in these countries next year.

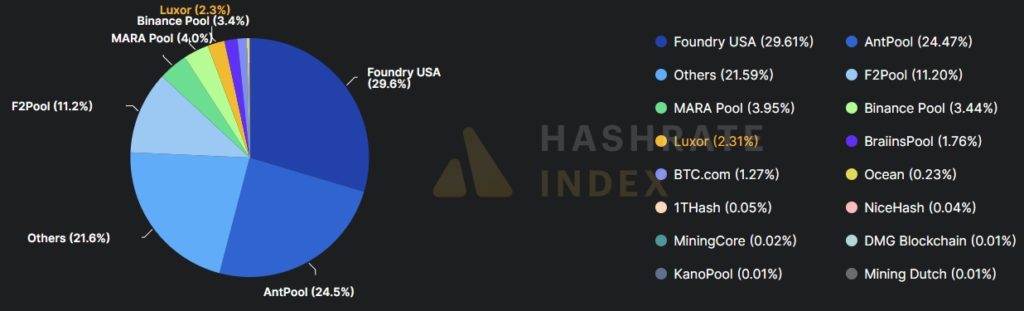

By pool, Foundry USA leads with 29.6% (based on average hashrate over the year).

US‑based entities, including MARAS Pool and Luxor, are steadily expanding their share, eroding the dominance of Chinese pools. Analysts say this is further evidence that US hashrate is growing faster than elsewhere.

Conclusions

The industry lived through another halving and emerged stronger, as record hashrate attests. But before the next reduction in block rewards, miners must address declining profitability.

AI is both a ‘lifeline’ for some miners and a competitor for scarce energy and infrastructure.

The state of that infrastructure in the US is one reason local firms look set to keep dominating. They can also tap the world’s deepest capital markets and political support. Equipment makers are plainly betting on America, too.