Every bull market has revived the hardy narrative of finding the perfect “Ethereum killer”. Since 2017, dozens of projects have hit the market promising to become a better version of the second-largest cryptocurrency.

ForkLog reviews the evolution of alternative layer-1 (L1) blockchains—what they promised, the billions they raised, and the harsher reality protocol teams face in 2026.

Early-stage fundraising data are from ICO Drops; total value locked (TVL) figures are from DeFiLlama.

The standard is born—and early pretenders to the throne

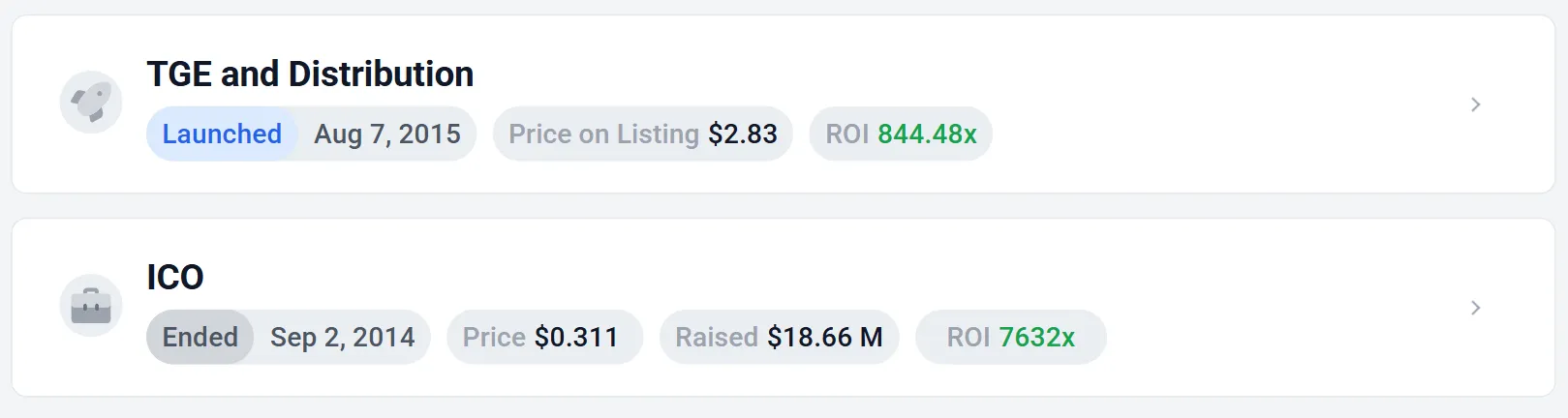

In 2014, when crypto was synonymous with bitcoin, Ethereum’s co-founders held a historic ICO. From 22 July to 2 September the project raised 31,591 BTC (then about $18.6m). Investors bought the offered ETH at an average price of $0.31.

After the TGE in 2015, Ethereum’s concept of a “world computer” powered by smart contracts looked like a breakthrough. Yet low throughput, a new programming language (Solidity), unfamiliar DAO governance and UX hindered adoption. Early rivals rushed in.

Neo X (formerly NEO)

Launch: 2016

Funds raised: first public-sale round in October 2015 — $560,000; after the 2016 TGE — an additional $4.5m

Founded in 2014 as Antshares, the project rebranded to NEO and continued as a layer‑1 blockchain. Marketed as the “Chinese Ethereum”, it leaned into Solidity’s niche appeal and instead let developers write smart contracts in C# and Java.

In 2023, facing thin liquidity, the team took a step toward Ethereum’s orbit. A year later it launched the Neo X EVM mainnet.

Launch: 2017

Funds raised: ~$62m

Created by Ethereum co-founder Charles Hoskinson, Cardano embraced an academic approach with the PoS consensus Ouroboros. Its L1 extended the UTXO model to support smart contracts (EUTXO). The protocol pitched itself as “the only PoS family member with mathematically proven security”.

In 2024 the project faced a wave of criticism hinting at the ecosystem’s “death”. Hoskinson replied with “major upgrades” aimed chiefly at a transition to decentralised governance.

Cardano’s focus areas include government initiatives, enterprise solutions, RWA and digital identity.

Launch: 2017

Funds raised: ~$242m before TGE

Flush with ICO cash, Tezos sought to outmanoeuvre rivals amid the post–The DAO hard‑fork rifts by introducing on‑chain, vote‑based governance. Despite the innovation and war chest, it failed to hold ground after the “DeFi summer” ended in 2022. As of April 2026 the network ranks 51st by TVL ($28.14m).

In 2026 a major Tezos X upgrade is planned. The team is shifting from a monolithic L1 toward a rollup ecosystem built on modular architecture. The EVM‑compatible Etherlink targets closer alignment with Ethereum, a move away from the niche Michelson language, and RWA/DeFi for business.

Vaulta (formerly EOS)

Launch: 2017

Funds raised: an industry record — over $4bn during the ICO

The EOS token sale ran for about a year—from 26 June 2017 to 1 June 2018. Block.one pitched it as a high‑throughput operating system with zero fees, enabled by DPoS. Designed by EOS co‑founder Dan Larimer, the model relied on 21 validators and a complex governance structure. The lack of decentralisation drew criticism, as did questions about the integrity of the ICO.

In 2022 Block.one was accused of underfunding protocol development. Larimer supported the community’s effort to regain control of a $4.2bn treasury. Prolonged corporate lawsuits between the EOS Network Foundation and Block.one ultimately pushed the former to rebrand. A strategic pivot to Web3 banking under the new name Vaulta followed in 2025.

Launch: 2017

Funds raised: ~$78m before TGE

Self‑styled as an “Ethereum killer”, TRX initially launched as an ERC-20 token before migrating to its own chain.

The protocol borrowed Ethereum Foundation’s codebase and EOS’s DPoS consensus. For that, Vitalik Buterin publicly accused TRON founder Justin Sun of plagiarism.

Its trump card was integrating USDT. High speed and low fees made the chain one of the most popular rails for the stablecoin.

The DeFi era and the venture boom

Ethereum steadily became DeFi’s home base. Between 2019 and 2021 average fees rose to $5–20 and in peak periods exceeded $60. Costs opened a flank that a new crop of VC‑funded L1s exploited in their marketing.

Launch: 2017 (mainnet and TGE in 2019)

Funds raised: ~$126m

The founder— a Turing Award laureate, Silvio Micali — promised to solve the “blockchain trilemma” with Pure Proof‑of‑Stake.

The engineering was meticulous; tokenomics and investor psychology, early on, were not.

Validator full nodes (relay nodes) became a closed club run by universities and corporations sponsored by the Algorand Foundation.

Matters worsened with cyclical investor sell‑offs (accelerated vesting) and heavy marketing spend.

By 2026 many flaws had been addressed, but lost time dented the protocol’s DeFi standing. According to DeFiLlama, as of April 2026 the platform’s 30‑day fee revenue was $408.

Algorand continues to focus on RWA (real‑estate tokenisation via Lofty), and enterprise and government solutions. In 2025 the blockchain was used to create a digital health passport for women in India.

Launch: 2020

Funds raised: ~$360m (of which ~$314m after the 2021 TGE)

Launching into “DeFi summer”, Solana pitched itself as a high-speed network with sub‑cent transactions enabled by Proof‑of‑History (PoH).

Buoyed by post‑TGE capital, the team stayed on‑trend: close ties with FTX, the NFT boom, a chain for DePIN projects, a crypto smartphone, RWA. It also subsidised user growth and offered developers funding for development.

The rapid rise of the SOL token, speed and cheap transactions drove adoption across DeFi—even frequent outages did not deter users.

At the peak of the meme‑coin trend, Solana became a liquidity centre for that asset class. Later, that spurred an outflow of traders amid more frequent fraud.

In 2026 the platform entered the top three by USDT transfer count.

Launch: 2020

Funds raised: ~$248m (of which ~$205m before TGE)

Addressing Ethereum’s scaling challenge, co‑founder Gavin Wood, after his departure, proposed a Layer‑0 design with parachains sharing the security of a central relay.

Thanks to a decentralised validator set, Polkadot has the highest Nakamoto coefficient—123, as of April 2026.

As elsewhere, strong technology without fitting tokenomics, incentives and marketing did not lead to a fair fight with Ethereum.

The network has dropped rigid parachain‑lease auctions, now targeting B2B and bespoke enterprise chains. In late 2025 it posted its first quarterly profit in three years.

BNB Chain (formerly Binance Smart Chain, BSC)

Launch: 2020

Funds raised: self‑funded by Binance

Binance’s corporate fork of Ethereum sacrificed decentralisation for low fees. The EVM‑compatible network targets DeFi, meme‑coin trading, gaming and popular verticals, including RWA.

The project is one of the DeFi leaders and a serious challenger to Ethereum. Its ecosystem includes top apps: the DEX PancakeSwap, the lending protocol Venus, and RWA platforms Securitize and Circle USYC.

Launch: 2020

Funds raised: ~$285m (of which ~$55m before TGE)

An architecture of three built‑in chains (X‑Chain, C‑Chain, P‑Chain) and a graph‑based consensus (DAG) deliver instant finality and custom subnets.

The split isolates heavy smart‑contract compute from basic asset transfers and staking, protecting the network from critical overloads. Avalanche anticipated today’s broad shift toward modular blockchains.

Its current strategy centres on institutional subnets, use in the public sector and RWA, courting traditional banks and funds.

Launch: 2020

Funds raised: ~$544m (of which ~$503m after TGE)

A bet on sharding (Nightshade) and UX (human‑readable addresses) was meant to attract the masses. In practice, convenience and technology were not enough to win liquidity and developers.

Having stepped back from head‑on L1 competition, NEAR has become a hub for chain abstraction and consumer AI apps, aiming for a seamless Web2‑like experience. A key tool is Chain Signatures, which lets users control assets on other networks (including bitcoin and Ethereum) from a single NEAR account.

Launch: 2021

Funds raised: ~$167m before TGE

ICP began as an ambitious “killer of the centralised internet and Ethereum”. Management promised to replace AWS and host social networks on‑chain, but failed to cope with market manipulations, after which the ICP token fell 95%.

Today it is not an Ethereum rival, but a distinctive L1 serving as decentralised hosting for Web3 and enabling cross‑chain liquidity control without vulnerable bridges. The current focus is AI and decentralised cloud storage.

In February 2026 Pakistan’s Digital Authority and DFINITY, ICP’s core developer, signed an MoU to build sovereign digital AI infrastructure—keeping confidential data at home and reducing reliance on foreign cloud providers.

Full speed to the graveyard

After Ethereum’s transition to Proof‑of‑Stake and a shift toward L2, would‑be “killers” pivoted to parallelisation and a speed race. The new wave of L1s includes:

- Aptos (2022) and Sui (2023). Heirs to Meta’s shuttered Diem, their novelty lies in the Move language and parallel execution. Both now cast themselves as flagships of GameFi and DeSoc, targeting retail users who expect instant, lag‑free Web3 apps;

- Sei (2023). Positions itself as an L1 solely for trading with 400ms finality. With a narrow specialisation, Sei acts as a universal liquidity engine for traders and DEX builders;

- Berachain (2024–2025). Built on Cosmos SDK with a Proof‑of‑Liquidity (PoL) consensus, where liquidity providers secure the chain. Its strategy is radical gamification of finance, turning classic staking into a speculative flywheel;

- Monad (2025). Created by alumni of Jump Trading, it raised $225m to deliver Ethereum‑compatible parallel execution. The focus is DeFi and speed for trading.

Today, most boasts of surpassing Ethereum look naïve. Its ecosystem has held the lead thanks to network effects, security and L2s that neutralised high fees.

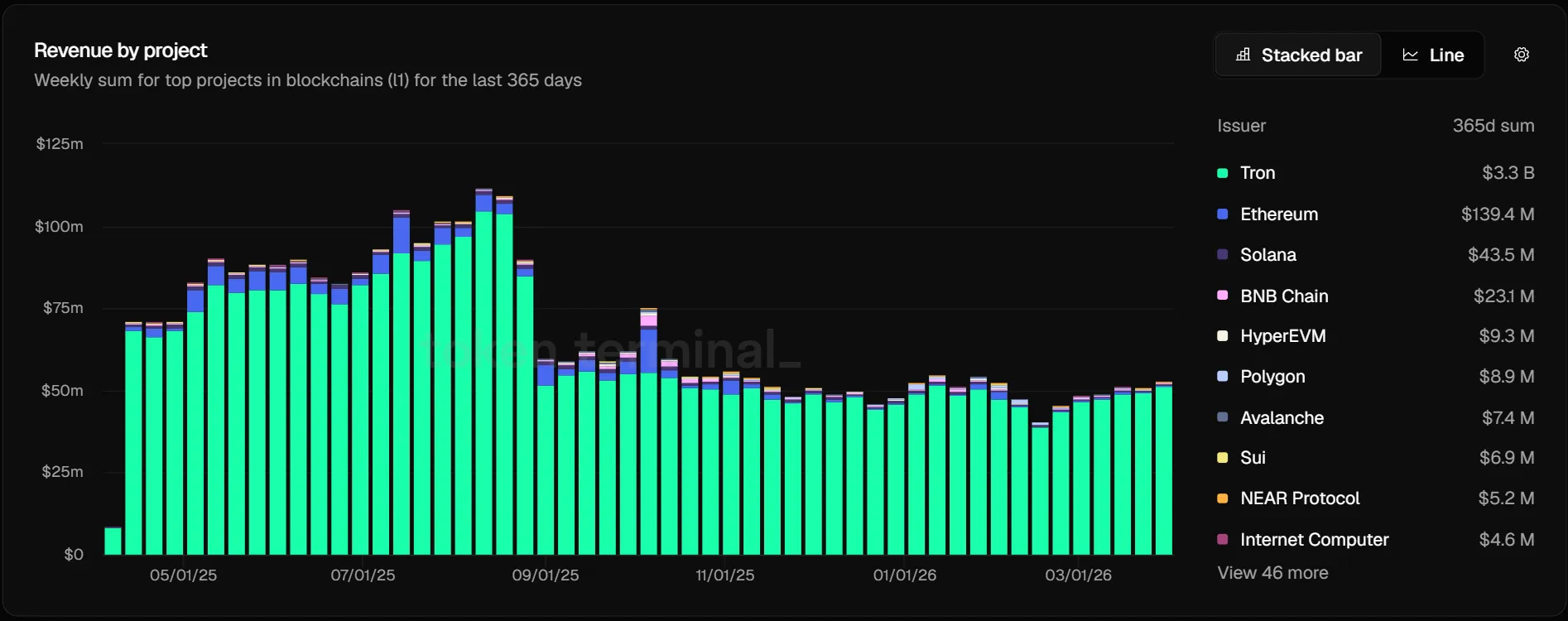

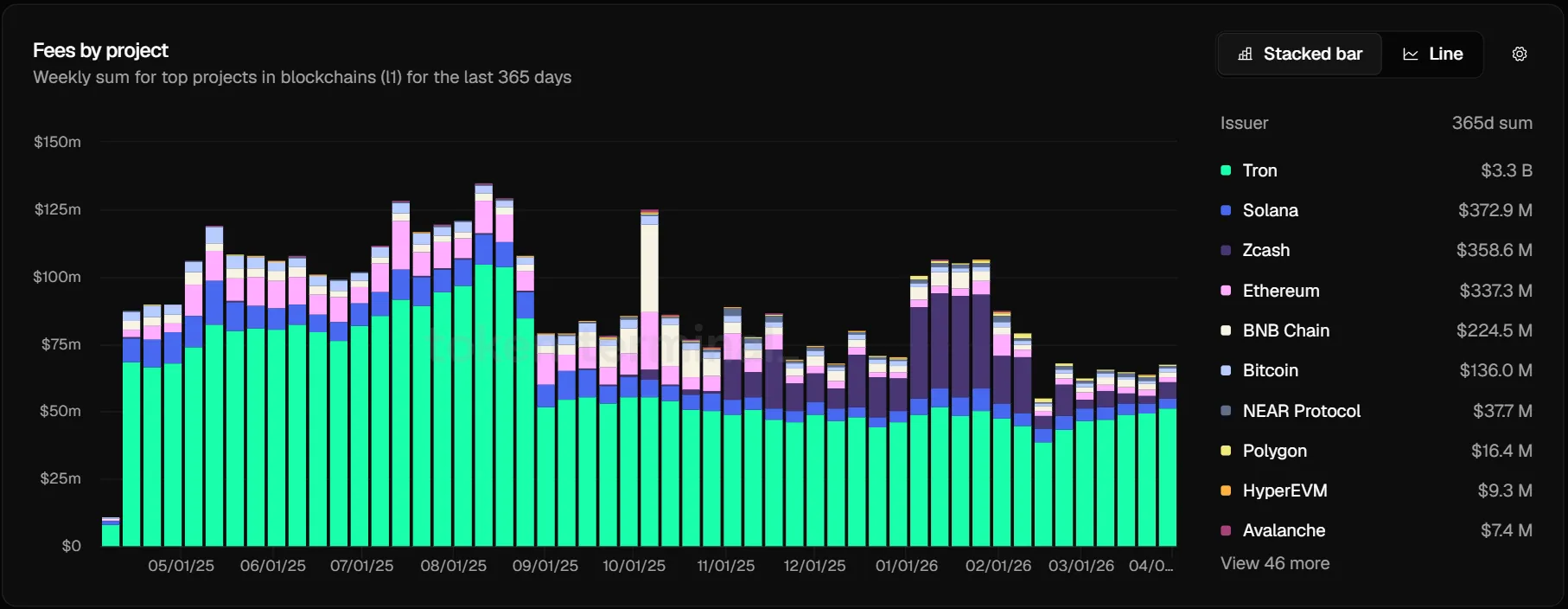

TRON has overtaken Ethereum on a crucial metric: stablecoin transfer volume. Sun built a cheap payments rail for a fiat alternative—worlds away from a decentralised “world computer”.

According to Token Terminal, as of April 2026 TRON ranks first by revenue from transaction fees, well ahead of Ethereum, at $3.3bn.

Solana is the only chain to have built an independent ecosystem and a loyal community comparable to Ethereum’s. It is blisteringly fast, but demanding validator hardware and periodic outages still raise questions.

Most 2019–2021 vintages are technically diverse but financially weak:

- Cardano and Algorand keep polishing academic code, but suffer from a dearth of real users and liquidity;

- Avalanche and NEAR saw speculative capital ebb away. In bull markets they served as cheap retail alternatives, but ultra‑cheap Ethereum rollups diluted their pitch. They remain technically active and sign corporate deals, yet their crypto market share keeps shrinking;

- EOS and NEO are trying to stir, but look more like relics.

The new cohort of builders is betting on extreme hardware optimisation and parallel execution. History suggests crypto rarely crowns the fastest tech—it favours the one with the strongest social consensus. On that measure, Ethereum’s base layer remains the clear leader.